Australia and New Zealand face world-leading housing crashes

Goldman Sachs has released research tipping large house price declines across Australia and New Zealand. Goldman also believes these housing downturns pose major risks to their respective economies.

_________________________________________________________________________________________________

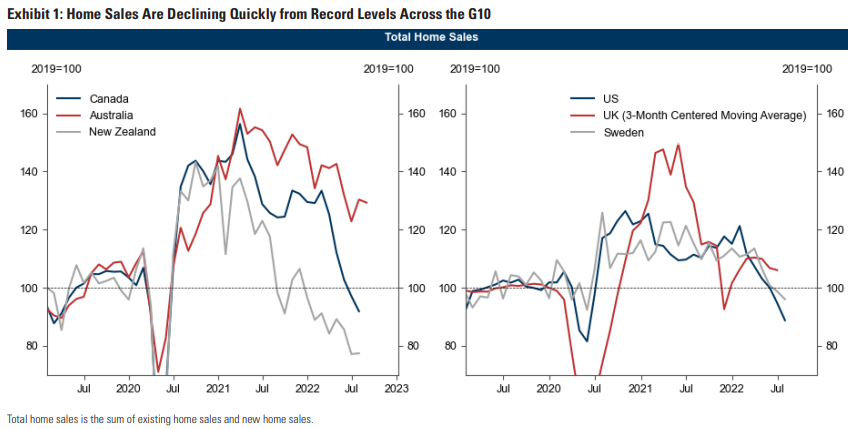

Following the rapid deterioration in affordability, home sales are falling quickly from record levels across the G10. Home sales are now below the pandemic peak by around 45% in New Zealand, 40% in Canada and the UK, 30% in the US, and 25% in Australia and Sweden (Exhibit 1).

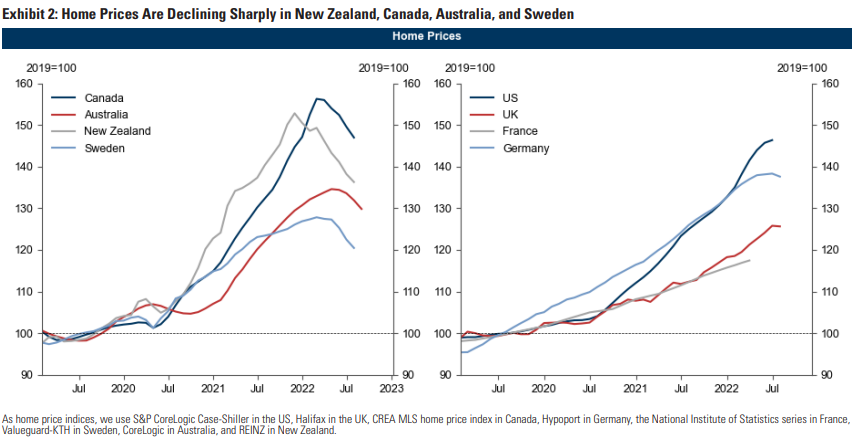

Home price growth is slowing too, with outright price declines in places that saw the bigger increases during the pandemic. Home prices are now 11% below the peak in New Zealand, 6% in Canada and Sweden, and 4% in Australia…

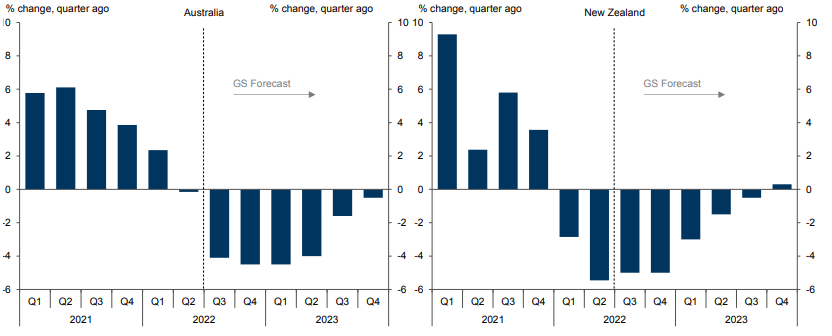

Our models imply sizable home price declines from the peak through end-2023 of 21% in New Zealand, 18% in Australia, 13% in Canada, and 6% in France. Our models also suggest that nominal home prices will stagnate in the US and the UK. Beyond the formal models, we view the risks to these forecasts as tilted to the downside because our descriptive home price outlook scores have weakened sharply and because of evidence of strong mean reversion in regional data.

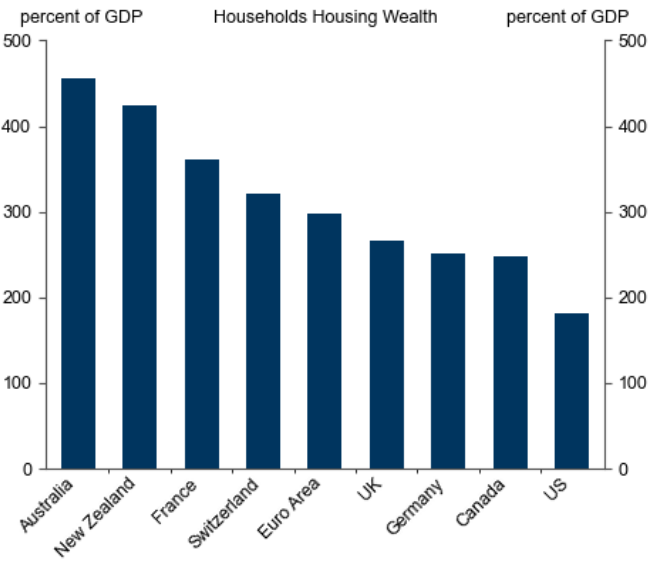

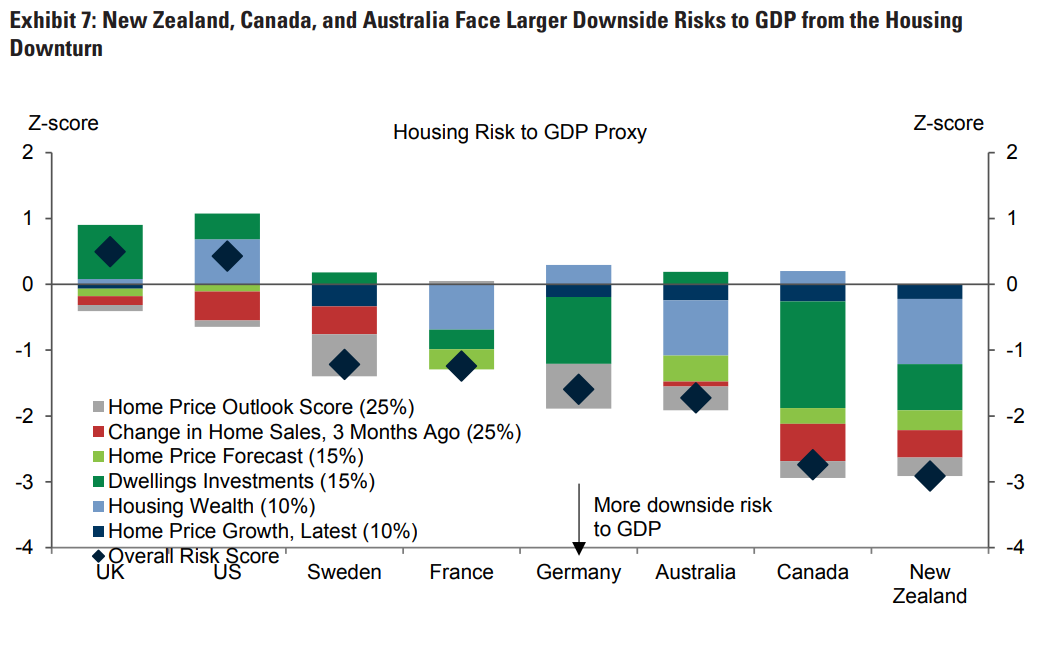

Households housing wealth is especially large in Australia and New Zealand where it exceeds 400% of GDP…

Based on this negative outlook for home prices, and the importance of residential investment and housing wealth, we find that the housing downturn poses larger downside risks to GDP in New Zealand, Australia, and Canada…

Overall, the housing sector is likely to play a larger role during this hiking cycle in New Zealand, Canada, and Australia than in the US and Europe, both through growth and inflation. However, even in New Zealand, Canada, and Australia, central banks are unlikely to blink because of a weaker housing market anytime soon, given their strong desire for both housing and inflation to cool significantly.