A bunch of economists have warned that the Reserve Bank of Australia’s (RBA) aggressively monetary tightening will likely drive Australia into recession next year.

Leading the charge is Barrenjoey chief economist, Jo Masters, who says a recession is “on the cards” for Australia because the RBA will be forced to lift the official cash rate (OCR) to 3.35% in tandem with the US Federal Reserve:

“This will have economic consequences – weakening the growth outlook and seeing the unemployment rate lift,” [Masters] said.

“B*Eco modelling suggests this would drive the economy into recession.”

Westpac’s chief economist, Bill Evans, made similar arguments, claiming the stubborn outlook for high inflation and wages growth in the US, and rising interest rates globally, will force the RBA to lift interest rates to 3.6% early next year to stop the Australian dollar from losing value:

“The RBA governor would be concerned that such a sharp widening of the expected yield differential with global rates will have implications for a weaker Australian dollar complicating the inflation challenge.”

David Bassanese, chief economist at BetaShares, also mirrored these arguments.

Why does the RBA need to follow the Federal Reserve into recession by continuing to aggressively lift interest rates?

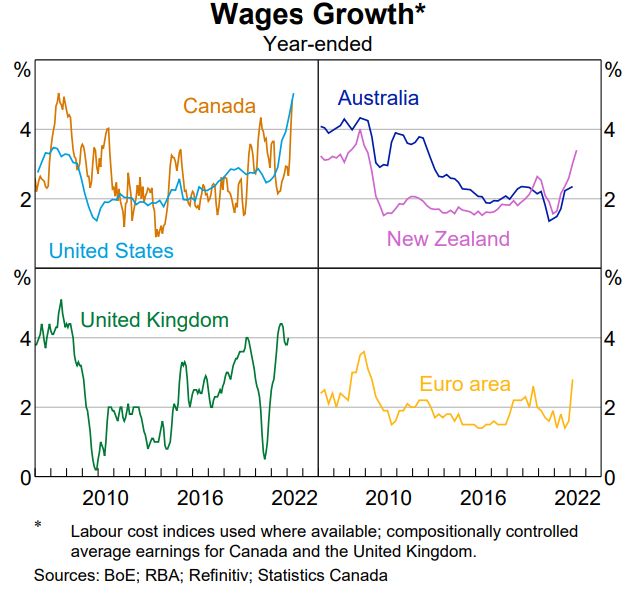

Australian wage growth is lagging way behind the US and other advanced nations, as illustrated clearly in the below RBA chart:

No wage-price spiral in Australia.

As such, there is no wage-price spiral in Australia, which negates the need for the RBA to hike rates aggressively.

In fact, Australian wages are growing well below the ~3.5% level the RBA previously nominated as consistent with inflation within the target band over the medium term.

The RBA also should not be concerned about a pending wage-price spiral in Australia, given the Albanese Government has just launched the biggest immigration program in the nation’s history, which will add massively to labour supply next year and crush any hopes of accelerating wage growth.

Let’s also not forget that around 40% of mortgages taken out over the pandemic were at one to three-year fixed rates at an average of ~2.25%. As these mortgages expire from late this year, borrowers will be pushed onto much higher (circa double) mortgage rates. Therefore, monetary conditions will tighten anyway in the absence of further rate hikes.

The Global economy is also facing recession next year on the back of soaring energy costs, aggressive central bank tightening and China, which negates the need for the RBA to continue tightening.

In any event, the best thing the RBA could do to temper inflation is pressure the federal government to sort the East Coast energy market out by delinking domestic gas and electricity prices from the global market. This could be done with the stroke of a pen via domestic gas reservation (as applied in Western Australia) and super profits taxes.

Most of Australia’s inflationary pressures are supply driven. So, address the problem directly by lowering the cost of domestic energy supply. It isn’t rocket science.