The awesome Michael Wilson of Morgan Stanley gives us a one-two punch this week.

Can You Hear Me Now?

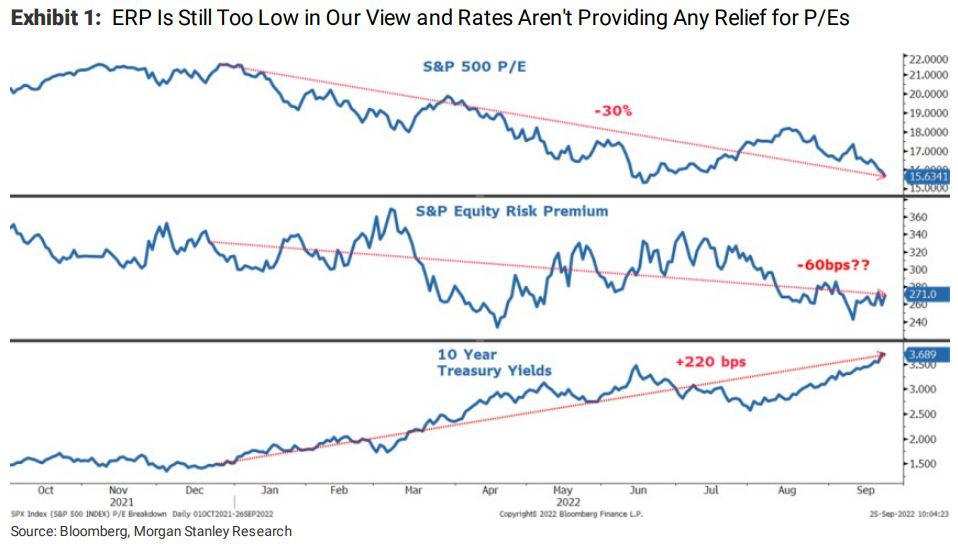

Last week’s Fed meeting gave us the 75bps hike most investors were expecting and similar messaging to what we heard at Jackson Hole a month ago – i.e., the Fed means business with inflation and is willing to do whatever it takes to combat it. So why such a dramatic reaction in the bond and stock markets? Were investors still hoping a dovish Fed would return? Whatever the reason, both stocks and bonds are right back to their lows in June with many bellwether stocks and Treasuries even lower. As we wrote a few weeks ago, we think investor hopes for a Fed pivot were misplaced,and Chair Powell has certainly made that crystal clear the past few times he has spoken. It appears investors have finally gotten the message and hear him clearly now. Secondly, we noted last week that the only remaininghope for stocks would be if the bond market rallied at the back end on the view the Fed was finally ahead of the curve and would win its war on inflation, while slowing the economy materially. Instead, back end rates spiked higher, squelching any hopes of multiple expansion (Exhibit 1). While 15.6x is back to the June lows, that P/E still embeds what we think is a completely mispriced Equity Risk Premium given the rising risk to earnings. As discussed here many times, when growth is decelerating as it is today, the ERP is typically higher than average,not lower. Using our model to predict ERP suggests it’s off by ~100bps today,and that’s before the PMI and other key variables have fallen to levels we expect over the next few months. Suffice it to say, that argues for a P/E that is ~2turns lower given the level of 10-year yields.