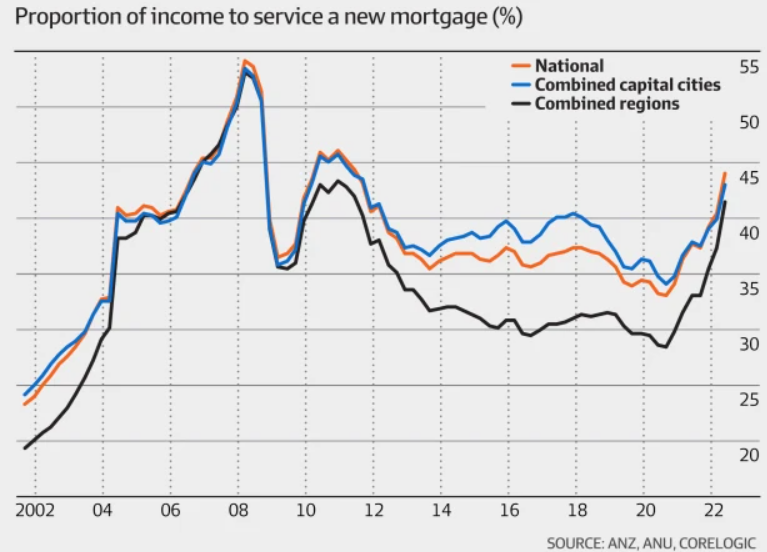

ANZ has released a new housing affordability report, which shows that the proportion of income required to service a new mortgage has surged from 34% last year to 44% in the June quarter:

“There’s a bit of a perception that if house prices fall, then mortgage affordability will improve but actually, on our interest rate forecasts, prices would have to fall another more than 25 per cent for mortgage serviceability to improve, and we don’t think that prices will fall that far, certainly not a national level.

“So with higher interest rates, we are seeing a big increase in how much people have to pay to service their mortgage and that means on that measure, affordability will deteriorate.”

The above data only captures the first two interest rate hikes from the Reserve Bank of Australia (RBA), and does not capture the 0.5% consecutive rate hikes in July and August.

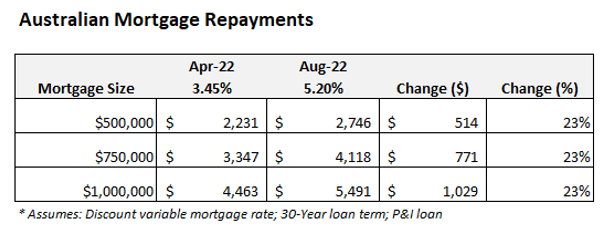

As illustrated in the table below, the average discount variable mortgage rate has already risen to 5.2%, up from 3.45% in April:

Advertisement

Average mortgage repayments have already risen 23%.

In turn, average monthly mortgage repayments have soared by 23% from their April pre-tightening level.

For a household with a $500,000 mortgage, this represents a monthly increase in repayments of $514, whereas a household with a $1,000,000 mortgage will pay an extra $1,029 a month.

Advertisement

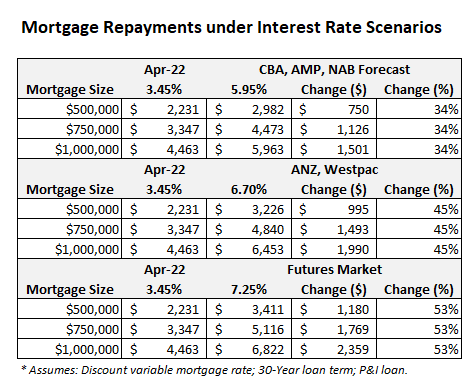

While everybody expects the RBA to continue hiking rates, economists are divided on how far.

CBA, AMP and NAB believe that the official cash rate (OCR) will peak at 2.6% per cent, whereas ANZ and Westpac forecast a 3.25% peak in early 2023.

The futures market is even more hawkish, pricing a peak OCR of 3.9% by mid-2023.

Advertisement

The impact on Australian mortgage holders would be a bitter pill to swallow under all scenarios, as illustrated by the next table:

Aussies facing big lift in mortgage repayments.

Under the lower CBA, AMP and NAB OCR forecast, Australia’s average discount variable mortgage rate would rise to 5.95%.

Advertisement

In turn, average monthly mortgage repayments would rise by 34% versus their level in April before the RBA commenced its rate tightening cycle.

The higher OCR forecasts of ANZ/Westpac and the futures market would send the average discount variable mortgage rate to 6.70% and 7.10% respectively, increasing monthly mortgage repayments by 45% and 51% respectively.

If mortgage repayments rise as sharply as the more bullish forecasts, this will crunch household budgets and detract from household consumption – the economy’s biggest growth driver.

Advertisement

The negative drag on household consumption will be exacerbated by a sharp fall in house prices, which would make Australians feel poorer.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.