Aussie bank bubble bursting slowly, then all at once….

The usual Aussie bank groveling articles are appearing as we approach full-year results. These articles focus on the juicy dividends without making reference to the business cycle. A bad idea.

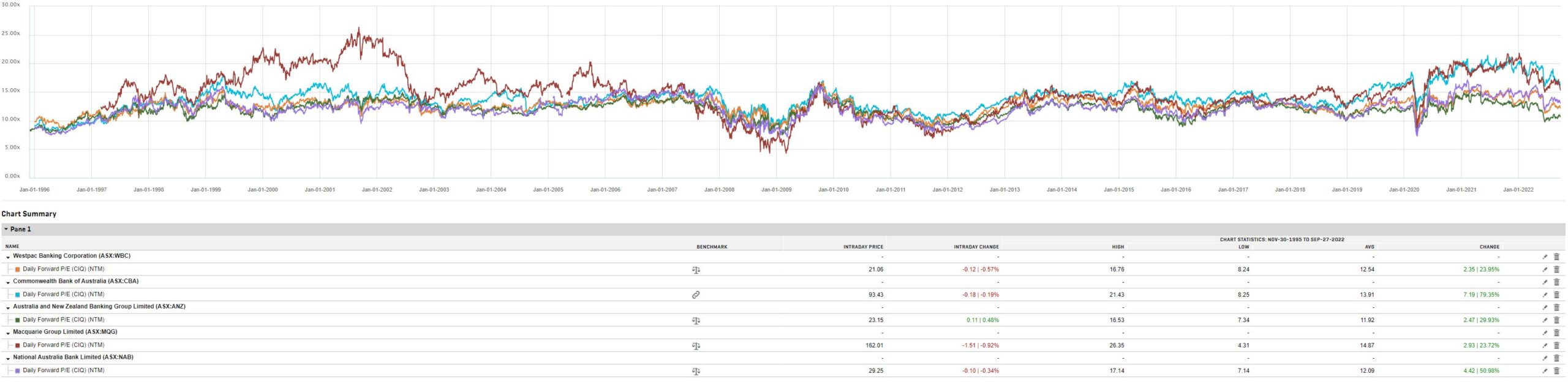

Bank’s forward earnings multiples have been falling much of this year. Some of this is the lifting margins emanating from rising interest rates. Some of it, and more importantly for this post, is falling capital values:

For me, it is pretty obvious that the business cycle is deteriorating quickly and earnings tailwinds are going to turn into headwinds in short order as the RBA overcooks the tightening. Australia is lagging behind the global cycle owing to its later exit from COVID, but that is not going to matter as the proverbial poo hits the fan worldwide when central banks crash the cycle to bash inflation back into shape.

It will arrive in Australia as an external shock, more than an endogenous tightening of monetary policy which, if the RBA has any brains left, will lag what is happening elsewhere. In fact, it already is, as wholesale bank funding costs are rising steadily, soon to be alarmingly:

As you can see from the above NTM valuation, banks are still quite expensive relative to past cyclical bottoms which tend to be below 10x.

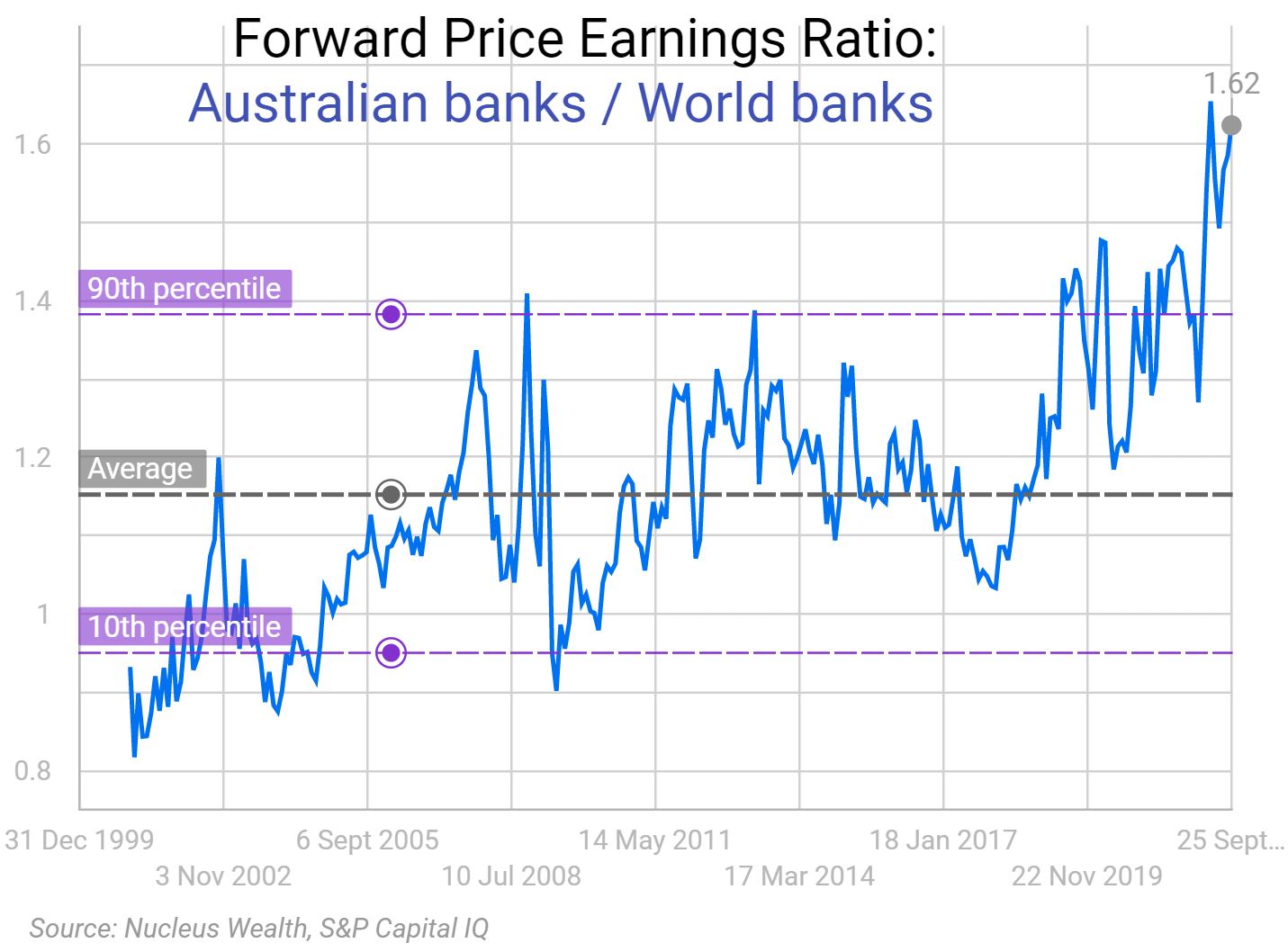

Moreover, in global context, Aussie banks are crazily expensive:

Do either of these measures make sense in terms of Australia’s exceptionally higher sensitivity to interest rate rises, I ask you?

In fact, the great Aussie bank bubble that has reigned supreme since 2017 looks rather like the vestige of a past era of lowflation in which big divvies bid banks like they were bonds.

I am not yet of the view that the future is structurally more inflationary. Perhaps it is, perhaps not. But we can certainly say that the Aussie cash rate is already overshooting given the rapidly deteriorating global economy.

At some point when the shock lands proper, Aussie banks will have to make provisions, plus earnings and divvie cuts. This may not be calamitous but it doesn’t need to be for a cyclical equity derating.

It looks rather like the old adage of first they went broke slowly and then all at once: