I wonder when Wall Street will admit to the truth. The Chinese growth era is over and endlessly pushing out the recovery is pointless. Not until they rid themselves of their commodity long, I guess! Goldman kicks the Chinese can again when the base case now is now that not only is no recovery coming, a recession is likely as smashed domestic demand meets a global trade shock.

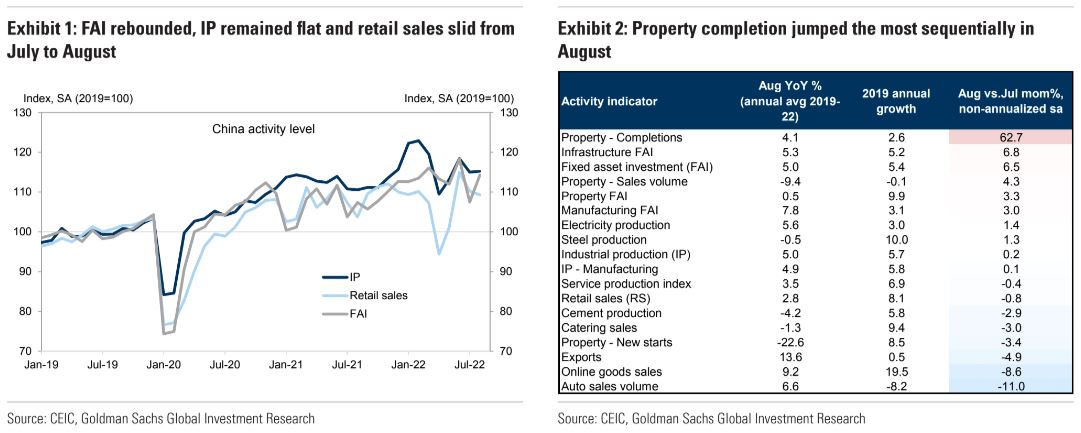

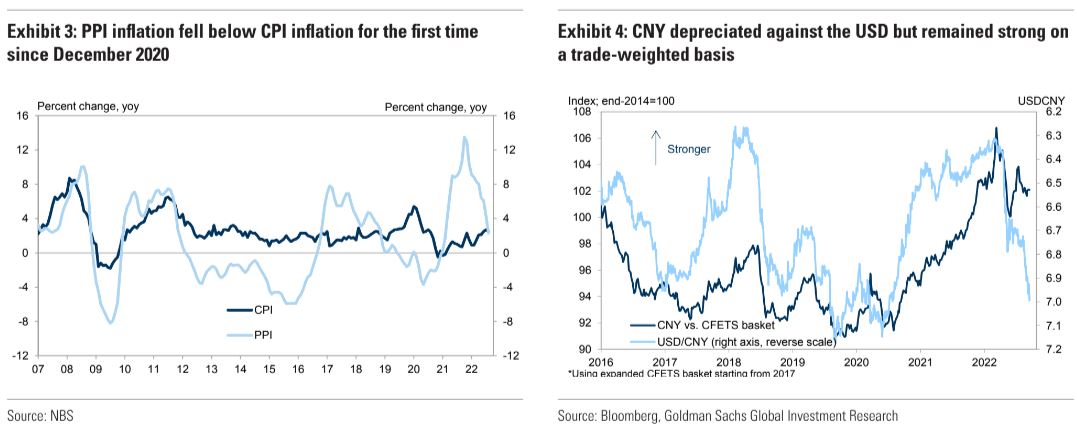

August activity surprised to the upside on low expectations. Investment rebounded from the July dip, industrial production was flat, and retail sales slid on a sequential basis. Property completions increased the most on the government’s efforts to prioritize construction and delivery of pre-sold apartments. Exports fell notably and disappointed consensus for the first time in a year.

Monthly volatility aside, the bigger picture of the Chinese economy remains the same. Rolling lockdowns continue under the zero-Covid policy. The property market recovery struggles as local lockdowns muted the impact of property easing and the breadth of government support for developers remains unclear. Infrastructure investment is still a rare bright spot in the economy. Consumer confidence is still depressed amid heightened uncertainties about the future. Taken together, our 3% GDP growth forecast for 2022 is on track.

The upcoming 20th Party Congress and potential changes to domestic policy have garnered significant market attention. In our view, policymakers’ reaction function such as “no flooding of easing measures” and the top leadership’s long-term goals such as “housing is for living in, not for speculation” are unlikely to change after the 20thParty Congress.

On the dynamic zero-Covid policy, we believe China is unlikely to begin reopening before Q2 next year on both political considerations (e.g., government reshuffling at next March’s “Two Sessions”), and medical considerations (e.g., elderly vaccination rate and the availability of cheap and effective Covid pills). In this baseline scenario, the growth acceleration expected upon reopening may not materialize until H2 2023, resulting in a delayed economic recovery.

Considering the delayed rebound from China reopening, we revise down our 2023 GDP growth forecast to 4.5% (vs. 5.3% previously). On a sequential basis for 2023, we expect a softer Q2 growth because the initial stage of reopening will likely lead to a surge in Covid cases. We nudge up H2 2023 sequential growth on consumption and service recovery after reopening, although policy accommodation may be partially withdrawn in response.