AMP Capital’s chief economist, Shane Oliver, has written a detailed note explaining why he believes that “this time is different” for Australia’s housing market, and why “this downturn will likely be deeper and the recovery slower than in past cycles”.

Dr Oliver believes three primary factors will conspire to drive a “15-20% top to bottom fall in home prices out to the second half of next year”, namely “higher home price to income levels; higher debt levels; and an end to the long-term decline in interest rates”.

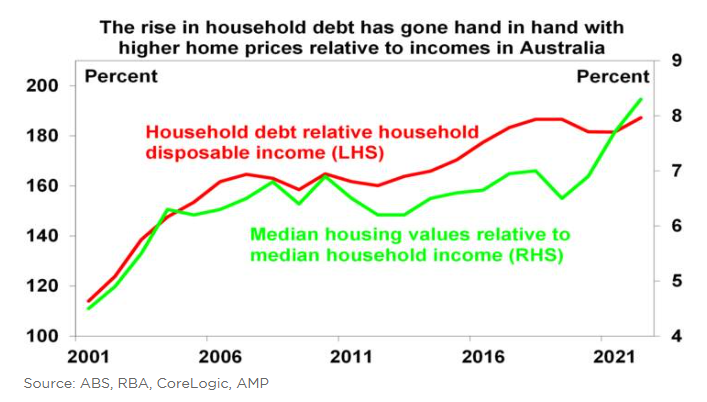

Regarding the first factor – higher home price to income levels – Oliver notes that “home price to income ratios are now very high, which will limit their upside, unlike 30 years ago”. This is illustrated by the next chart, which shows that the rise in household debt (the second factor) has gone hand-in-hand with the march higher in house prices:

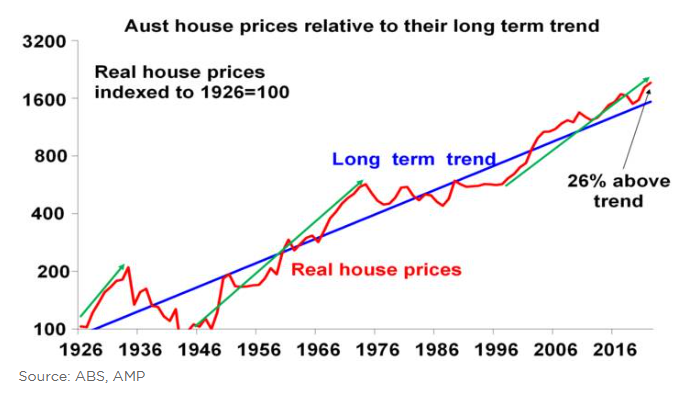

According to Oliver, “the boom over the last 25 years has seen real property prices rise from about 23% below their very long-term trend to 26% above”. And this boom “has been largely driven by the shift to low interest rates and a surge in population relative to housing supply”:

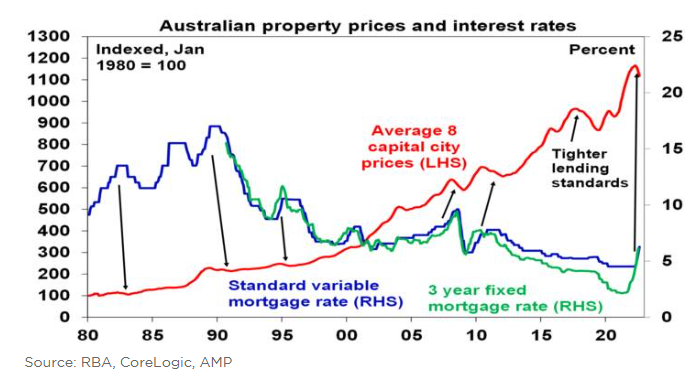

However, “the 32-year falling trend in mortgage rates from 17% in 1989 to 2% – which enabled new buyers to borrow & pay more for property and drove strong investor “search for yield” demand, is likely over”. Instead, the “world is now more inflation prone,… so a return to a 0.1% cash rate & 2% fixed rates looks unlikely”:

Oliver notes that his forecast 15-20% peak-to-trough decline in house prices is based on the official cash rate peaking at 2.6%. However, “if the cash rate is raised to the 4% level the money market is assuming – this would more than double household interest payments and push total mortgage repayments to record highs relative to incomes & likely drive a 30% or so fall in prices”.

So basically, the housing market’s destiny is in the hands of the RBA.