Here’s Professor Ross Garnaut’s keynote address from the Jobs and Skills Destruction Summit:

We are kidding ourselves about how well our economy is performing, absolutely and relative to other developed countries. True, for nearly three decades from 1991 we experienced the longest economic expansion unbroken by recession of any developed country, ever. That ended in the first half of 2020.

In late 2020 and early 2021, our economy bounced back more quickly from pandemic recession than most developed countries, because our fiscal expansion was bigger and faster. Since then, we have looked ordinary in a troubled developed world.

Our 28 years of economic expansion were not uniformly good. Through the first decade, we had the strongest productivity growth in the developed world. For the next decade, through the China resources boom, we experienced large increases in average incomes despite lower productivity growth.

In the Dog Days from 2013 to the pandemic, productivity, wages and median incomes grew less than in other developed democracies. Unemployment moved from being well below to well above the US.

We can’t turn the economy back to before the pandemic. Even if we could, pre-pandemic conditions are not good enough. That’s high unemployment and underemployment and stagnant living standards.

The problems from the Dog Days and the pandemic have been compounded by the Russian invasion of the Ukraine and its disruption of global energy markets. Unlike Western Europe and north-east Asia, Australia as a geographic entity has higher terms of trade when gas and coal prices rise. But under current policies, average Australians are poorer.

We are kidding ourselves if we think no deep wounds will be left in our polity from high coal and gas and therefore electricity prices bringing record profits for companies, and substantially lower living standards to most Australians.

We have to stop kidding ourselves about the budget. We need unquestionably strong public finances to have low cost of capital, private and public, for our superpower transformation, and to shield us from a disturbed international economy and geopolity.

Yet we have emerged from the pandemic with historically large budget deficits in the Commonwealth and most states and peacetime record highs of public debt. We have large deficits when our high terms of trade should be driving surpluses. Interest rates are rising on the eye-watering Commonwealth debt.

We talk about the most difficult geostrategic environment since the 1940s requiring much higher defence expenditure, but not about higher taxes to pay for it. We say we are under-providing for care and underpaying nurses, and under-providing for education and failing to adequately reward our teachers.

The most recent Treasury intergenerational report update tells us that the ratio of over-65 to conventionally work-age population will rise by half over the next four decades, bringing higher costs and fewer workers to carry them.

In the face of these immense budget challenges, total federal and state taxation revenue as a share of GDP is 5.7 per cent lower than the developed country average.

Let’s stop kidding ourselves.

The Pre-election Economic and Fiscal Outlook was released four months ago, to inform the discussion of economic policy during the election campaign. It said that average real wages would decline by 3 per cent in the two years to next June. By the time of the Treasurer’s statement three months later, the expected decline had increased to 7 per cent.

We should see the statement not as a forecast of the future, but as a warning of dangers to be avoided.

The facts have changed, and we should be ready to change our minds.

When we stop kidding ourselves, we will recognise the need for policies that we now think impossible.

The realities facing Australia are much more dangerous than revealed to the electorate in May this year. But the zero carbon opportunities are much richer. Policy will need to change more than we thought necessary, and more than we think possible.

But stop kidding ourselves, make the necessary impossible changes in policy, prepare thoroughly to build the zero emissions superpower, and we can have full employment with rising incomes and the right amount of debt for a long period ahead.

In this successful Australia, rising standards of living will rely less on regulated wages and more on fiscal transfers than in the past.

We have to raise much more revenue while increasing labour force participation and investment. I suggest for consideration two reforms from my book Reset. On taxation of personal income, Australian Income Security, based on guaranteed minimum payments and lower marginal effective taxation rates, would supplement low wages while encouraging participation.

On taxation of corporate income, using cash flow rather than accounting income as the tax base increases incentives for business innovation and investment without reducing total revenue. It shifts the burden from normal income in competitive parts of the economy to economic rent.

These two reforms would increase the budget deficit in the short term, which fitted perfectly the fiscal expansion required during the pandemic recession. That opportunity has passed, but the longer term case for the changes is stronger than ever. After a while, increased labour force participation would claw back part, but not all, of the initial revenue loss from Australian Income Security.

Sooner rather than later, the efficiency gains from the new corporate tax base would return all of and then more than the lost revenue. Our debt requires us to make good any loss of revenue.

There are many opportunities for raising additional revenue in Australia while enhancing equity and improving or at least not damaging economic efficiency. The mineral rent taxation is just one of them.

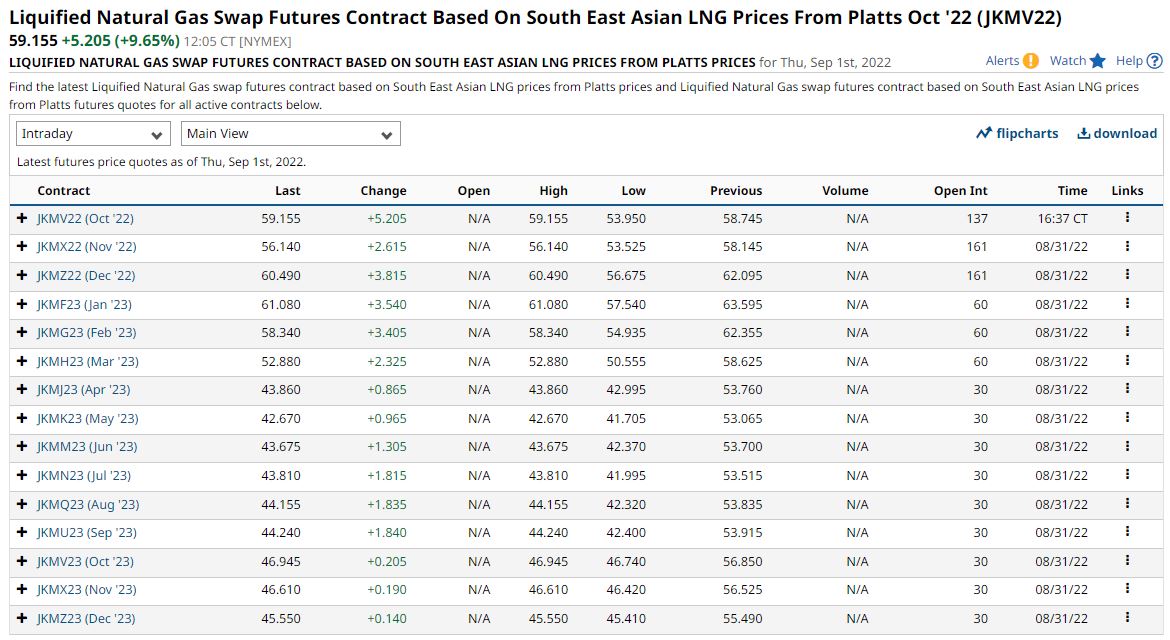

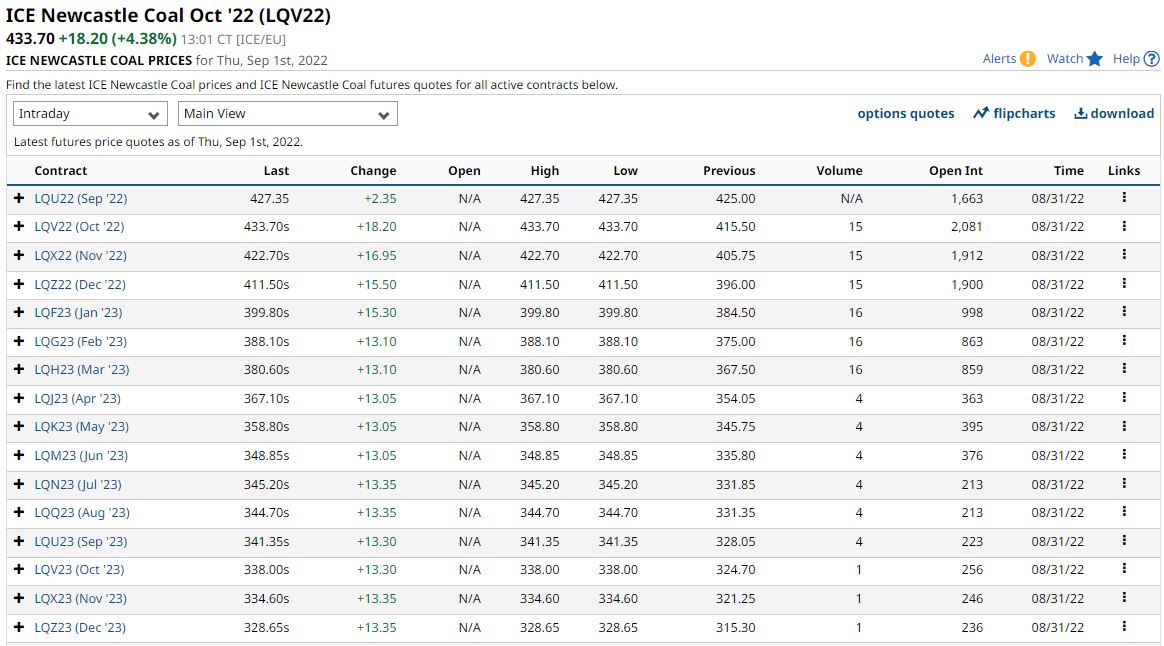

All sounds good to me. The energy cartels must be reined in. The international prices for gas and coal remain at nosebleed levels:

If the cartels import these prices, and they will try, then local electricity prices will rise to over $1000MW/h, utility bills will rise 700%, and the CPI climb by 20% in the next year with more the following.

In short, Albo’s cowards must act and either apply low-priced domestic reservation on coal and gas or, even better, an export levy benchmarked to pre-Ukraine prices.

I can only hope that Professor’s Garnaut’s appearance at the Summit signifies a shift in thinking among Albo’s cowards towards these ideas.