Goldman Sachs with the note:

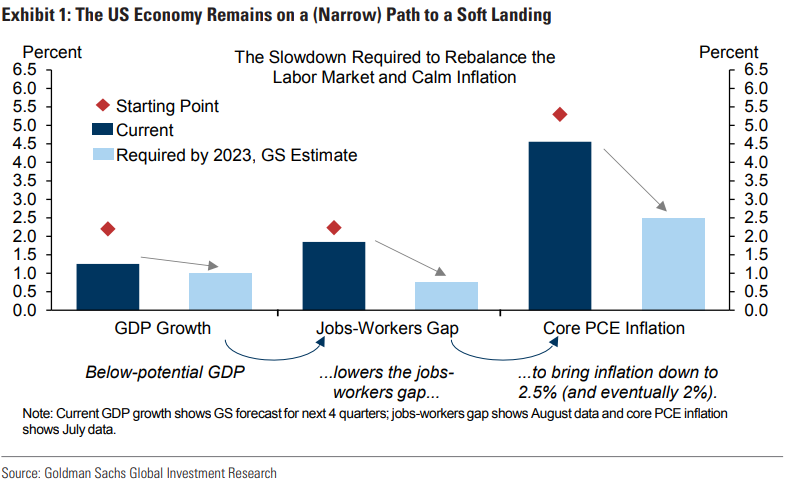

1. Since the FOMC started hiking the funds rate early this year, we have argued that the US economy can achieve a soft landing, even though the path is narrow. It requires sustained below-trend output growth, a rebalancing of the labor market via sharply lower job openings coupled with a moderate rise in unemployment, and a large decline in inflation. While much can still go wrong and our probability that a (mild) recession will start in the next year remains about one in three, we see some encouraging signs that the economy is moving toward all three of these goals.

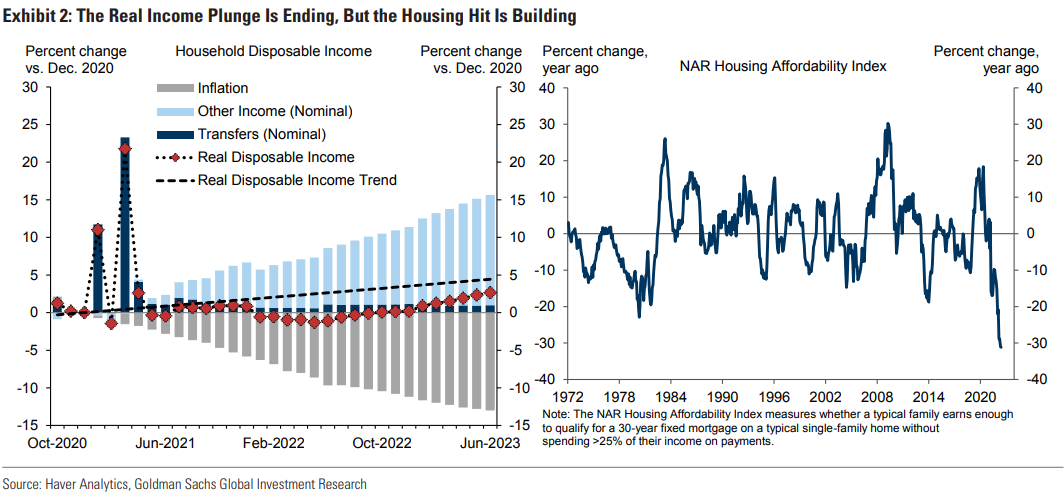

2. The growth adjustment is furthest advanced. The initial slowdown in early 2022 came in response to the biggest decline in real disposable personal income in postwar history, driven by reduced fiscal support and much higher food and energy prices. This hit has largely run its course, as the fiscal tightening is now behind us and the renewed decline in energy prices has started to support real income. However, the drag from financial conditions is still building. The most important channel is the 300bp increase in 30-year mortgage rates to just over 6%, which has led to the sharpest decline in housing affordability on record. This will deliver a notable blow to residential construction activity and is also likely to weigh on consumption via lower real house prices. All told, we remain comfortable with our forecast that US growth will remain well below trend over the next year.

The full text of this article is available to MacroBusiness subscribers