DXY was firm Friday night. It looks like it’s gathering for another spring to me:

The all-important CNY held on with the support of better than expected, though very poor, data:

Advertisement

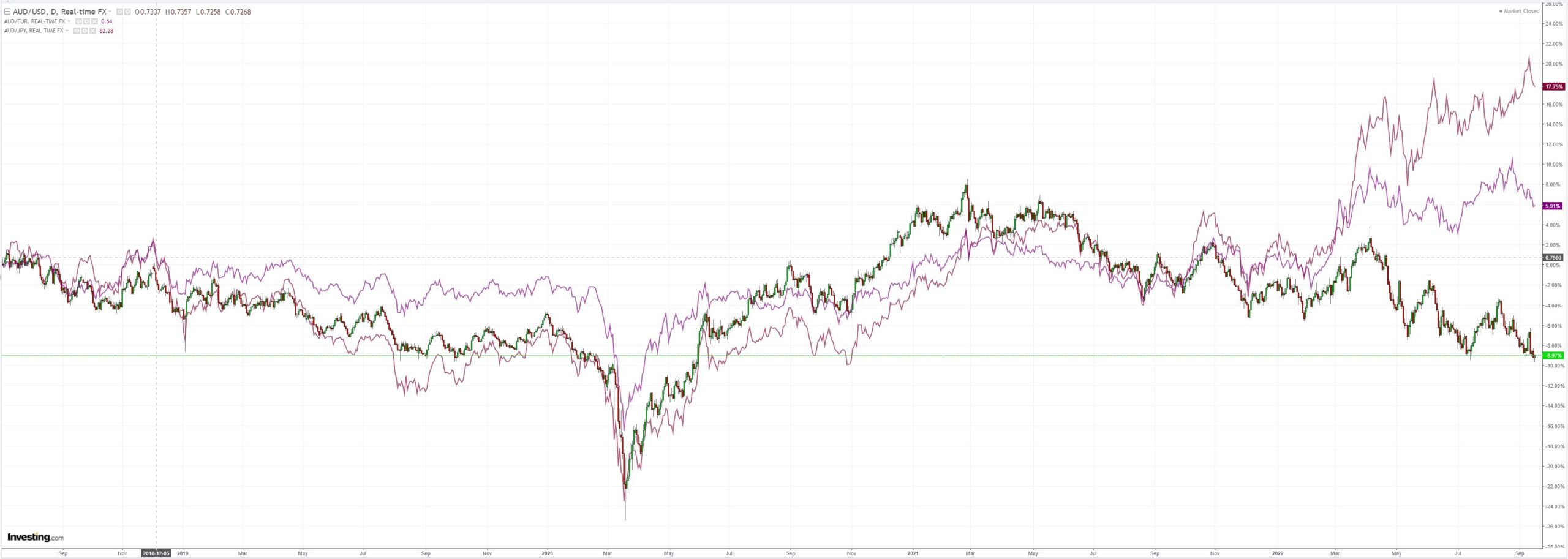

AUD held on hopelessly:

Oil and gold are not well:

Buy base metals if you are an idiot:

Advertisement

Miners leaking away:

EM stocks broke:

US junk is at the cliff:

Advertisement

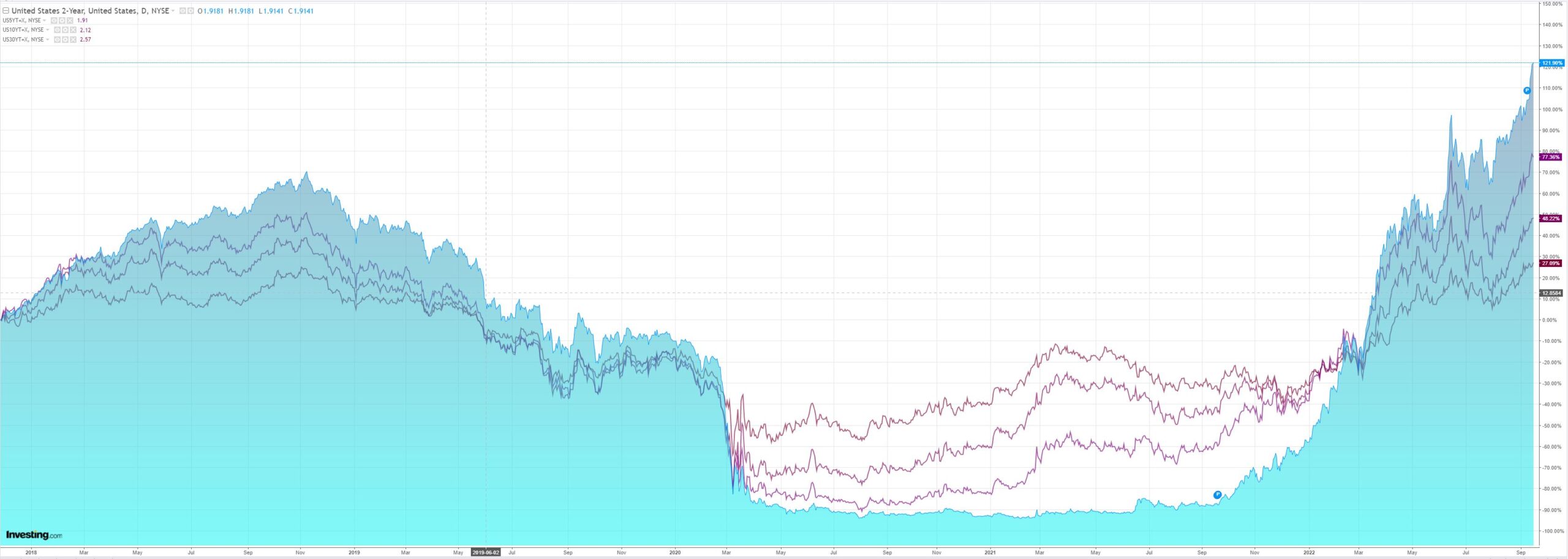

Thr curve is a red mess:

DM stocks broke:

It’s Fed week. 75bps? 100bps? Who cares. It’s not done.

Advertisement

Therefore, neither are the falls for AUD. Citi:

We are bearish AUDUSD in the near-term, but expect a gradual recovery in the medium-termfor the pair. AUDUSD will remain heavily driven by deteriorating external drivers in the short-term. Further downside to risk-assets (we think equity markets have yet to price in a recessionfrom an earnings perspective, and risk sentiment is key for AUD performance. AUD exhibits the second highest average historical beta to MXWO in G10), a Fed that will keep aggressively tightening, and pessimism around Chinese economy with further lockdowns and still lacklustrepolicy support for credit/ property markets, should see further AUD weakness. China feeds into AUD dynamics also through AUDUSD’s tight correlation with broader EM Asia FX, which our EM Strategists forecast to continue to weaken from challenges to growth, manufacturing and export performance.

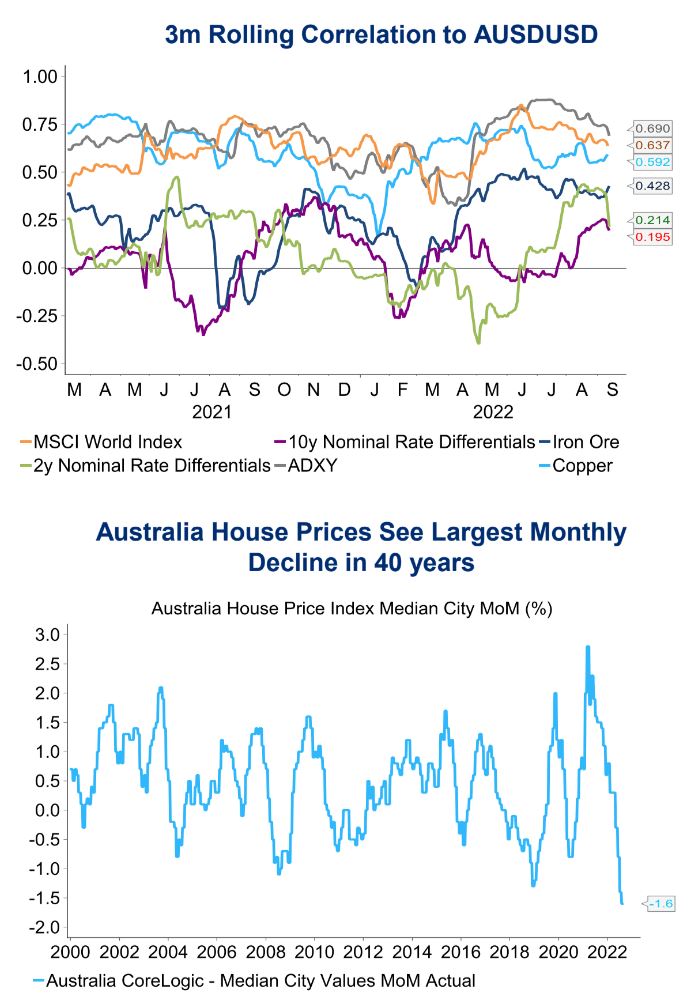

The RBA has also leaned dovish, and Citi Economics expect them to slow the hiking pace to3x 25bps hikes this year, to 3.1% terminal rate throughout 2023. This compares to peak OISpricing at around 3.5%, so Citi are still below the market even with a large negative repricing since Lowe’s dovish speech at the Anika Foundation. Against a backdrop of the largestMoM%drop in house prices in 40 years and an 80% floating rate mortgage market, we certainly sympathise with the view that market policy rate pricing is too rich. As a caveat, we note that correlations to rate differentials have not been moving AUDUSD since the start of the year, but these correlations have started to creep up.

Interesting that stocks have had the highest correlation with AUD in COVID-era. I guess we take that as a signal that both are unduly influenced by the same American money printing.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.