For the last year, all I have heard from China pundits is that its property market will eventually be saved. They have been non-stop wrong.

China’s property market has not bottomed. Authorities have been slow to react and did little when they moved. The overriding ideological shift coming from Beijing – of Common Prosperity and “houses are for living in, not speculation” – is intact. Worse, the underlying driver of the policy shift, deteriorating demographics, has only fallen away faster than expected.

Some months ago I declared that we are past the tipping point in this market adjustment. By that, I meant it was now self-fulfilling. Expectations and psychology are broken. Neither buyers nor developers have any desire to leverage up into an asset class that is being sat on by Beijing forever more, even if it is fed short-term stimulus.

Chinese property is caught in a classic liquidity trap and the adjustment to property price and construction volumes is irreversible and structural.

Friday gave us the latest round of evidence that being bearish about Chinese property is still the base case.

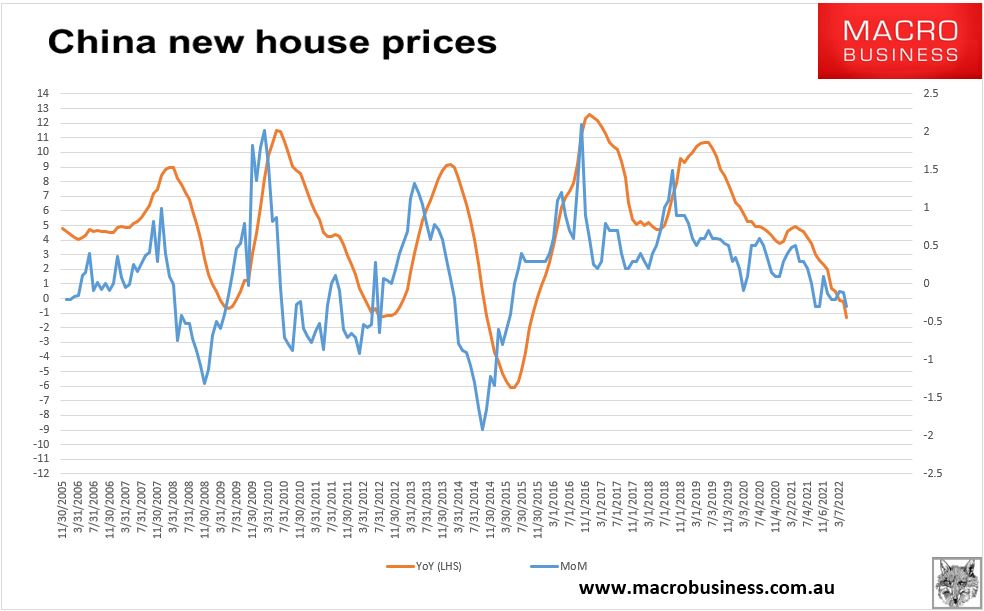

Despite months of easy credit, mortgage rate cuts, huge macroprudential loosening, bailouts for developers and striking mortgagees, prices are still falling 0.3% per month and down -1.3% over the year:

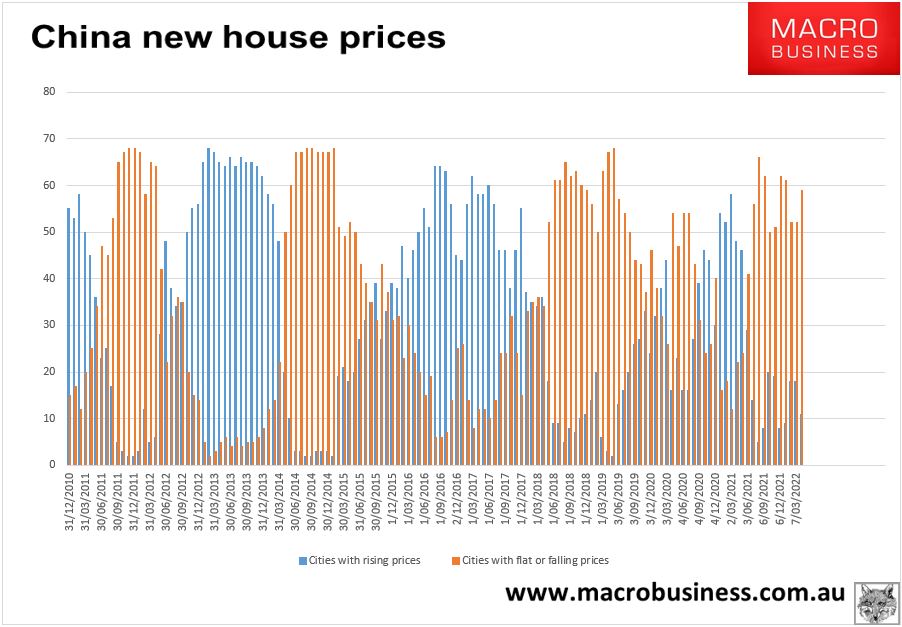

The composition of price movements is salient. The correction is broad-based:

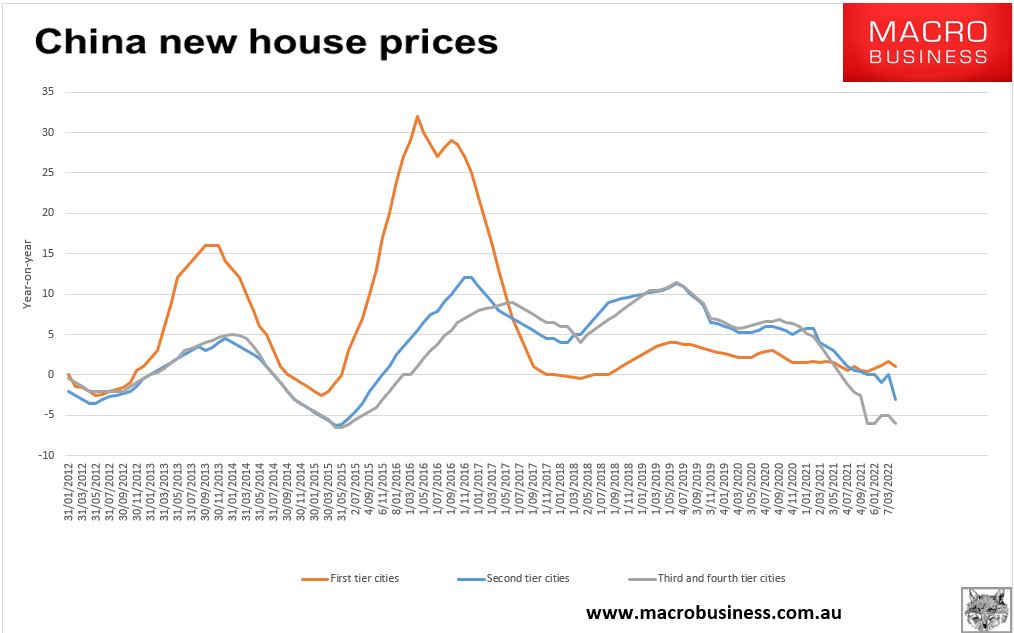

But much more intense in the lower tier cities where 70% of construction transpires and enormous volumes of unsold, unfinished, and untenable sky-scrapers are piling up and losing value:

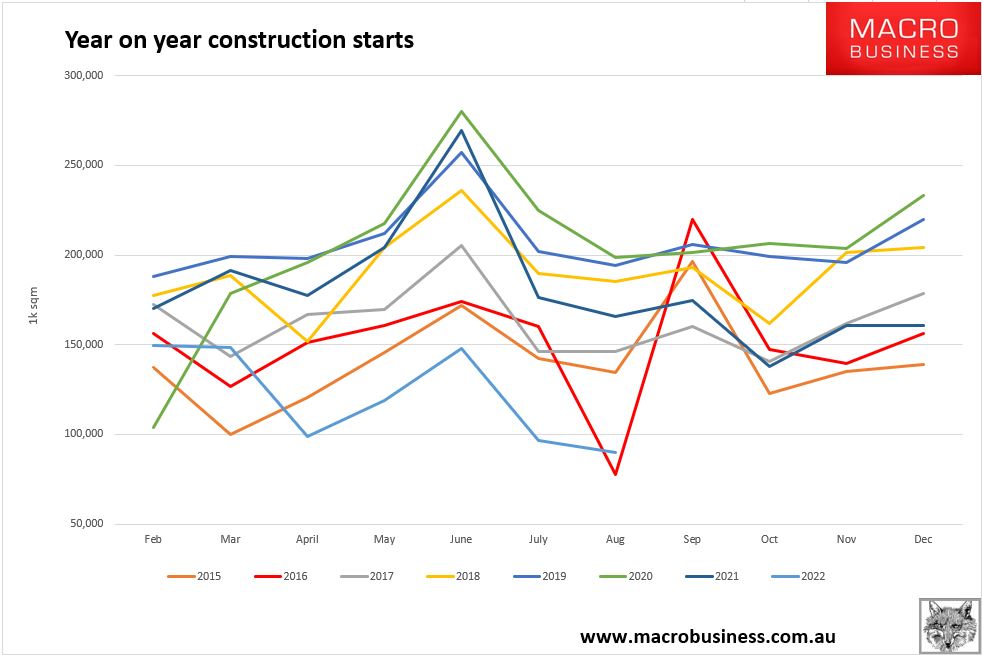

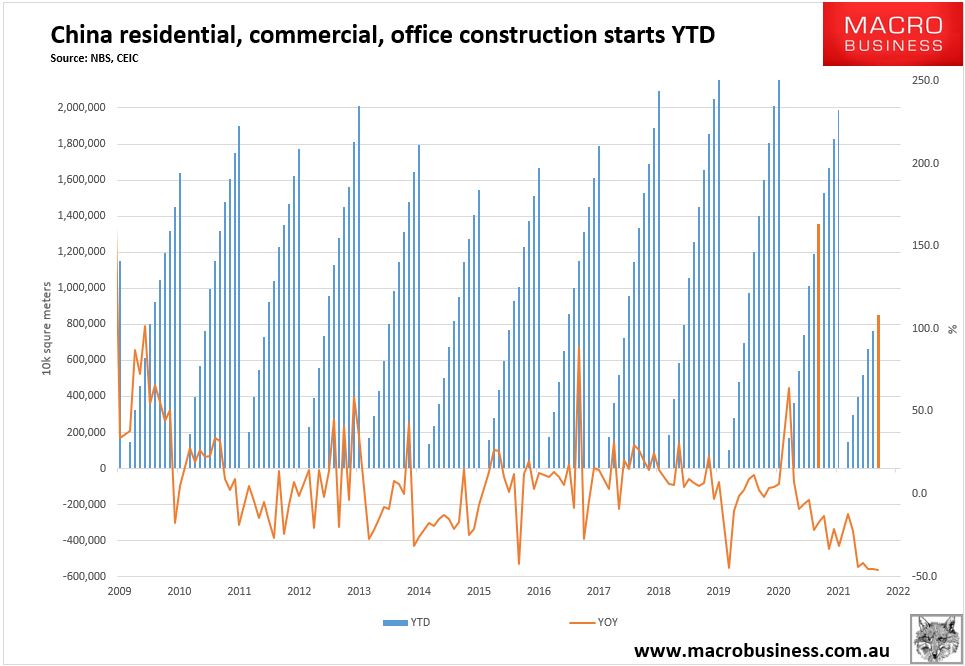

Weak prices are dwarfed by falling volumes of floor area sales and starts. Friday’s NBS data showed starts continue to trend down at -45% year on year in August, roughly half their 2021 COVID peak:

Year-to-date is down 37%:

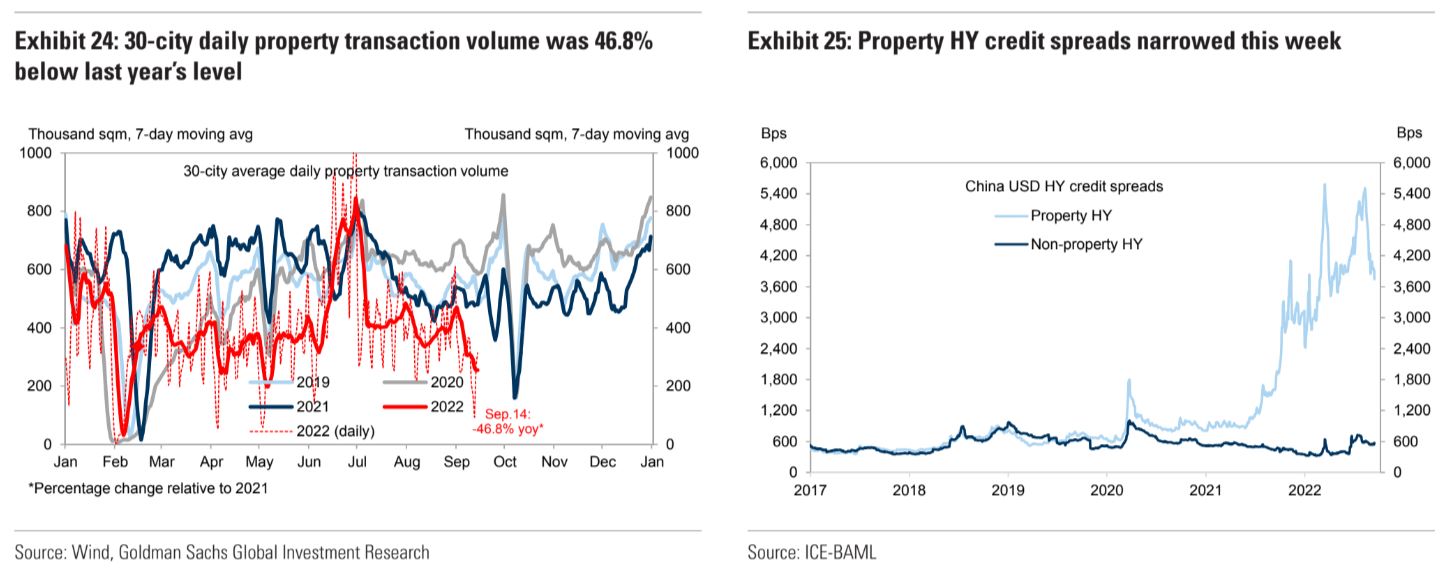

The leading indicators are worse. Real-time sales volumes are down by nearly half from 2021 and are running at about one-third of COVID peaks. Developer funding remains frozen:

Moreover, the key leading indicator for the whole market, land sales to developers, also remains down by half over the year and by about two-thirds over two. These are staggering numbers.

More support will be forthcoming but the market is beyond that. The one supportive measure I can see that might make a marginal difference is the lifting of zero-COVID which may or may not happen but won’t fix it, either way.

Those arguing that there will not be a global recession because there are no great economic imbalances to adjust are looking in the wrong place. The world’s largest construction market (by so far that second is irrelevant) is in a nuclear meltdown that will spread fallout lasting longer than human lifespans. China’s publically-owned banks can doubtless survive the bad debt flood headed their way, but they can’t reverse it. The direct implication is that the Chinese economy is going ex-growth vis Japan in 1989.

Anything exposed to this burgeoning mushroom cloud – commodities, EMs, CNY, AUD, and global inflation – is going to be turned to ash.