Westpac with the note. In a few words: commodity prices and the reopening boom.

The Federal budget position improved dramatically during the 2021/22 financial year, exceeding all expectations.

The underlying cash deficit came in at -$32.0bn, representing -1.4% of GDP. That was $47.9bn less than forecast in the 2022/23 March Budget.

The deficit narrowed sharply from the record deficit in 2020/21, at the onset of the pandemic, of -$134.2bn, -6.5% of GDP.

Receipts for 2021/22 were $27.7bn higher than anticipated. Payments were $20.1bn lower than expected.

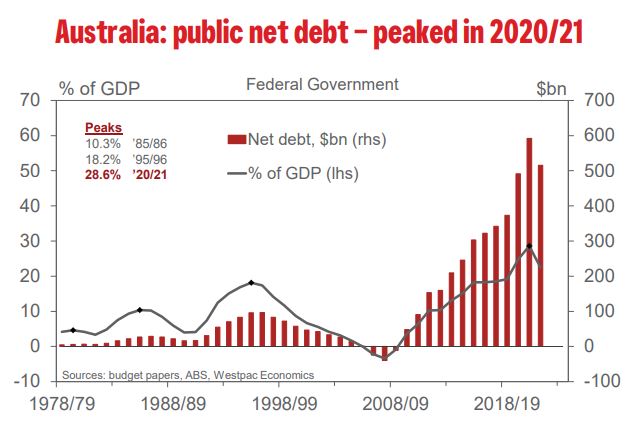

Net debt at June 2022 was $515.6bn, 22.5% of GDP, some $115.8bn lower than forecast in the Budget. Net debt peaked in 2020/21, at $592.2bn, 28.6% of GDP – declining by $76.6bn in 2021/22.

Gross debt at June 2022 was $895.3bn, 39.0% of GDP, a $10.7bn downside surprise. As a share of the economy, gross debt declined by 0.5% of GDP, down from a peak of 39.5% in 2020/21.

Economic overview

The Australian economy grew at a rapid pace in 2021/22, with nominal GDP growth of 11.0% – a fraction above the 10.75% forecast in the Budget.

While the Budget forecast of the economy was broadly correct, the fiscal numbers – revenue and payments – diverged considerably from the official forecasts, as noted above.

Double digit nominal GDP growth is well above par, a result significantly boosted by the terms of trade climbing to a record high, up 12.1% in the year, on higher global commodity prices.

Another factor was relatively high inflation more generally.

The mining sector was a major beneficiary, with mining profits up by 46% in the year.

Output grew by a brisk 3.9% in 2021/22, a fraction below the Budget forecast of 4.25%. The strong result was supported by earlier policy stimulus and the progressive relaxation of covid restrictions.

Labour market conditions were generally stronger than anticipated in the Budget. Employment grew by 3.3% in the year to the June quarter 2022, exceeding the forecast of 2.75%. Wages, as measured by the Wage Price Index, grew by 2.6% over the year to June, in line with the Budget forecast of 2.75%. Total compensation of employees increased by 5.6% in the 2021/22 financial year.

Revenue detail

Revenue for the 2021/22 year came in at $584.4bn, 25.4% of GDP.

This included $536.6bn in taxation receipts, 23.4% of GDP, a $24.1bn upside surprise. The upside surprises was centred on company tax, +$14.2bn, and individuals, +$6.8bn. Lower-than-expected utilisation of COVID-19 business support measures, such as temporary full expensing and loss carry-back, was a factor contributing to the higher than expected company tax receipts.

Non-tax receipts totalled $47.8bn, some $3.6bn above expectations.

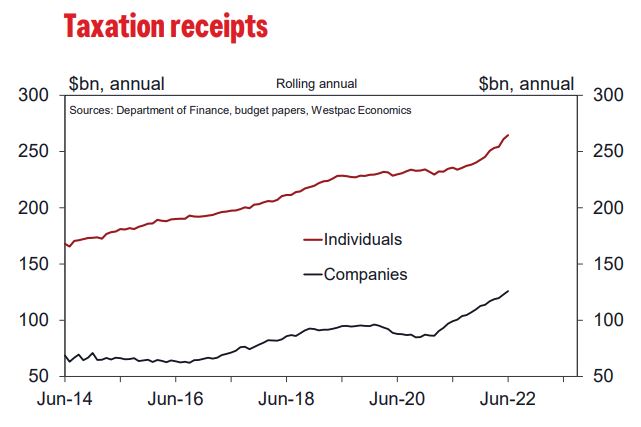

By way of further detail on tax receipts, in accrual terms they came in at $550.4bn for 2021/22. That was an increase of 14.6% on a year ago, +$70.2bn.

Income tax on individuals was $264.6bn, accounting for 63% of total tax receipts. That outcome was up 12.3% on a year ago, a rise of $28.9bn.

As to company profits, they were $125.9bn for the year, 30% of the total. That was a 27% increase on the year prior, a rise of $26.8bn.

Expenses detail

Payments were $616.3bn in 2021/22, 26.8% of GDP, a downside surprise of $20.1bn.

The FBO document cites a number of factors impacting specific programs, which together accounted for $11.1bn of lower than expected payments – 55% of the downside surprise.

The budget paper cites:

* “programs that provide funding responding to COVID-19 have experienced delays or lower-than-estimated demand;

* health-related programs experienced lower-than-estimated demand;

* several programs were also impacted by disruptions to supply chains and capacity constraints, resulting in lower-than-estimated payments or payment delays;

* other programs also experienced lower-than-estimated take-up; and

* the outcome also reflects increases in payments in certain programs”.

We note that the stronger than expected labour market will have placed downward pressure on social welfare payments, likely contributing to the lower than expected payments. Unemployment declined to 3.75% in the June quarter, below the Budget forecast of 4%, and employment growth was materially stronger (3.3% vs an expected 2.75%).

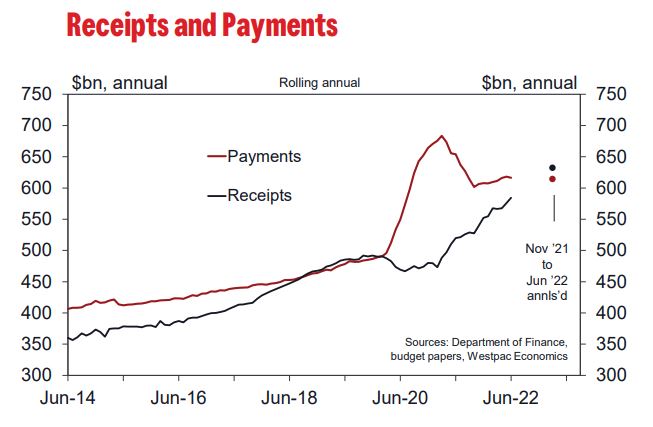

Lock-down and reopening: dramatic budget impact

Conditions have been volatile over the past couple of years, with covid related restrictions greatly disrupting activity at times.

This was evident in the 2021/22 financial year, with the opening months impacted by the delta lockdowns in the two largest states, NSW and Victoria.

The transition from lockdowns to reopening had a dramatic impact upon the fiscal numbers during 2021/22 – the $32.0bn deficit for the year as a whole reflected two very different periods.

Over the opening four months of 2021/22, July to October, the cumulative budget deficit came in at $43.9bn.

Over the eight months November to June 2022, benefiting from the reopening, the budget swung into surplus, to the tune of a cumulative $12.0bn.

Between the two periods, the monthly pace of receipts jumped by 29% ($40.7bn to $52.7bn), while payments stabilised, down -1% ($51.7bn to $51.2bn).

Recall that in 2018/19, prior to the pandemic, the budget was in balance.

An uncertain outlook

Where to from here remains highly uncertain.

There is a looming sharp slowdown of the Australian economy in response to an aggressive RBA tightening cycle. In addition, global commodity prices have retreated from their highs on global recession concerns.

The upcoming Federal Budget on October 25 – the initial budget of the newly elected government – will provide an update of official forecasts, both economic and fiscal.

Today, Federal Treasurer Chalmers has reportedly stated: “don’t expect to see surplus in budget forward years”, adding that “budget pressures intensifying, rather than easing”.

In earlier comments, at a Joint Press conference with the Finance Minister on September 20, Treasurer Chalmers highlighted “the five big growing areas of spending in the budget, which are creating pretty substantial structural concerns. Health, NDIS, aged care, defence, and the cost of servicing a trillion dollars in debt, all of those costs are growing fast. And that’s a combination of the unavoidable and the desirable, and so we do need to have a conversation about that”