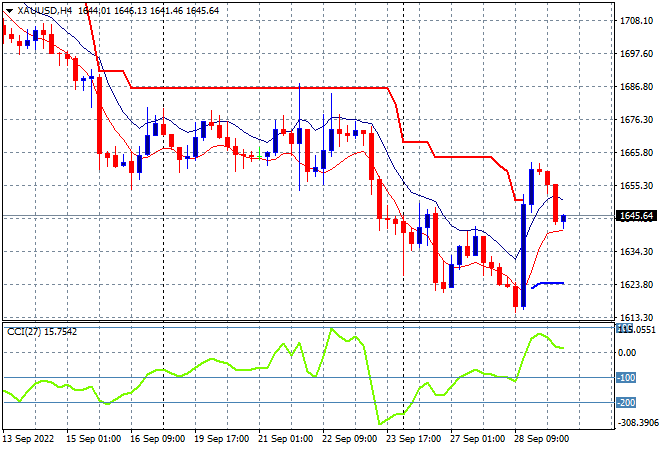

Asian stock markets have bounced back in similar fashion to European and US stocks although Chinese shares remain hesitant to take on more risk. The fallout from the BOE stepping in to save UK gilts is still being felt, while the USD has regained most of its lost ground against the major currencies, as Euro continues to fall. Meanwhile oil prices are failing to stabilise with Brent crude hovering back down to the $87USD per barrel level while gold has returned to its poor start of week position, still crushed below former support at the $1700USD per ounce level, currently at $1645:

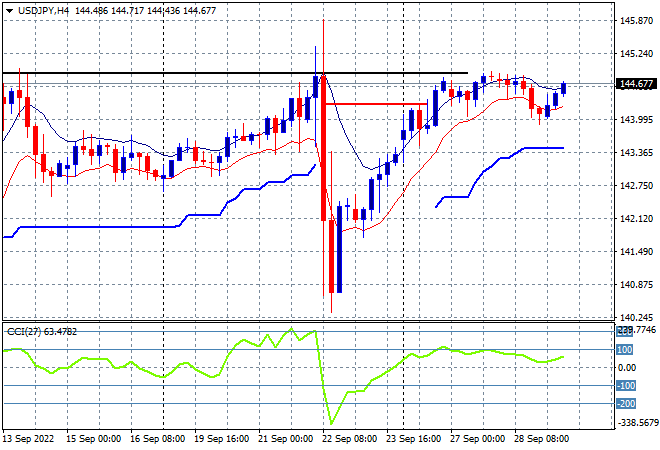

Mainland Chinese share markets are the standouts by failing to bounceback alongside overnight markets with the Shanghai Composite down 0.2% to 3039 points while the Hang Seng Index can’t get a break, down another 0.6% at 17150 points. Japanese stock markets however recovered somewhat, with the Nikkei 225 closing nearly 1% lower at 26422 points while the USDJPY pair has heading back to its recent weekly highs just below the 145 handle after last night’s very mild dip:

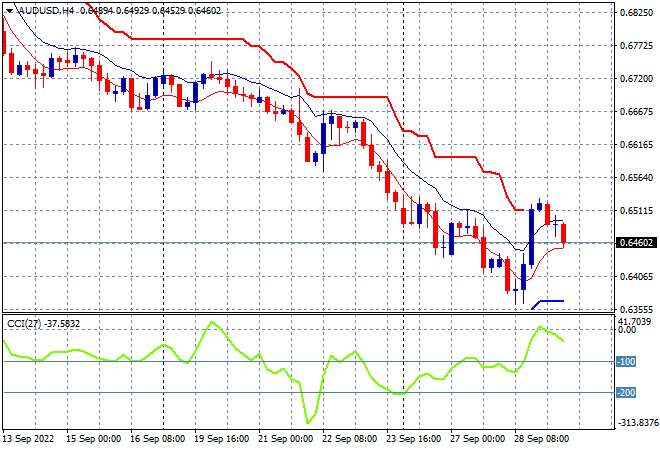

Australian stocks were the best in the region, this time to the upside with the ASX200 gaining more than 1.4% to close at the 6555 point level, bouncing off its recent monthly low. The Australian dollar has rolled over again, despite the latest CPI print with the Pacific Peso heading back below the 65 handle after last night’s sharp bounce that has proven to be shortlived already:

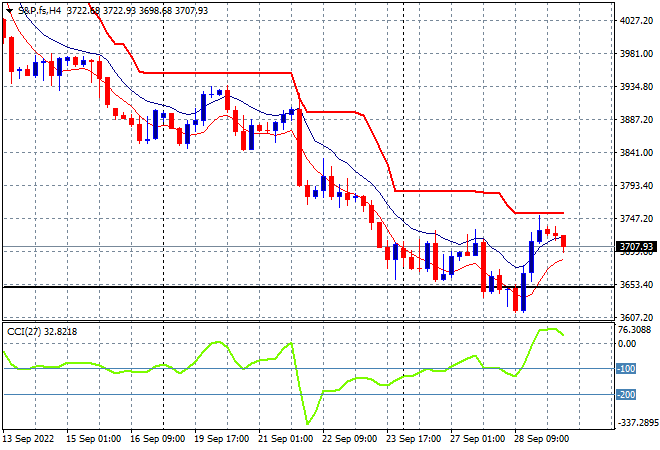

Eurostoxx and US futures are treading water with the latter pulling back a little as we go into the London session with the S&P500 four hourly futures chart showing price action retracing back to the 3700 point level. Medium term and possibly psychological long term resistance at the 4000 point level seems unattainable at the moment with support at 3800 points a distant memory, as price has been unable to get above trailing resistance:

The economic calendar will include the latest German CPI print, then the Q2 US GDP growth rate estimates.