Pantheon with the note. I don’t think so. Restarting stalled projects is one thing. Overturning “houses are for living in not speculation” is another. But you never know your luck in the big city!

Property Stimulus Starts to Show in the Data, but Much More is Needed

China’s property sector is yet to pull out of its nosedive, despite the rollout of bailout funds for stalled projects. Transactions, construction, and prices are all still falling, and stress in the developer sector is increasingly spilling over into the rest of the economy. The drag on growth is likely to intensify as we head into Q4, absent a stronger policy response. New bailout funds are seemingly announced every day, however, and reportedly are now sufficient to restart all stalled construction, raising the tantalising prospect that the sector will finally bottom out by the end of 2022.

Residential property sales and starts continued to fall in August, extending the worst spell for the market on record. The 12-month-on-12-month growth rate—which we prefer because it deals with distortions introduced by Covid lockdowns—fell to -26.1% for sales values, from -25.9% in July, with volumes dropping 23.6%, from -23.1% previously. New starts fell 33.6%, from -30.9%, with total residential property under construction falling 6.8%, from -6.1%. In all cases, this is the worst month on record, as shown in our first chart. Prices also continued to fall in August, for the twelfth consecutive month.

A lack of confidence in developers—many of which are in default, or otherwise struggling to proceed with construction—is a key driver of the weakness in sales. This is evident in the plunge in pre-sales, against relative stability in sales of existing property; fear that developers will fail before completing a new project provides a powerful reason not to pay in advance. The dominance of pre-sales—even now—also illustrates the Ponzi-like product Chinese property has become, and how reliant it is on hope.

A lack of confidence amongst borrowers has knock on effects for other sectors, too. A mortgage boycott which started two months ago is again threatening to intensify as construction remains stalled, according to Reuters, which adds to the woes of China’s financial system, already suffering from its direct exposure to property developers.

Real estate developers are also reportedly defaulting on their commercial paper. A report from the CRIC Research Center showed the number of firms not repaying unsecured debt obligations jumped 40% year-over-year in August, spreading the pain to their suppliers, with building materials, decoration, and furniture firms in turn reporting increasing credit impairment losses, up 37% year-over-year. This must inevitably lead to lower investment and hiring by these firms, alongside further losses in the financial sector.

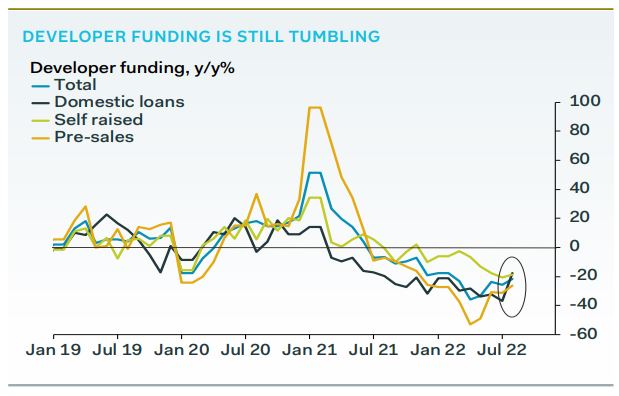

Unfortunately, China is caught in a vicious cycle. Confidence in property developers can be restored only if construction resumes, debts are paid, and their long-term survival seems assured. But for that to happen, developers need money, and they are—or were—heavily reliant on revenues from pre-sold properties, and debt financing. The property bailout funds aim to break this feedback loop, using government balance sheets to restart stalled construction. August credit data showed some signs that these funds were being rolled out, as shadow financing and corporate lending rose—a mix of entrusted loans by SOEs, and local government financing vehicles borrowing—and we think the improvement in domestic loans to developers shows these funds are reaching their intended targets.

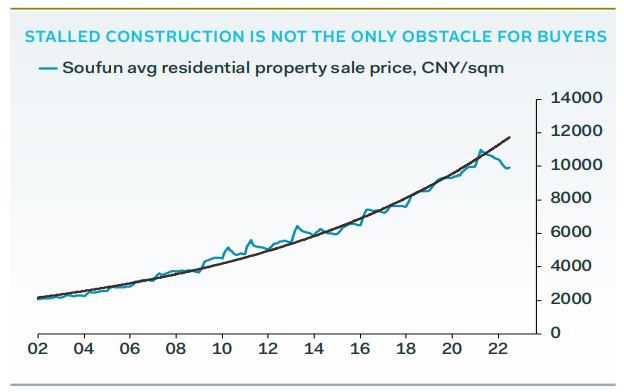

We still have a long way to go, however, with developer funding growth still in deeply negative territory. Local governments are rolling out their own bailout funds, to complement the RMB 200B from the central government, and some reports suggest the total may be enough to cover the cost of restarting all stalled projects. If true, this would be an important first step in providing a floor for the sector, restoring confidence and boosting developer cashflow. We suspect, even so, that unchecked demand will not return; no longer can homebuyers assume rapid and perpetual increases in prices, as in the past. The very clear break in trend price growth— shown in our chart below—will force a reassessment of property as an investment.

We are somewhat sceptical, however, that the bailout funds will prove sufficient, given the squeezed position of local government finances. Land acquisitions by LGFVs jumped 70% year-over-year in H1, which essentially represents off-balance sheet borrowing by local governments, selling land to themselves. We suspect that many local governments will ultimately prove unable to support their regional property markets without further help from the centre.