Goldman has an update on the rapidly deteriorating Chinese fiscal circumstances. Note especially the harm being done to revenue from the property bust. This is the problem with the pro-cyclical economic system that develops over the lifetime of a major bubble. When it ends, it is as hard to keep aloft as it was easy to keep it going in the salad days.

Note as well that Goldman is hinting at the possibility of a Chinese financial crisis as its impossible trinity unwinds. It’s not my base case but it is still an uncomfortably real tail risk.

Property bust > deeper deficits > cash rate cuts > falling CNY > market rate hikes > property bust > rise and repeat…

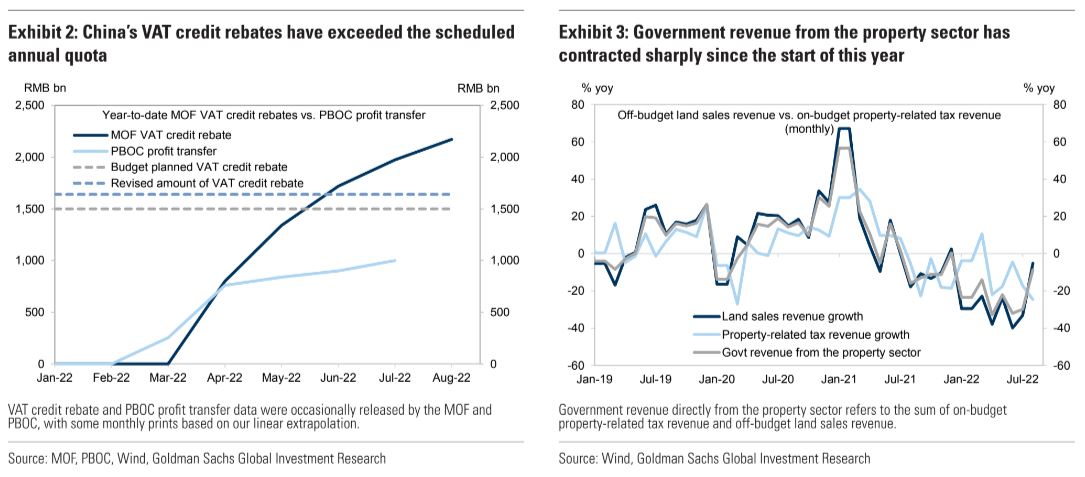

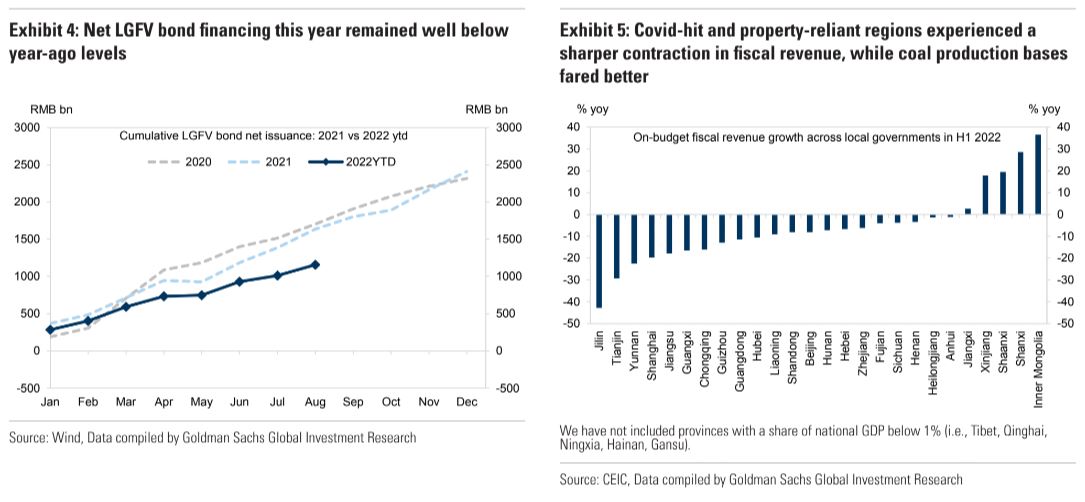

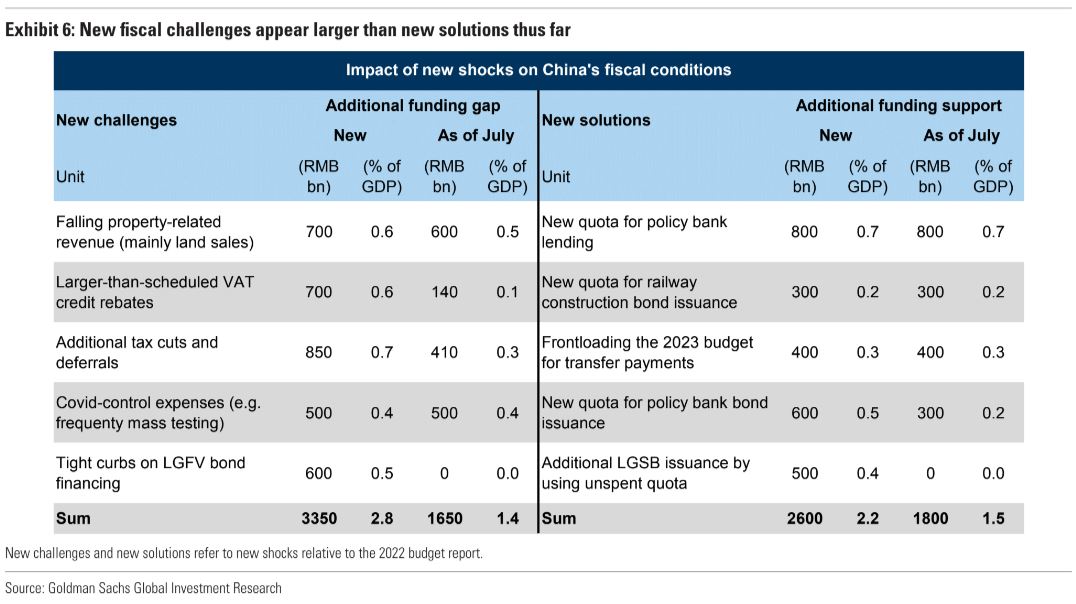

Since we published our H2 fiscal outlook in early July, there have been some new developments on China’s fiscal challenges: 1) larger-than-scheduled tax rebates and deferrals; 2) sharper-than-expected contraction in property-related government revenue, and 3) persistent weakness in LGFV financing. We also see fiscal stress unevenly distributed across regions, with Covid-hit and property-reliant local governments bearing the brunt.

As a response, the government has rolled out incremental stimulus measures to fill the funding gap, including an RMB500bn quota for additional LGSB issuance and another RMB300bn quota for policy bank credit support. However, we estimate new policy solutions appear insufficient to fill in the government funding gap caused by new fiscal challenges relative to the 2022 budget.

Although we expect incremental fiscal easing to maintain the strength in government spending, a massive stimulus package after the 20thParty Congress appears unlikely, as policymakers clearly understand their policy constraints at present, the current focus of top policymakers appears to be on stemming further downside risks, and the efficiency of fiscal stimulus could be a concern.

Given the significant government funding gap this year, China has consumed some one-off policy buffers accumulated from previous years, borrowed some policy space from the future and leveraged more off-budget channels. The unique pattern of fiscal policy this year has strong implications for policymaking next year, and could significantly affect the funding conditions for the government and corporate sectors in 2023.

We maintain our forecast for China’s augmented fiscal deficit (AFD) to widen by 3pp of GDP this year, but to narrow by 2pp in 2023, which implies a more gradual pace of fiscal policy normalization ahead than in 2021. Moreover, we expect fiscal policy to be frontloaded again in 2023, similar to 2020 and 2022.