From the excellent Gareth Aird at CBA today.

Overview

The Australian economy performed very well over the first half of 2022 as evidenced by the Q2 22 national accounts.GDP grew by a strong 1.6%overthe March and June quarters combined, largely powered by the consumer. Over the same period employment rose by ~300kand the unemployment rate dropped by 0.7ppts to 3.5%. These were incredibly strong outcomes and signalled that the Australian economy had strong momentum when the RBA commenced its tightening cycle in May 2022.

But hot economic expansions cannot run indefinitely. The challenge for policymakers is to avoid turning a boom that has been accompanied by swiftly rising inflation into a bust.

The RBA Board is committed to returning inflation to target over time. And as Governor Lowe has stated on more than one occasion it is seeking to do this in a way that, “that keeps the economy on an even keel”.

The Governor acknowledged the significant challenge the RBA faces in achieving these outcomes when he stated, “it is possible to achieve this, but the path here is a narrow one and it is clouded in uncertainty.” We very much agree.

The RBA has put through an incredible amount of tightening in a very short amount of time. It has caught the vast majority of households and businesses off guard as they were under the impression rates were likely to be on hold until ‘2024 at the earliest’. In contrast CBA called a 2022 RBA rate hike in June 2021.

We were not surprised the RBA commenced their tightening cycle in Q2 22 (in February this year we pencilled in June for the first rate). But the rapid pace and size of rate rises has surprised us. We have made revisions to our RBA forecast profile on a couple of occasions since the RBA commenced their tightening cycle. Of course we have not been alone and the entire forecasting community at various stages over the tightening cycle have amended their RBA call.

The job of a macro-economist though is not just to have a call on the central bank. We must also have a view on the real economy and in our case also the Australian housing market. The challenge has been to call both the Australian economy, housing market and RBA simultaneously when there is an inherent circularity in outcomes.

The incoming economic data and the outlook for the economy dictates what the RBA does. But the RBA’s decisions influence economic outcomes. We can therefore find ourselves at loggerheads with the central bank if we think the economy, and in particular households, will respond differently to a particular amount of policy tightening.

The RBA has focussed a lot on the resilience in consumer spending. But official data on spending to date has barely captured the impact of rate hikes given the lags between changes in the RBA cash rate and when a home borrower cash flow is impacted.

Our updated forecasts for GDP and in particular consumer spending differ to the RBA’s forecasts. We expect the economy to slow more significantly than the RBA.

Updated GDP profile

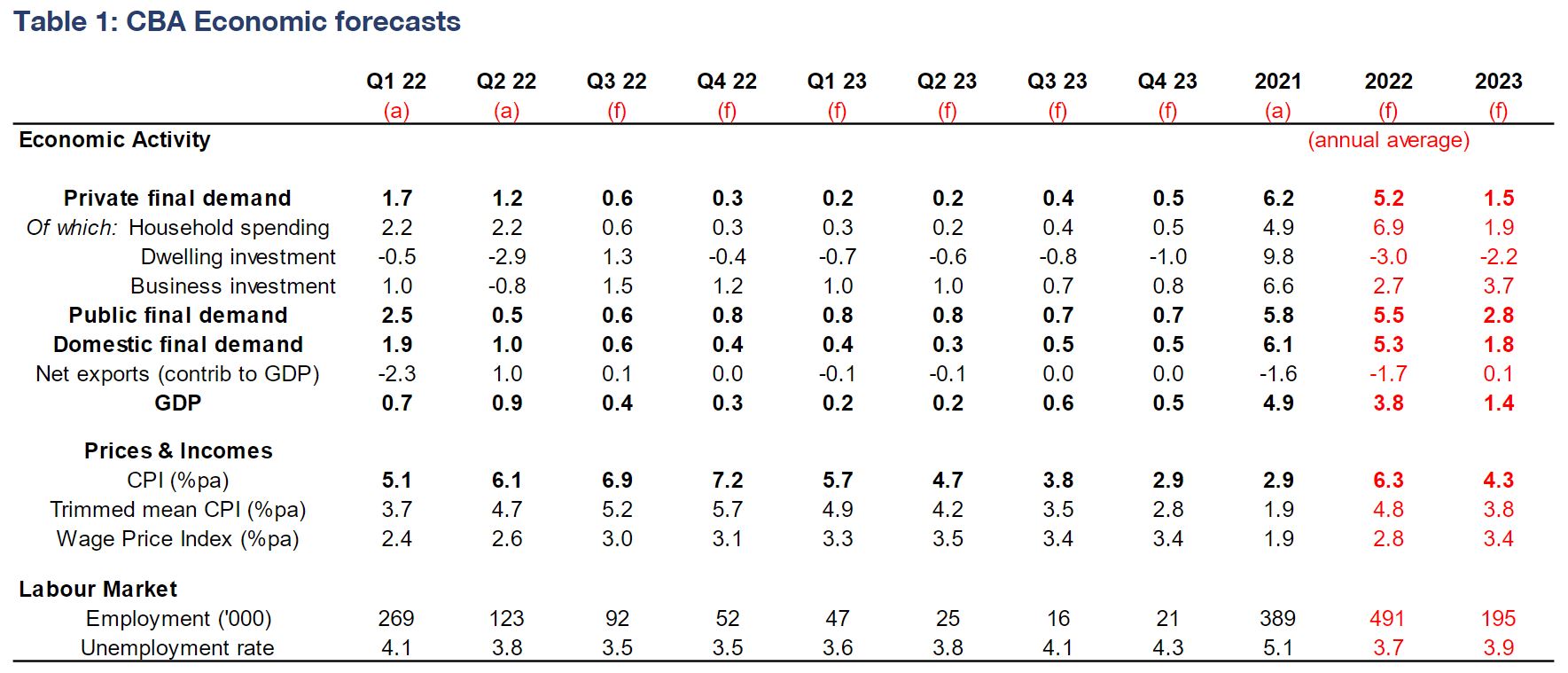

We have made some amendments to our GDP profile. The most significant is our expectation for considerably slower growth in 2023.

We forecast GDP growth to moderate over H2 22 and for growth to be 2.3%/yr at Q422 (3.8% annual average in 2022). GDP is expected to further slow in 2023 to be 1.5%/yr in Q4 22 (1.4% annual average in 2023).

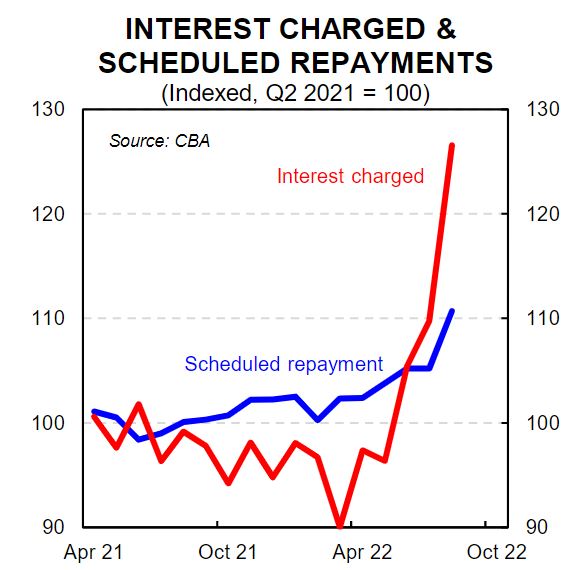

At the heart of our forecast for materially below-trend growth is a significant slowdown in household consumption. The compounding forces of negative real wages growth, considerably higher standard variable mortgage rates, the fixed rate home loan expiry schedule, falling home prices (and by extension a negative wealth effect), lower turnover in the housing market and bracket creep will all weigh on spending. For context we estimate that the interest paid on housing debt is likely to swell by ~$A40bn in 2023 (from 2.0% of GDP in 2021/22 to ~3.5% of GDPin 2023).

There will be a partial offset by an anticipated fall in the savings rate(the savings rate will decline to 6.0%by end-2023on our forecast profile). And by H2 23 we believe real wages growth will turn positive. In addition we expect the RBA to ease policy in H2 23as inflation comes down and the focus shifts towards monetary policy providing support to stop the unemployment rate from rising above 4.5%. Notwithstanding over the next year the headwinds on the consumer will significantly outweigh the tailwinds. As such, we expect very modest growth in consumer spending.

On our estimates household consumption growth will slow to 5.3%/yr in Q422 (growth of 0.9% over H2 22 is anticipated). We forecast consumer spending to be 1.4%/yr in Q4 23. Our forecast profile sees the volume of household consumption per capita fall over Q4 22 and H1 22. Strong population growth should mean the overall level of spending does not contract. It is, however, a distinct possibility, particularly if the RBA takes the cash rate north of 3.0%.

Inflation and wages

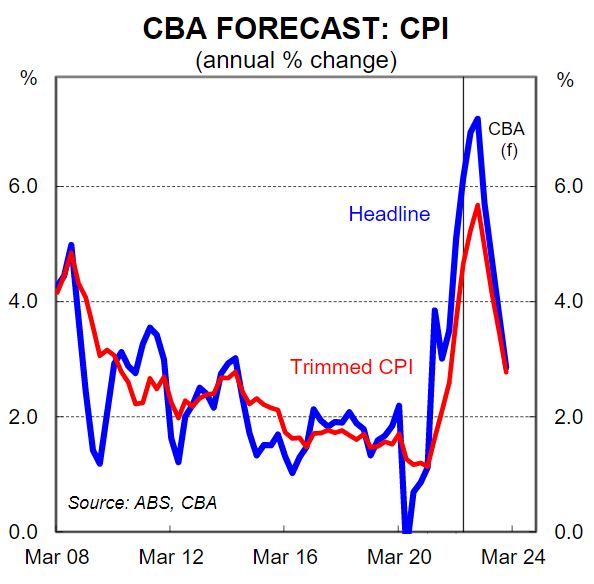

We expect the headline rate of inflation to peak at ~7¼%/yr in Q4 22(not too dissimilar to the RBA’s forecast for a peak in inflation of 7¾%/yr).But our key point of differentiation with the RBA’s inflation outlook lies in ourprofile for 2023. More specifically we expectboth headline and underlying inflation to sit at the top of the RBA’s 2-3% target by late-2023 (2.9%/yr headline and2.8%/yr underlying at Q4 23). In contrast the RBA expects headline inflation to be 4.3%/yr in Q4 23 and underlying inflation to be 3.8%/yr.

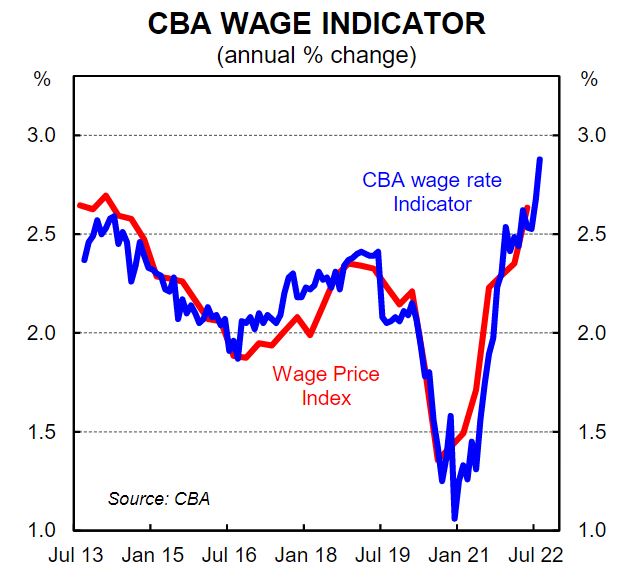

Our internal data on wages paid into CBA bank accounts indicates that wages growth was running at 2.9%/yr in August 2022 (note that our data measures actual dollars paid into a matched sample of ~275k CBA bank accounts–see facing chart). Australia is not in a wage-price spiral like is being observed in some other jurisdictions.By extension the RBA does not need to run as hard as other central banks against inflation and wages. Indeed the RBA wants wages growth to continue to rise!

We expect wages growth, as measured by the wage price index (WPI) to accelerate to 3.5%/yr by mid-2023, which is very similar to the RBA’s forecast. This is an outcome that is desired.

Fiscal policy

Fiscal policy remains a key unknown and therefore source of risk. But the most recent comments from Treasurer Jim Chalmers indicate the 25 OctoberBudgetis unlikely to contain any meaningful stimulatory policies. On 7 September the Treasurer stated, “the task in providing responsible cost-of-living support is to make sure that you can do it in a way that doesn’t put extra pressure on the Reserve Bank and risk being counter-productive”.

The Government is clearly cognisant of the relationship between demand and inflation. And it looks like the Government does not want to do anything that would cause interest rates to rise by more than would otherwise be the case.