In a bear market be bearish. Chinese property is in a bear market and will keep throwing spanners into the global works:

China’s mortgage boycott may be picking up steam, even as authorities try to stem the crisis with support measures.

A highly-watched list on the GitHub open-source site titled “WeNeedHome” showed that homebuyers are boycotting 342 projects in 119 cities, up from about 320 in 100 cities in early August. There are a high number of boycotts in the central Henan and Hunan provinces.

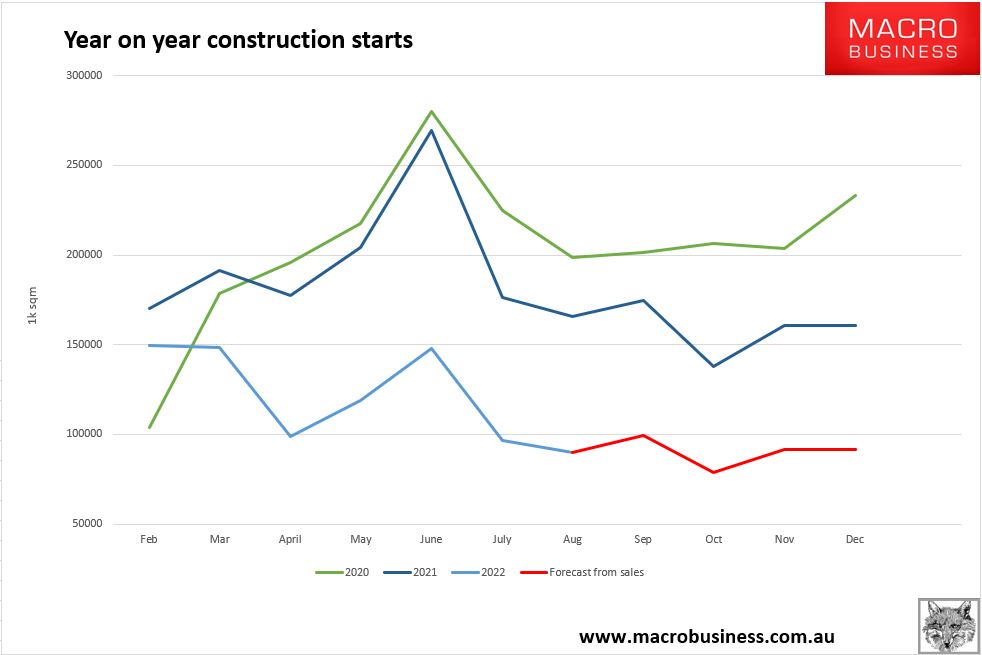

The latest sales numbers are -43% for new home floor space. This is significant because we are already into annual base effects that should be making year-on-year comparisons easier not harder given that 2021 numbers were far down from 2020. Instead, it is getting worse:

Advertisement

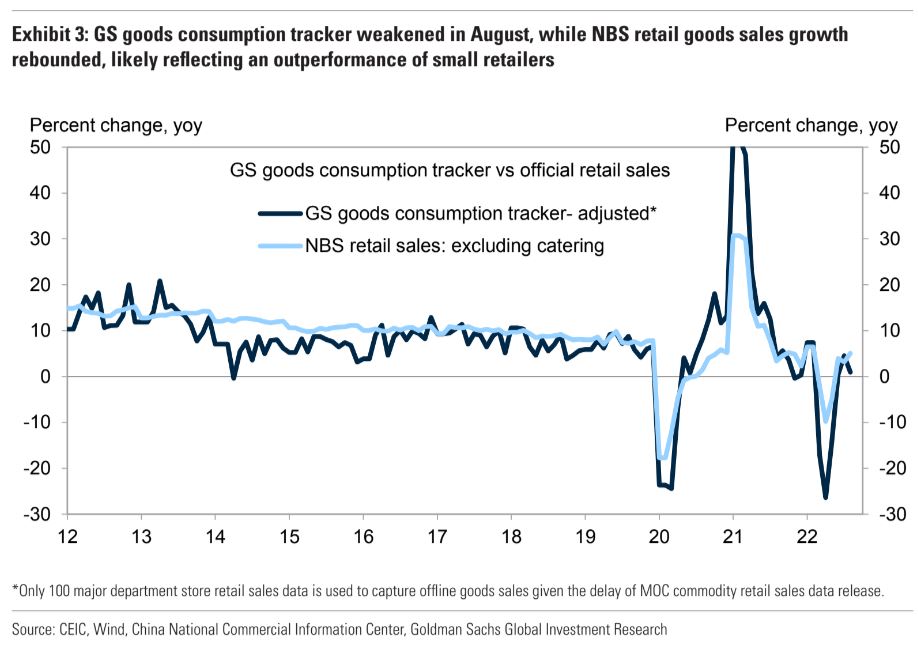

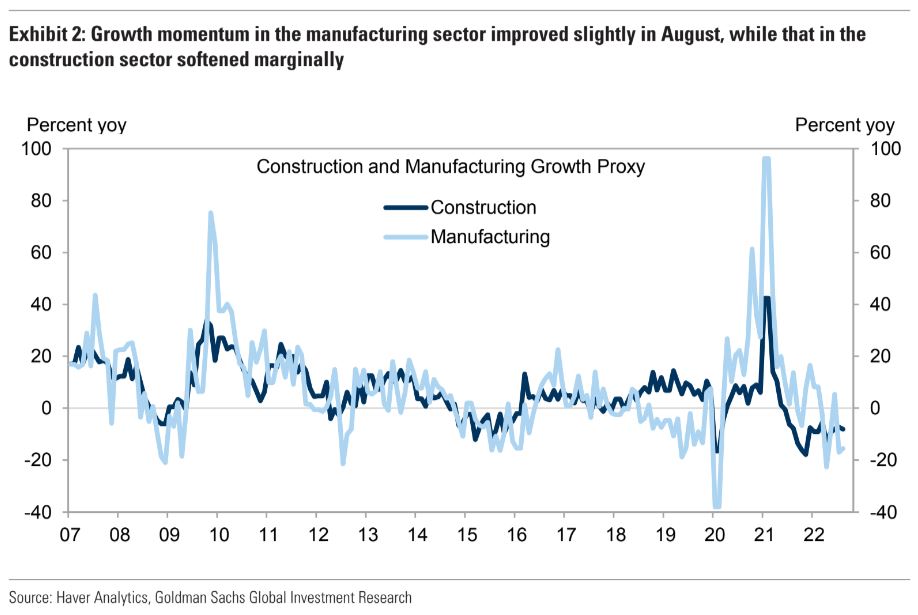

Goldman’s nowcasting indexes have retail, construction, and industry all struggling mightily:

And help is not coming. Pantheon:

Advertisement

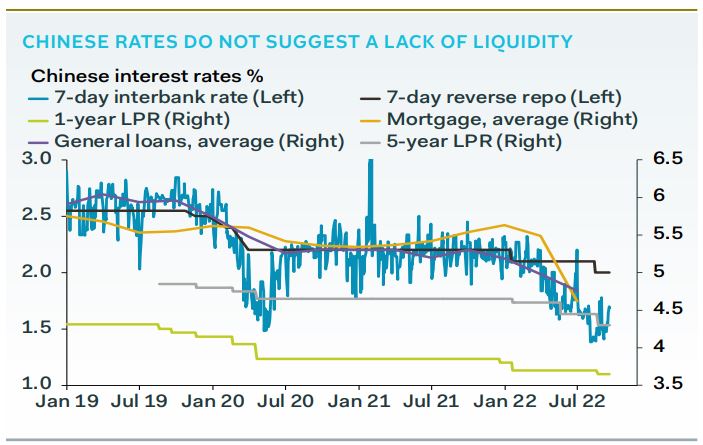

Monetary policy also looks fairly stable in China, for the time being. The 1- and 5-year loan prime rates were left unchanged on Tuesday, in line with expectations, after the MLF policy rate was left on hold earlier this month. The PBoC has cut the 14-day repo rate by 10bp, to 2.15%, but this is both a very small cut, and applies to a tool used only rarely; 14- day liquidity was last provided in February.

The September injection of 14-day liquidity is a drop in the ocean compared to the RMB 200B withdrawn through MLF operations, so we still see the PBoC as tightening policy, at the margin. As we have argued before, China is in a liquidity trap at the moment. Loan growth is struggling despite liquidity injections and rate cuts, and market rates are either below policy rates, or falling much more rapidly than the small cuts implemented by the PBoC, as shown in our chart below.

We stll think, however, that we will see one last easing push by the PBoC before the year is out, even though it will not amount to much. Pressure on the central bank to support the economy is likely to build, and with local governments under pressure to utilise bond quotas fully by October, demand for liquidity should rise, temporarily. We think an RRR cut is still in the offing, as a result. But note that it requires fiscal spending to make monetary policy useful again.

Much MOAR easing will be needed but it can’t be delivered until the Fed is done lest Chinese authorities trigger a currency and financial crisis.

Even then, as monetary pressures ease, a trade shock will land as the Fed only stops when the US economy does.

China is ground zero in the coming global recession.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.