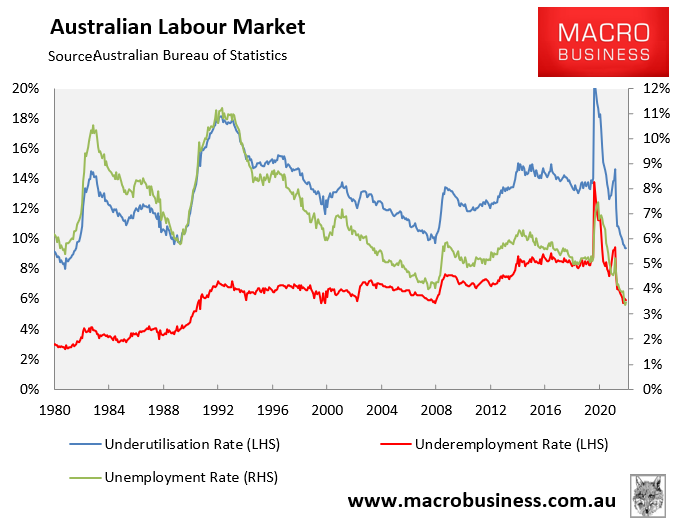

Yesterday, the Australian Bureau of Statistics (ABS) released its labour market survey for August, which revealed that Australia’s unemployment rate rose 0.1% to 3.5% (still close to its lowest level since August 1974), whereas the underemployment rate (5.9%) fell 0.1%. Labour underutilisation (i.e. unemployment and underemployment combined), remained flat at 9.4% – the lowest level since 1982:

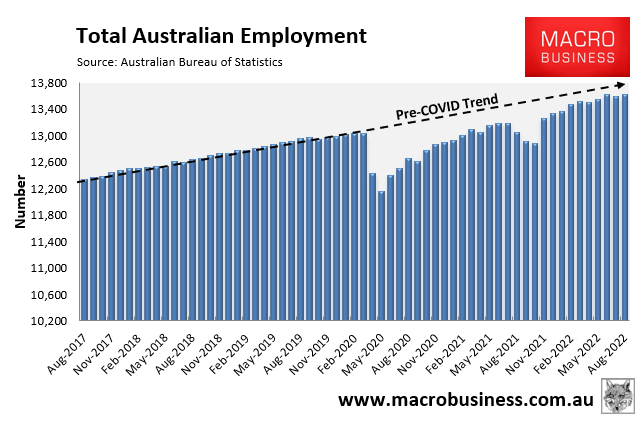

Even though total employment rose another 33,500 in August, jobs growth remained below the pre-COVID trend:

Advertisement

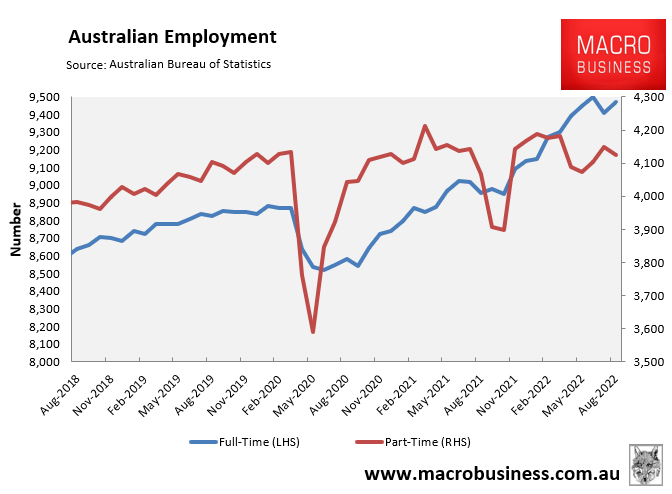

However, full-time jobs are booming, up 6.7% over the pandemic versus a 0.1% fall in part-time jobs:

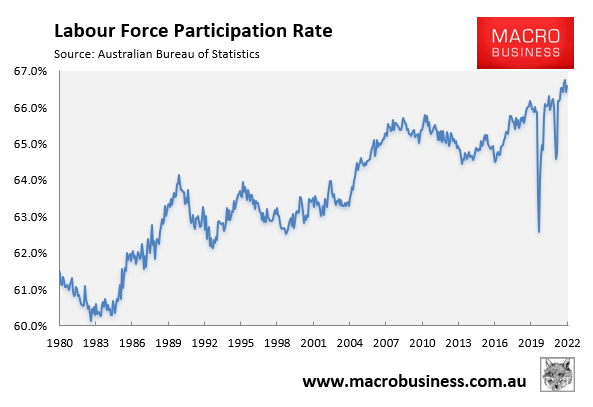

The Labour force participation rate has also climbed to 66.6% – a whisker below the record high 66.8% recorded in June 2022:

Advertisement

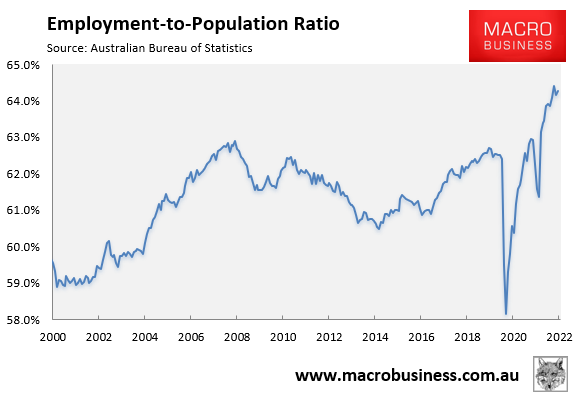

The employment-to-population ratio has also soared to 64.3% as the denominator (population) has stagnated:

Advertisement

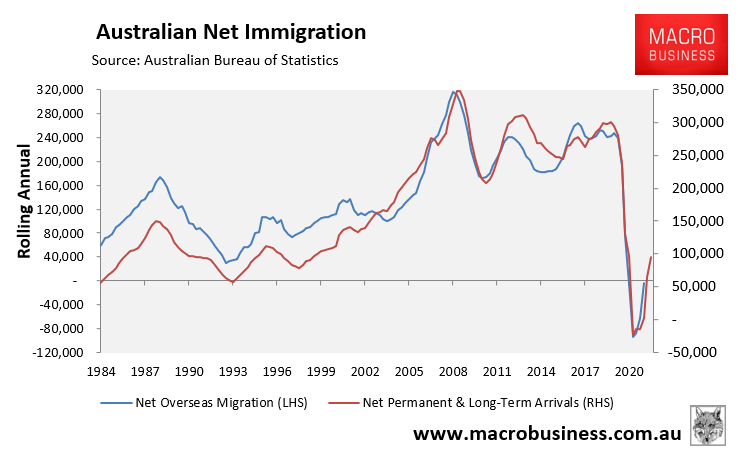

Given Australia’s jobs growth has lagged the pre-COVID trend, while labour force participation has increased, the main explanation for Australia’s near 48-year low unemployment is because labour supply has grown much more slowly, thanks to negative immigration over the pandemic:

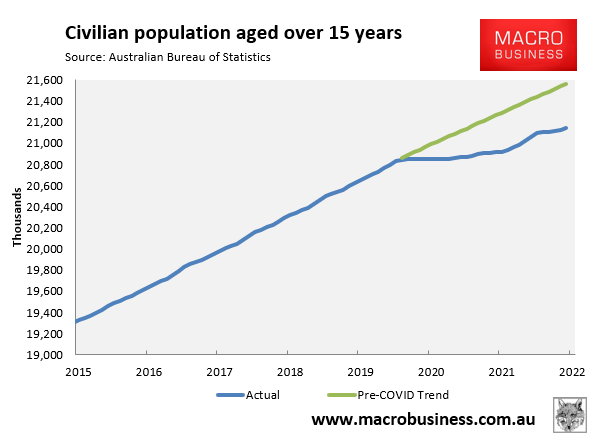

As shown in the next chart, Australia’s civilian population aged over 16 has gone from growing strongly (circa 25,000 people a month pre-pandemic) to growing only slowly:

Advertisement

Therefore, the newly created jobs have gone to unemployed Australians rather than migrants.

Had immigration continued at its pre-COVID level, Australia’s civilian population aged over 16 would be roughly 420,000 larger than it is currently. In turn, both unemployment and underemployment would be significantly higher and the employment to population ratio would be much lower (due to an increase in the denominator).

Advertisement

If you don’t believe my analysis go read Professor Bill Mitchell’s take, who is the Chair in Economics and Director of the Centre of Full Employment and Equity (CofFEE), an official research centre at the University of Newcastle. He estimates that Australia’s unemployment rate would have been 6% in August had immigration continued at its pre-pandemic level:

The following graph shows the evolution of the actual unemployment rate since January 1980 to August 2022 and the dotted line is the ‘What-if’ rate, which is calculated by assuming the most recent peak participation rate (recorded at August 2022 = 66.8 per cent), the extrapolated working age population (based on growth rate between 2015 and April 2020) and the actual employment since April 2020.

It shows what the unemployment rate would have been given the actual employment growth had the working age population trajectory followed the past trends…

So instead of an unemployment rate of 3.5 per cent, the rate would have been 6 per cent in August 2022, given the employment performance since the pandemic…

Earlier this week, both SEEK and the National Skills Commission released data suggesting that job ads have peaked.

Advertisement

This is problematic because the Albanese Government has committed to the largest temporary and permanent migration program in this nation’s history, which will necessarily ramp-up labour supply and increase unemployment (other things equal) next year and beyond.

When combined with the RBA’s aggressive rate hikes, which will slow the economy, expect to see the Australia’s unemployment rate rise back up to pre-COVID levels or above over the Albanese Government’s term.

Albo’s ‘Big Australia’ mass immigration policy will kill the jobs boom for ordinary Australians, while also leaving them desperately short of rental accommodation.

Advertisement

With friends like the ‘Labor’ Party, Australian workers sure don’t need enemies.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.