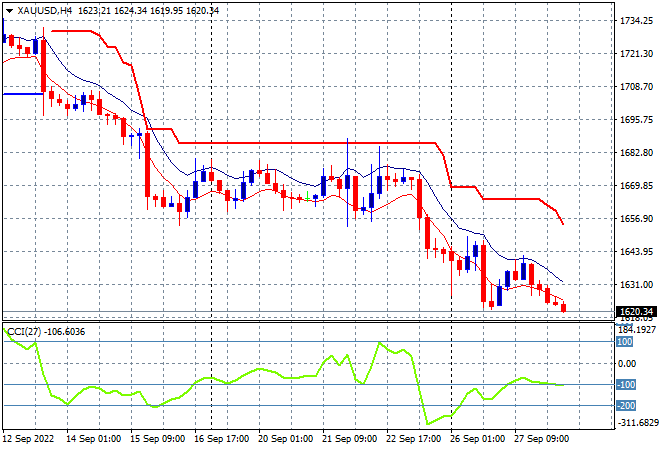

Another sea of red across Asian stock markets today following more overnight macro worries in Europe and a hawkish Fed amid rising interest rates and bond yields. The USD has regained all it lost (i.e not much) against the major currencies, as falls continue in Pound Sterling and Euro. Meanwhile oil prices are trying to stabilise with Brent crude hovering above the $83USD per barrel level while gold has returned to its poor start of week position, still crushed below former support at the $1700USD per ounce level, currently at $1620 at a two year low:

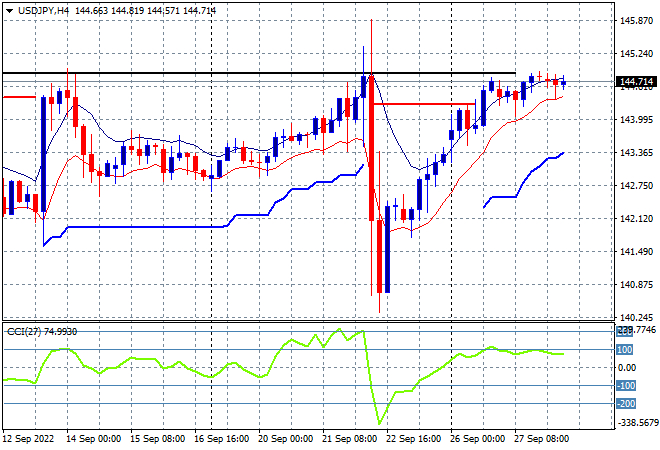

Mainland Chinese share markets have sold off sharply with the Shanghai Composite down 1.6% to 3045 points while the Hang Seng Index is getting crushed, down another 3% at 17225 points. Japanese stock markets also stumbled, with the Nikkei 225 closing some 1.5% lower at 26173 points while the USDJPY pair is treading water here despite other currencies lifting slightly against USD, still at its previous weekly high just below the 145 handle:

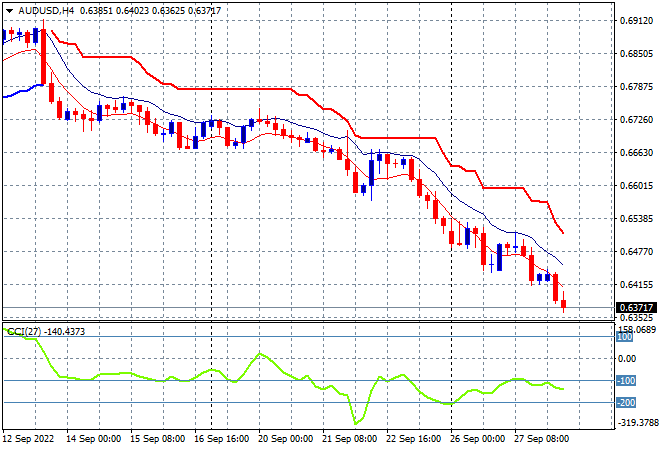

Australian stocks were the best in the region, all things being equal, with the ASX200 only losing 0.5% to close at the 6462 point level, hovering at a new monthly low. The Australian dollar also moved sharply lower despite the retail sales print, falling well below the 64 handle this afternoon as the four hourly chart shows this move gaining pace – 60 cents next?

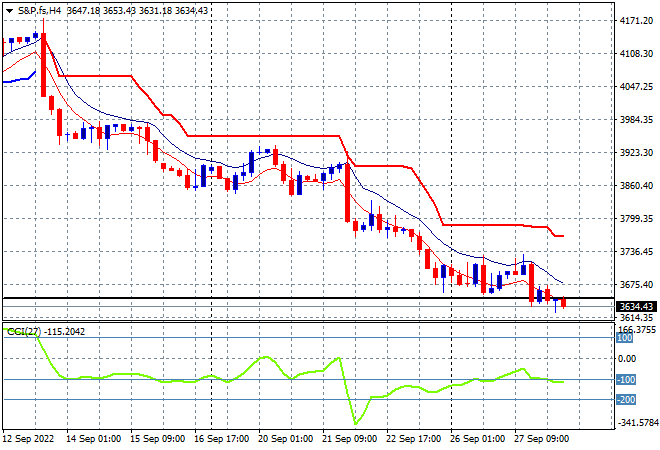

Eurostoxx and US futures are falling smartly as we go into the London session with the S&P500 four hourly futures chart showing price action distancing itself sharply away from the 3700 point level. Medium term and possibly psychological long term resistance at the 4000 point level seems unattainable at the moment with support at 3800 points a distant memory:

The economic calendar will include the latest German consumer confidence print, then US home sales with another speech by Fed Chair Powell to keep an ear out for…