Morgan Stanley on China’s mushrooming funding gap as the housing market comes apart. I have learned over time that MS is rather bullish on China so take its suggestions with a grain of salt.

There’s no health reason for China to pivot out of zero-COVID. Its vaccination rates have basically stalled and Sinopharm doesn’t work very well anyway. There’s no particular political reason, either. Xi Jinping has hung his hat on it so Emporer or not he is still responsible.

It is the economic and fiscal costs climbing too high that is the most likely trigger. Beijing could open up and just bury the exploding death rates with its usual Ministry of Misinformation tricks.

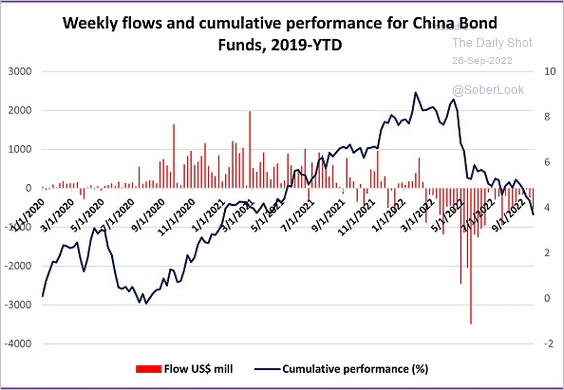

After all, funding that deficit is not getting any easier as CNY collapses:

And capital flees the bond market:

Any Spring pivot is an eternity from today and will not fix the property market anyway…

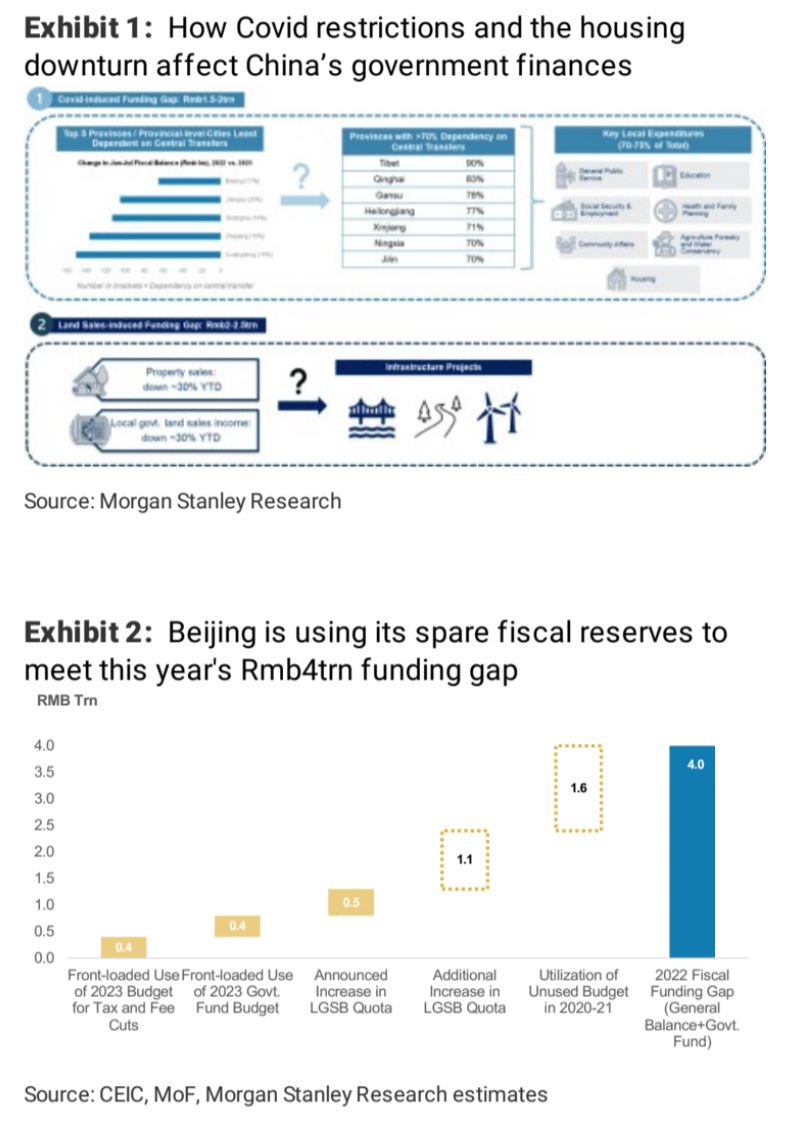

Covid restrictions and a housing downturn have added to fiscal sustainability risk by causing an estimated Rmb4trn funding gap in 2022 and using up spare fiscal reserves. To avoid a potential cut in essential social benefits in 2023, either a rise in public leverage or an exit from Covid zero to support growth is likely needed.

Why could fiscal sustainability trigger a change in China’s Covid policy? While growth is tracking at the edge of our estimated recession threshold of 2.5%Y, we think Beijing’s recent doubling down on Covid zero and slow response to the housing downturn leave investors little hope of imminent policy changes. However, our analysis suggests government finances are deteriorating quickly, which we think may prompt Beijing to exit Covid zero in 2023. The housing downturn and Covid restrictions have caused an Rmb4trn funding gap for local governments this year, we estimate, likely usingup central government’s spare fiscal reserves. If there is no change to Covid zero in 6 months, we think policymakers could face a dilemma between cutting livelihood-related social spending in inland poorer provinces (which would be a setback to policy goals of poverty reduction and common prosperity) and a rise in the government debt ratio.

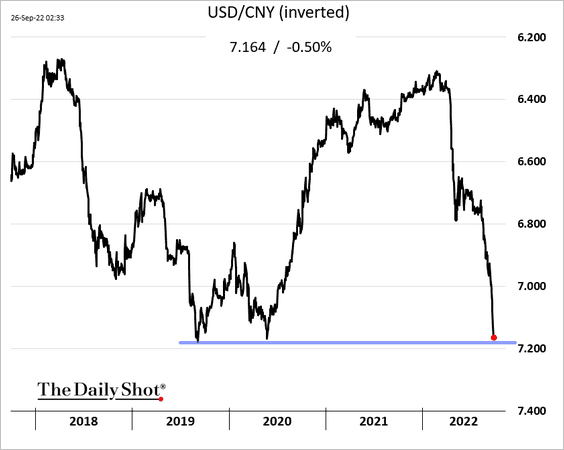

How does Beijing meet this year’s fiscal funding gap and maintain public spending? We estimate that the full-year government funding gap (the difference between the actual and budgeted deficit) could reach a record high of ~Rmb4trn this year. Within this, we estimate around Rmb1.5-2trn is due to the impact of Covid lockdowns on general government revenue, which could affect central government fiscal transfers and threaten spending on essential social benefits in poorer inland regions; the other Rmb2-2.5trn is caused by reduced land sales amid a sluggish property market,a key funding source for local government infrastructure spending.

Nonetheless, both livelihood-related public spending and infrastructure capex growth have held up well this year, as Beijing has been using its spare fiscal reserves to make up for the fiscal revenue shortfall. Over the past three months, policymakers announced the front-loading of Rmb800bn of the 2023 budget into this year and introduced Rmb500bn of additional local govt. special bond (LGSB) quota. We think the remaining Rmb2.7trn shortfall could be funded by: (1) another increase of Rmb1.1trn in LGSB quota, which is the amount available under the LGSB debt ceiling management;and (2) mobilization of the remaining Rmb1.6trn unused fiscal budget in 2020-21.

Why is the fiscal position not sustainable? The total fiscal funding gap will likely stay at ~Rmb4trn if Covid zero and the housing downturn extend into next year,and could be even larger should non-linear housing spillover risk materialize. Given that the spare fiscal reserves would already be depleted by next year, we think the reduction in fiscal revenue would inevitably translate into weaker government spending. In our view, what would concern Beijing the most would be constrained central fiscal transfers to support poorer inland provinces. This would likely affect livelihood-related public spending (such as social benefits,healthcare,and education) in these regions, countering the policy goals of poverty reduction and common prosperity while adding social stability risk. Reflecting this pressure, the general budget balances of Guangdong, Shanghai, Beijing, Jiangsu,and Zhejiang – which are the top five contributors to central government fiscal revenue – have worsened notably YTD amid Covid lockdowns. To be sure, Beijing could turn to a rise in public financing and hidden debt buildup to fund spending. But without a clear trend toward a Covid zero exit, such moves would increase doubt on China’s fiscal sustainability.

The way out – a gradual Covid exit next spring?In our view, the most effective way to revive growth and fiscal revenue would be to shift away from the Covid-zero strategy.

This would bring a turnaround in domestic private consumption (particularly services) and amplify the policy easing pass-through to the real economy. A recovery in the job market and a rise in mobility would also benefit property sales,helping stabilize local government land sales. Nonetheless, renewed lockdowns in several major cities and the recent slowdown in vaccination progress, coupled with a risk of resurgence during the winter, suggest that a swift end to Covid-zero after the Party Congress is doubtful. We will be closely watching for signposts such as faster pace of vaccination, wider adoption of domestic Covid treatments, and shifts in public opinion on the publichealth implications of Covid in the next 3-5 months. These, if they materialize, could give us higher conviction on a gradual reopening from spring 2023and a firmer economic recovery from 2Q23.