A timely note from Westpac. I am not concerned about this.

Demand is going to fall materially globally and deliver a nasty trade shock just as an inventory cycle triggers a reverse bullwhip effect. These are circumstances in which imports and exporters are going to absorb FX impacts in their margins, not pass them on. Especially so given preposterously elevated corporate margins.

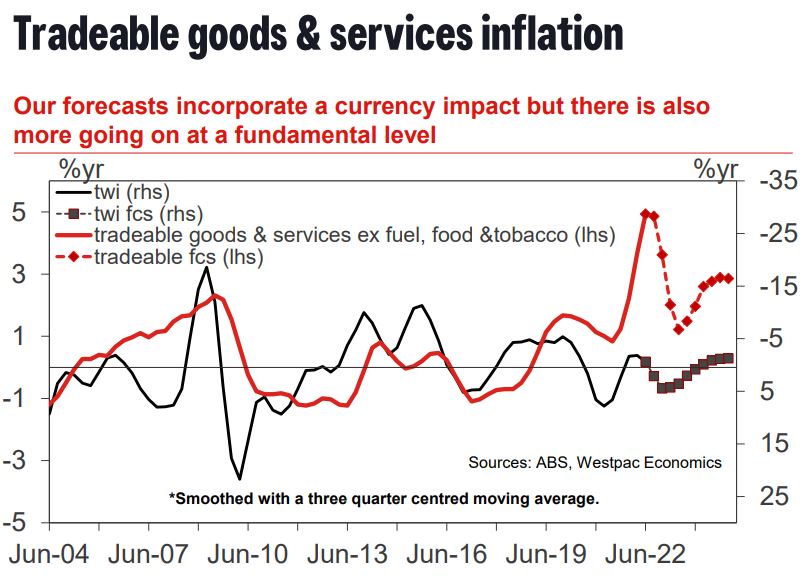

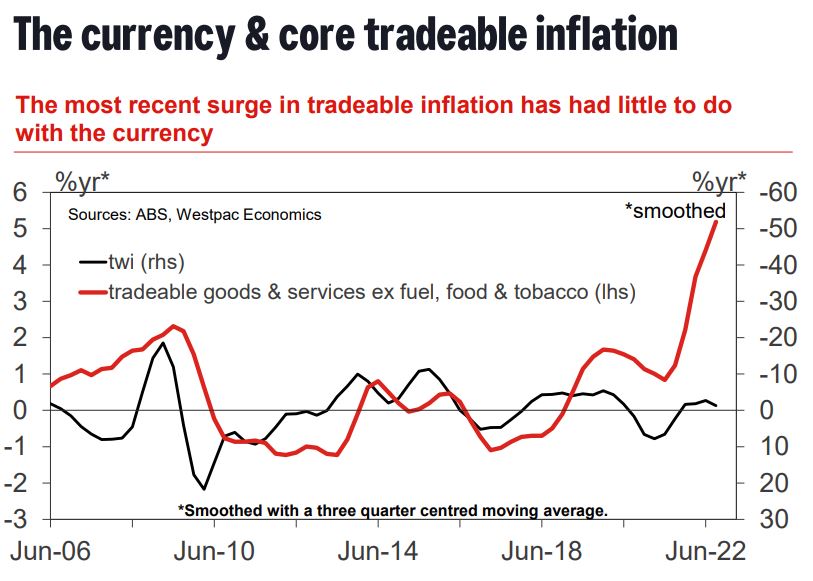

Westpac is underestimating how much deflation is coming as margins revert to mean. As it says itself on the second chart, the recent surge in tradable inflation had nothing to do with FX and this is where the big reversal will be: goods and lots of ’em!

Rough rule of thumb – a 10% depreciation of the currency will lift the CPI by around 0.3ppt to 0.4ppt though the next six months.

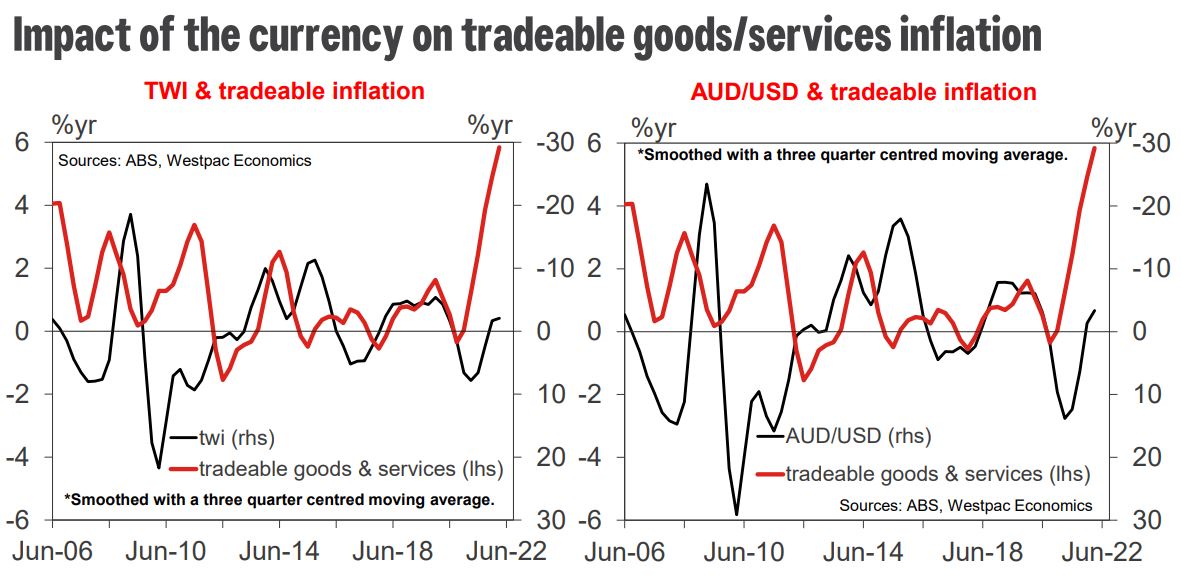

As well as the currency the consumer price of imported goods and services will also reflect global prices, freight, shipping and warehousing costs plus local margins. As such the effect of the currency can often be masked by these other factors.

But that is not to say the currency has no impact.

The exchange rate has a broad, but far from perfect, relationship with core tradeable good & services (ex food, fuel & tobacco). A 10% rise in the currency will lower the tradeable goods & services (ex food, fuel & tobacco) by 2%.

As core tradeable has a weight of 12.4% in the CPI -10% on the currency will lower the CPI by 0.25ppt.

A rough rule of thumb is that a 10% fall in the currency will lift auto fuel prices by around 1.3% through next month. Fuel has a weight of 3.6% in the CPI so a 10% fall in the currency boosts the CP 0.05ppt.

A 10% fall in the currency has a +0.05ppt impact via fuel and +0.25ppt via tradeable goods & services.

In total a 10% fall in the currency will result in a 0.26ppt boost to the CPI.

For total tradeable goods & services a 10% fall in the exchange rate will raise prices for this group by around 1% – being 37% in the CPI this will generate a 0.37ppt increase in the CPI.