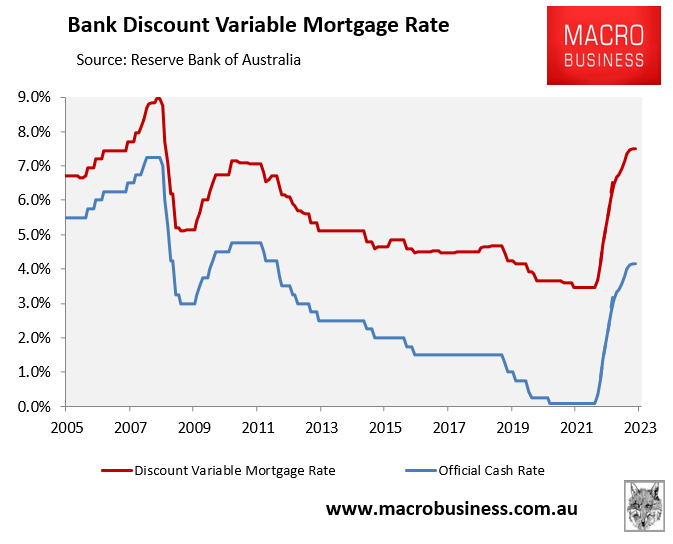

I noted yesterday how the bond market had aggressively lifted its interest rate expectations and now believes Australia’s official cash rate (OCR) will peak at 4.15% by mid 2023.

This would lift the average discount variable mortgage rate to 7.50% – more than double the 3.45% that presided in April before the Reserve Bank of Australia’s (RBA) first rate hike.

The bond market’s OCR forecast would drive mortgage rates to their highest level since October 2008.

This would be the highest discount variable mortgage rate since October 2008 and comes at a time when Australians are carrying record levels of mortgage and household debt.

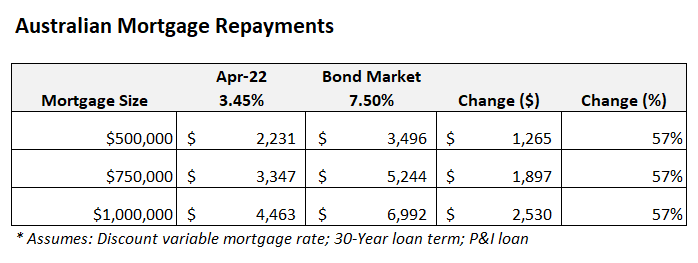

As illustrated in the next table, the bond market’s forecast would lift average variable mortgage repayments by 57% versus their pre-tightening level, adding $1,265 in monthly repayments to a $500,000 mortgage:

I described the bond market’s OCR forecast as “insane”, arguing that it would drive the economy into a harsh recession and crash the housing market.

AMP Capital’s chief economist, Dr Shane Oliver, has likewise described the bond market’s forecast as “crazy” for the same reasons:

“You lift the cash rate to that level, you drive the country into recession. You probably knock 30 per cent off house prices”.

“We’re talking about a two to two-and-a-half-fold increase in mortgage repayments for millions of people. This is tens of thousands of dollars worth of spending power taken out of the hands of consumers.”

Dr Oliver went on to explain that the bond market’s hawkish forecast is based on the US Federal Reserve’s aggressive monetary tightening. However, he argues there are major differences between Australia and the US, which negate the need for the RBA to tighten as aggressively.

In particular, most Americans are on 30-year fixed mortgage rates, whereas Australians are mostly on variable rates or short-term fixed rates. Australian households are also carrying around double the debt of Americans. Both factors make Australian households far more sensitive to interest rate hikes:

“The Fed is possibly making a huge policy mistake. It doesn’t mean we have to go over the same cliff here”, Dr Oliver said.

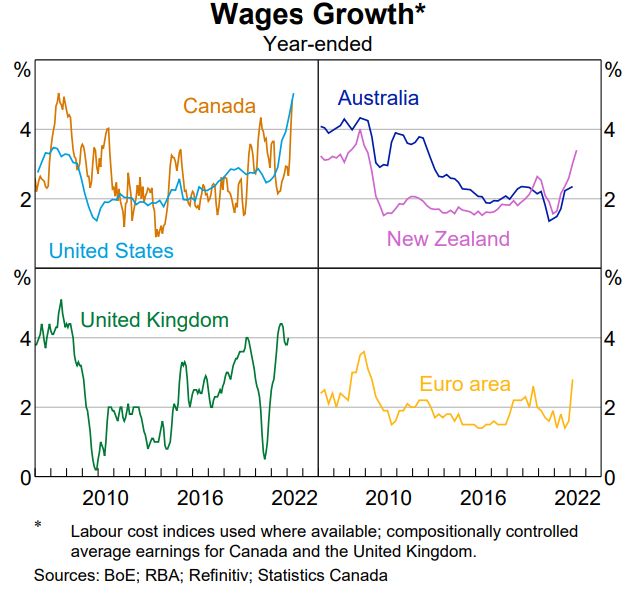

I will add that, unlike the US, Australia is not experiencing strong wage growth and is not at risk of a wage-price spiral:

Aussie wage growth is among the softest in the developed world.

In fact, Australian wages are growing well below the ~3.5% level the RBA previously nominated as consistent with inflation within the target band over the medium term.

Moreover, the Albanese Government has just launched the biggest immigration program in the nation’s history, which will add a massive amount of labour supply next year and crush any prospect of accelerating wage growth.

In short, the bond market’s OCR forecast is dangerously aggressive. If the RBA follows its lead, the Australian economy would be plunged into a painful and unnecessarily deep recession.

The RBA should ignore it and focus on the local economy.