Pantheon with the note. The recovery in Chinese credit has stalled with the structural property adjustment. Inflation is about to turn deep deflation.

In one line: No sign of China’s liquidity trap easing up

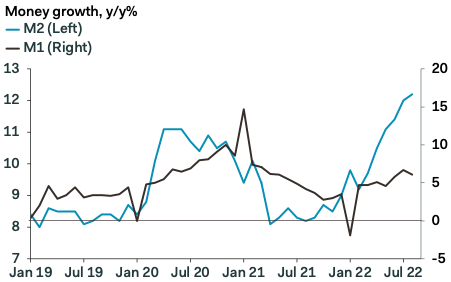

- M1 growth slowed to 6.1% in August, from 6.7% in July. Consensus was 6.9%.

- M2 growth rose to 12.2% y/y in August, from 12.0% in July. Consensus was 12.2%.

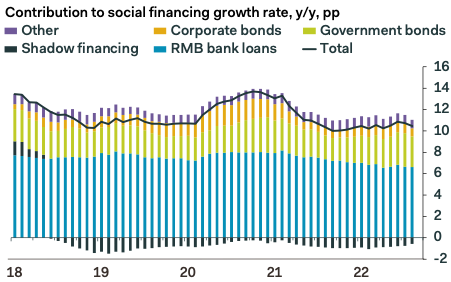

- Aggregate financing rose to RMB 2430.0B in August, from RMB 756.1B in July. Consensus was RMB 2075.0B

- New loans rose to RMB 1250B in August, from RMB 679.0B in July. Consensus was RMB 679.0B

The latest money and credit data suggest China is still suffering a liquidity trap, despite the rise in lending. The money supply data shows liquidity is still being pumped into the system; alongside the growing divergence in y/y rates, M2 rose 1.0% m/m, seasonally adjusted, for the sixth month in a row, while M1 was unchanged on the same basis. Broadly speaking, this means cash is flowing into bank accounts, and then sitting there, unused.

On the credit side, ASF growth slowed in August, to 10.5% y/y, from 10.7% in July. Every major component – loans, corporate bonds, government bonds – saw slower growth, with the exception of shadow financing, as bankers’ acceptances and entrusted loan growth picked up. This illustrates the risk of easing when facing a liquidity trap – private sector demand for loans is falling, but so much liquidity has been pumped in that it is starting to leak out into a shadow finance sector which, until earlier this year, had been shrinking faster and faster. Lending to households continued to slow, including for mortgages, suggesting no relief yet for the property market, despite recent rate cuts and ongoing efforts to restore a measure of confidence. Slower government bond issuance is also a worry, in that it means local governments are tapped out – though they have been granted a small additional quota for issuance by October – with little to show for it on the growth front.

As we have argued before, monetary policy looks largely played out, and additional easing will bring few benefits at this point, particularly with the renminbi already under pressure.

Inflation is on the slide with the economy. Pantheon again.

A Miss for Chinese Inflation, as a Lukewarm Economy Cools Further

Chinese inflation slowed more than expected in August, in a sign that domestic demand remains weak. The price data give no indication that stimulus efforts have revived the economy, and we expect further declines in September and October, given the tightening zero-Covid restrictions, which will squeeze demand and put pressure on core inflation. On the bright side, China will likely start exporting deflation sooner than we expected.

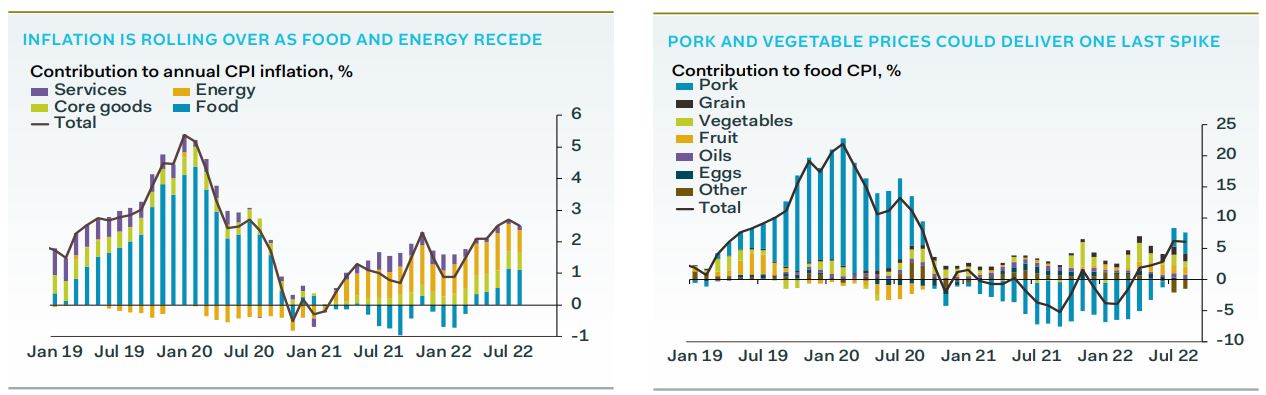

Chinese CPI inflation fell to 2.5% year-over-year in August, from 2.7% in July, driven chiefly by food and energy prices. Core inflation was unchanged, at 0.8% year-over-year, suggesting minimal demand pressure on prices. Nor is currency weakness creating

any inflationary problems for China, likely because producers lack any pricing power in this environment, reflected also by the fall in profits in July.

We think inflation is likely to fall further. Core and services inflation must contend with tightening zeroCovid restrictions, which typically choke consumption demand. These restrictions seem unlikely to ease until after the 20th Congress, which ends in late-October.

Energy inflation should also continue to fall. China does not report this directly, but utilities inflation fell to 3.4% year-over-year in August, from 3.6%, and fuel inflation slowed to 19.9%, from 24.2%. Our estimate of overall energy inflation, meanwhile, declined to 11.1%, from 13.4%. Further declines seem inevitable, given base effects, the end of China’s domestic energy crisis, and falling global oil prices.

The one wild card is food inflation, which fell in August, to 6.1% from 6.3%, thanks to a sharp drop in vegetable inflation. Pork prices, however, remain elevated, and the combination of lockdowns and forthcoming holidays tends to put pressure on fresh food and pork prices alike; both spiked in the first week of September, and pork is now at its most expensive since May 2021.

Surging food prices, however, tend to draw government attention. Central and local governments have started releasing pork reserves into the market to ensure supplies and limit price increases, with pig farms “advised” to sell at a normal pace, and firms also required to release commercial reserves. This is a recent development, so we will need to wait at least a week before knowing whether it has impacted prices, but we expect some success in limiting pork inflation.

Deflation is on its way

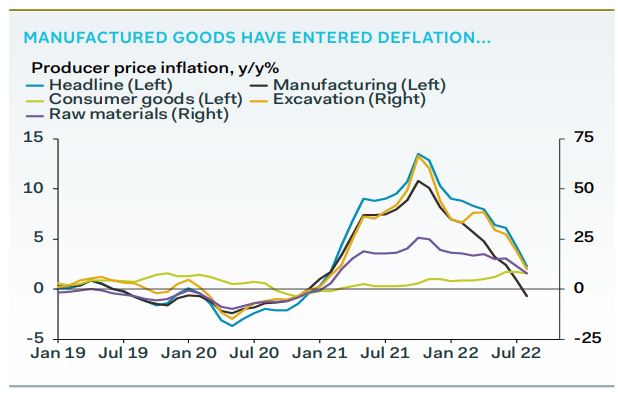

Chinese PPI inflation plunged to 2.3% year-overyear in August, down from 4.2% in July and well below consensus expectations. The fall was led by another dramatic drop in mining inflation, to 10.1% yearover-year, from 18.8%, reflecting both global energy prices and a favourable base effect from last year’s domestic thermal energy crisis. Coal mining inflation saw an even sharper decline, to 8.6%, from 20.7%. We should see this trend continue, particularly now that the recent limited energy shortages linked to regional droughts have been resolved.

Other producer inflation also slowed, with raw material prices echoing the global experience. China of course is a key player in global markets for many commodities, so this is as much a demand story as it is one of supply. The weaker-than-expected outturn of mining and raw material inflation suggests China’s industrial economy continues to falter, despite modest stimulus efforts. As we have argued before, the lack of policy support for demand, paired with subsidies for production, is highly disinflationary. Infrastructure spending is evidently falling short of making up for the ongoing decline of the property sector.

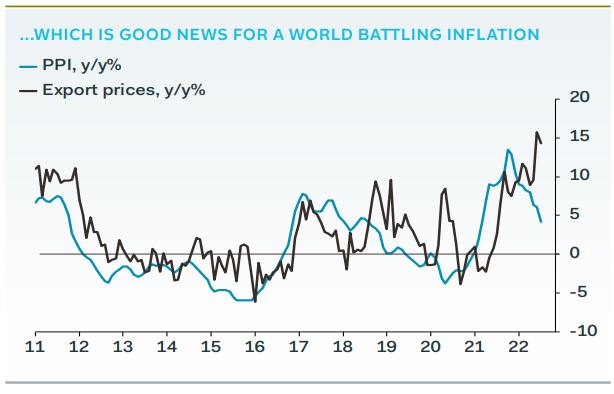

Disinflation has already turned to deflation for manufactured goods, prices of which fell 0.7% yearover-year in August, from growth of 0.9% in July, the first decline since 2020. This should pass through to domestic prices soon, though consumer goods prices were always resistant to cost-push inflation, partly because domestic demand is so weak. Global consumers, however, should feel more of a benefit, given the stronger degree of passthrough to export prices, shown in our chart above.

The authorities have, in recent months, reassured markets that the 3% inflation target is achievable for 2022. This always seemed an unnecessary statement, to us. The target has never been at risk, and even if it were, it would hardly be the most pressing economic problem facing China. Frankly, we would rather see China embrace a breach of the target because it would imply more expansionary fiscal policy, a prospect which currently seems very distant.

Instead, nearly every policy setting seems designed to limit inflation, even at the expense of slower growth.

We could say that the central bank has policy space, thanks to this lower inflation. But it would be meaningless. Monetary policy in China is powerless to support growth, because the economy is in a liquidity trap. Consequently, the main message from the inflation data is that China’s economy is still slowing, with little prospect of policy relief. But at least other economies should benefit.