A new survey of more than 3000 retirees by National Seniors and annuity-provider Challenger reveals that almost one-in-four retirees have no intention of drawing down their superannuation nest eggs to fund their retirements:

Almost 23 per cent said they did not want to spend their capital in retirement, and instead live off earnings. About half said they wanted to preserve at least some of their capital…

Treasury released a paper last July arguing the nest-egg framing of superannuation had contributed to a reluctance to spend money.

“Partly because they have only ever been primed to save as large a lump sum as possible, retirees struggle with the concept that superannuation is to be consumed to fund their retirement,” Treasury wrote.

The Australian Treasury’s Retirement Income Review noted that superannuants have been reluctant to draw down their savings, instead relying solely on their investment returns to fund their retirements. This, in turn, has turned Australia’s superannuation system into a wealth accumulation and transfer scheme that has increased inequality:

Inheritances are significant, representing the transfer of wealth from one generation to another. They are not distributed equally and increase inequity within the generation that receives the bequests. Most people die with the majority of wealth they had when they retired. If this does not change, as the superannuation system matures, superannuation balances will be larger when people die, as will inheritances. Superannuation is intended to fund living standards of retirees, not to accumulate wealth to pass to future generations…

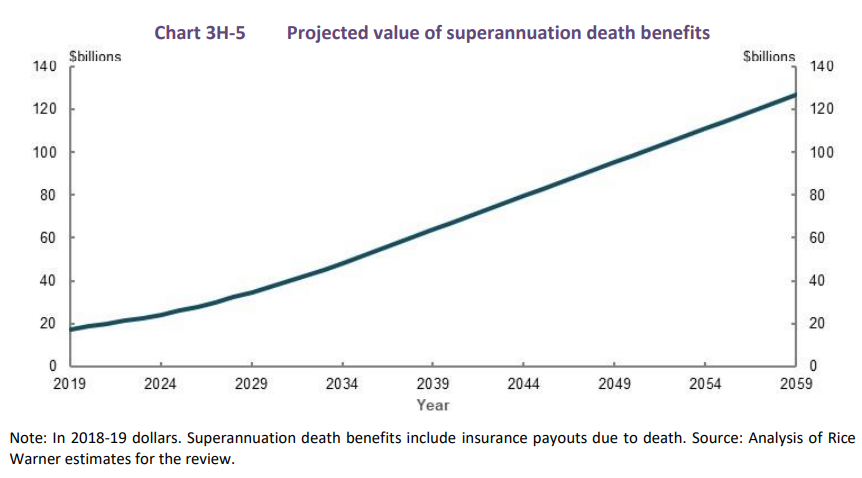

For example, assuming no change in how retirees draw down their superannuation balances, superannuation death benefits are projected to increase from around $17 billion in 2019 to just under $130 billion in 2059 (Chart 3H-5)…

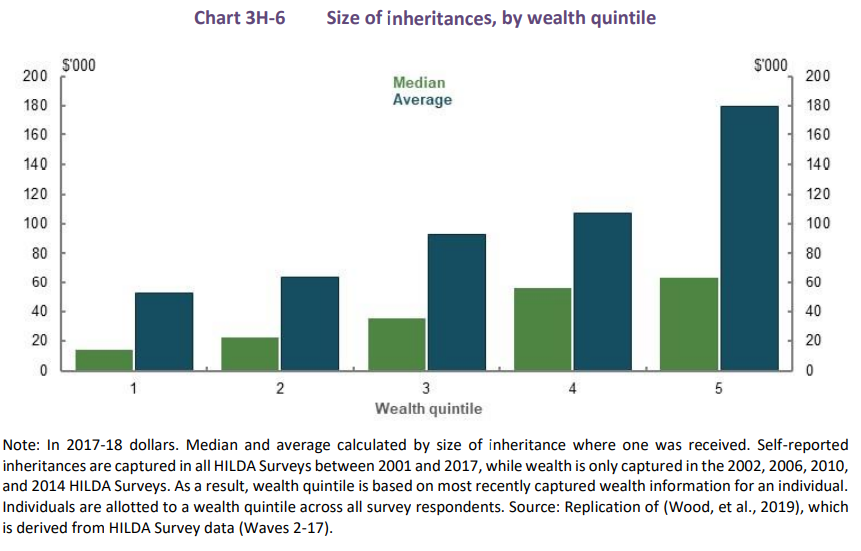

Although inheritances can help people to prepare for retirement, they are distributed unequally, with wealthier people tending to receive larger inheritances than those with lower wealth (Chart 3H6). Inheritances therefore increase intragenerational inequity…

Advertisement

Super nest eggs were never meant to be preserved in order to pass onto one’s heirs after death. They are supposed to be drawn-down to fund one’s retirement.

Consider, for example, a new retiree with superannuation savings of $500,000 earning a return of 5% annually (i.e. a combination of interest and dividends).

If this retiree relies only on investment returns to fund their retirement, they would receive $25,000 a year in income (i.e. 5% times $500,000). However, if principal is also drawn down, then $38,200 would be available over 20 years to fund their retirement.

Advertisement

In short, retirees must be made to draw-down their superannuation savings. This is a far more equitable and cheaper option than further lifting the superannuation guarantee.

The Morrison government’s retirement income covenant, which took effect last month, was a step in the right direction. This requires super funds to develop strategies that help people draw down their super balances in retirement.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.