Love him or hate him, Chris Joye is Australia’s best housing prognosticator in Australia and the story he is now telling is spot on:

According to this newspaper’s economics editor, John Kehoe, national house price falls of more than 10 to 15 per cent “would likely make Reserve Bank of Australia governor Phil Lowe nervous” because of their impact on “consumer spending and housing construction”.

Many would speculate that Kehoe did not simply pull this opinion out of his behind: that is to say, this might be an accurate representation of the Martin Place mandarin’s otherwise precarious state of mind.

If that’s true, the RBA should be crapping its dacks.

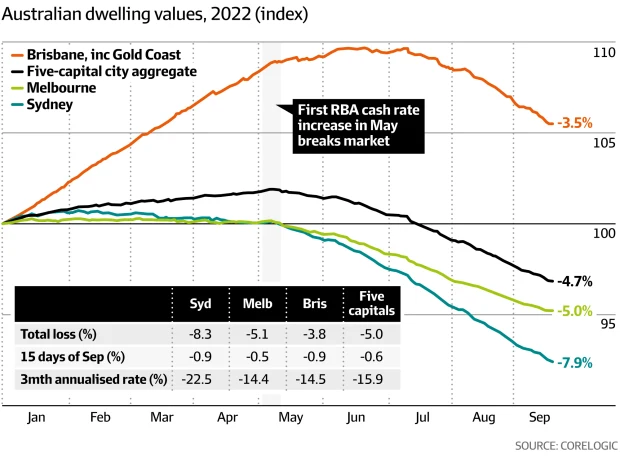

Yes, it should. The RBA has already massively overtightened. That it hasn’t become obvious in the economy yet should not distract from this fact. As Joye points out, the leading indicator for consumption activity, which drives 55% of GDP, is crashing at spectacular speed:

Joye goes on:

While our projection for a 15 to 25 per cent decline in prices explicitly allowed for a range of cash rate increases beyond the first 100 basis points, it did not countenance a much higher, circa 4 per cent cash rate.

In June, we published internal modelling that showed that if the RBA did raise its cash rate to, say, 4.25 per cent, the expected peak-to-trough loss in house prices would be greater, at 30 to 40 per cent. This is not, however, our central case, which remains a still remarkable 15 to 25 per cent retrenchment.

For perspective, remember that the peak to trough fall in US property values during the GFC was 27%.

That is what the RBA is toying with and it should, indeed, be “crapping its dacks” because nobody else is going to be blamed. Not even Albo’s cowards, who could avert it by fixing energy inflation.

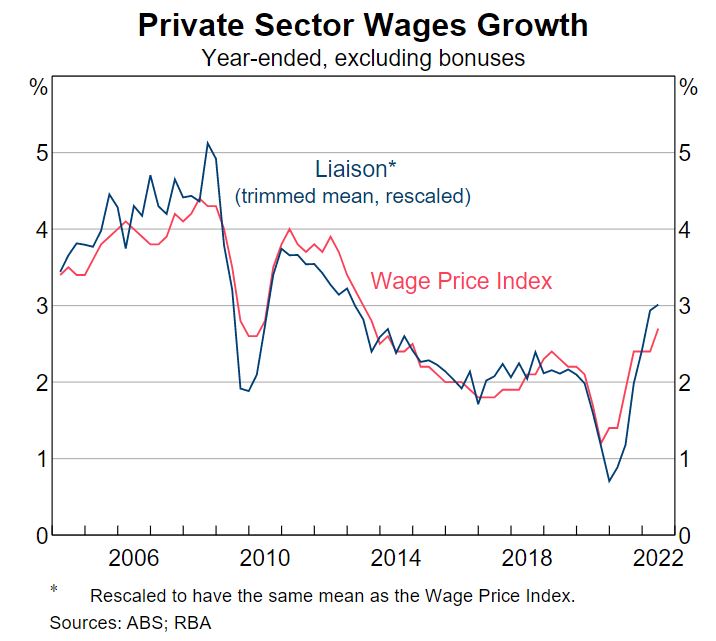

The radical RBA tightening makes even less sense when we examine new data from late last week. A few months before launching the most radical tightening of any DM central bank (faster even than the Fed, given it only meets every six weeks) the RBA said it would wait to see wage inflation data well above 3% in the hard numbers. Then it rolled suddenly based on the basis of its own internal soft data derived from “liaison”.

Late last week it released some of that data and it is damning as well:

The data clearly exaggerates the strength of prices on the way up and has not even reached 3% let alone the 4% the RBA says it needs for sustainable inflation.

Yet the RBA has already put a monetary clamp on households equal to that of the of the pre-GFC period when wages were running above 5%.

Australia should also be “crapping its dacks” being run by such inconsistent fools.