In 2009, I chose the nom de plume Houses and Holes because it fit so beautifully with Australian economic structure.

We dig holes and export the dirt. Then we leverage that income in global markets via the major banks who, in turn, overlend into mortgages at home.

This produces the world’s most objectionable property price bubble which supports the over-consumption of services.

Over time, the model has led to the hollowing out of everything productive that is not nailed down.

Advertisement

For more than ten years, Leith and I have lobbied to change the system via reform. We did not want to crash it because that would punish too many innocents. Moreover, our assessment was that it was possible to restore Australian competitiveness without destroying the lifestyles of Australians. A utilitarian calcualtion.

We’ve had some notable successes. Forcing APRA to do macroprudential. Forcing a rethink on immigration within the RBA and some parts of Canberra. Keeping the flame of better taxation for mining alive. Helping keep the AUD much lower than it would be otherwise. Holding the China grovellers to account.

But, overall, we’ve failed. Of course, we have. A little blog can’t compete with the untold billions of mining and banks. Especially so, since Canberra is not much evolved beyond the culture of the Rum Corps. Hundreds of years of deadshits seeking their infinnitessimal snifter of the action.

Advertisement

Thus, the Aussie economy has become ever more unbalanced with rapacious mining occupying ever more productive capacity and political economy space, and banks received scales of public support unthinkable 13 years ago.

But, now we’ve come to a point of crisis in which it is all so unbalanced that the holes half of the equation is engulfing the houses half. Either the interests that used to bulwark the bubble do not understand the perilousness of their situation, or they are outmatched by the holes in political economy terms.

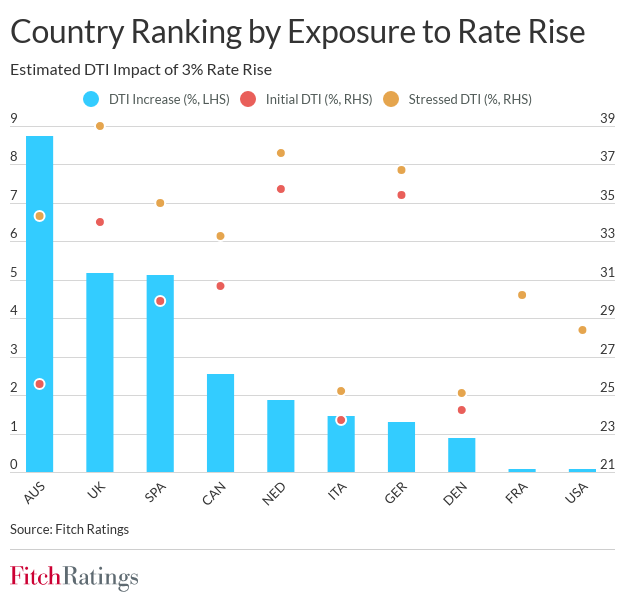

What am ranting about? This, via Fitch:

Advertisement

The share of variable rate residential loans and borrowers’ current debt-to-income (DTI) ratios give an indication of the relative exposure of RMBS and covered bond (CVB) markets to rising interest rates, Fitch Ratings says in a new report. Australia, Spain and the UK appear most vulnerable: exposure in Australia and Spain stems from the high proportion of variable rate lending, while borrowers in the UK have a relatively high DTI.

Fitch stress-tested the market average DTI ratio (monthly cost of debt service over monthly disposable income) for loans originated in 2020, assuming the rates payable on variable-rate loans increased by 3pp above their original rate by end-2023, while keeping income unchanged. Our ranking shows relative vulnerabilities based on average DTI due to the presence of variable-rate loans (floating rate loans for life and loans where the existing fixed rate will expire or reset within the next 24 months), and how far lower DTIs cushion these borrowers.

While this assesses the vulnerability to one variable, in practice changing incomes would also affect DTIs, for example if inflation eroded real incomes or rising rates depressed economic growth, pressuring salaries. Fitch also acknowledges that average DTI does not capture differences in DTI distributions that will affect credit performance. We examined the 2020 vintage, which we consider a good proxy for loans that could be included in forthcoming RMBS and CVB portfolios but is not representative of the entire mortgage market stock.

Variable-rate loans in the Netherlands, Germany and the UK appear the most sensitive because of high current DTIs. But overall, considering both variable and fixed-rate loans, borrowers in Australia, Spain and the UK would experience the most significant payment shocks in our scenario, measured by the relative increase in the stressed versus original DTI.

If it was not bad enough, note, espeically this sentence: “While this assesses the vulnerability to one variable, in practice changing incomes would also affect DTIs, for example if inflation eroded real incomes or rising rates depressed economic growth, pressuring salaries.”.

Here is the rub. The new Labor government is the most pro-holes in Australian history. Mining has groomed it par excellence. It threw the ALP out of power last time they were in, bankrolled the Coalition ever since, and has ensured a new Albanese Government controlled by a shovel in its butt.

As such, when the worst energy shock in Australian history landed on our shores pot-Ukraine War, Albo’s shovel-puppets protected the miners, not the people and the end result is now emerging for all to see:

Advertisement

Inflation is here. The first wave was COVID supply-side disruptions. But we could have shrugged that off. The deeper real income shock is ahead and it is all about holes.

The local gas price is still at nosebleed levels roughly 800% above the historical average and 400% above the pre-Ukraine War price:

Advertisement

Coal is at records as well above $400 per tonne, up 500% from pre-Ukraine War prices.

We produce both for next-to-nothing but the Albanese Government is captured by holes and is not acting to sever the link to international prices for domestic users.

Advertisement

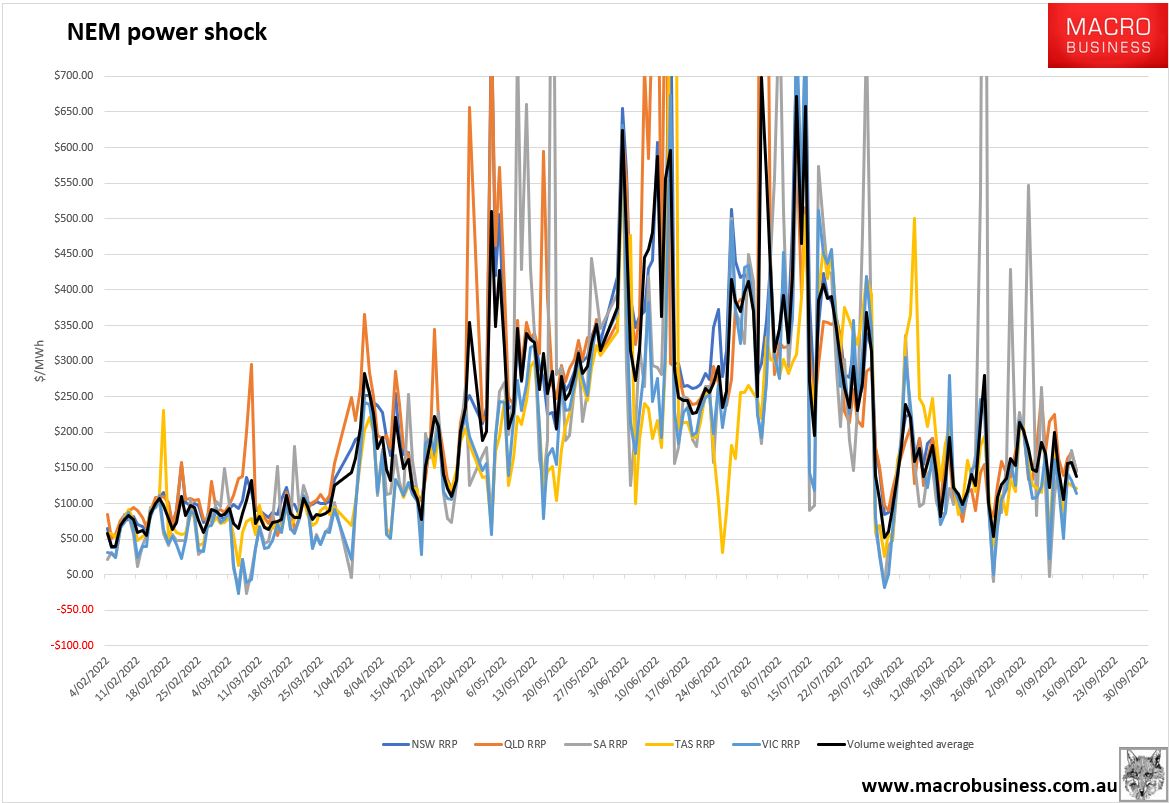

Hence, there’s no relief in power prices, either:

Combined, this is going to add 2.5% to the CPI over the next year and close to double that over two years as spillover prices follow.

By allowing foreign-owned energy cartels in coal and gas to determine local prices for electricity, Albo’s mining cowards have ensured a historic real income shock lasting years that will send houses into a fatal decline with rising interest rates, which will then hammer incomes again as the recession takes hold.

Advertisement

To simplify, the system used to work like this: mining boom lifts incomes > house prices, consumption and interest rates rise > mining income crashes with recession but houses take off with falling rates.

Now it works like this: mining boom kills incomes and house prices > interest rates rise on energy shocks > mining income and house prices fall through easing rates.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.