Sometimes when you take a break things can improve. Other times, they get worse.

The last week falls decisively into the latter category.

In his speech last week, Captain Phil Lowe of the RBA spent all his time explaining how it was that it missed the historic inflation surge this year:

One starting point for understanding the unexpected surge in inflation is the big lift in energy prices stemming from Russia’s invasion of Ukraine and various problems in the production of energy around the world. Analysis by the European Central Bank suggests that around three-quarters of the surprise in inflation in the euro area reflects unexpected developments in the markets for oil, gas and electricity. In the United Kingdom, the Bank of England estimates that higher energy prices will directly boost CPI inflation by 6½ percentage points this year. And in Australia, the price of petrol at the bowser increased by 32 per cent over the past year (Graph 4). The direct effect of this alone has been to add 1.2 percentage points to Australia’s CPI inflation, and on top of this there are second-round effects of higher fuel prices.

This is fair enough. It was the same war-related energy surges that caught MB by surprise.

What is not fair, is that Dr Lowe is making exactly the same mistake today, even as explains how he made it last time. Refusing to look forward.

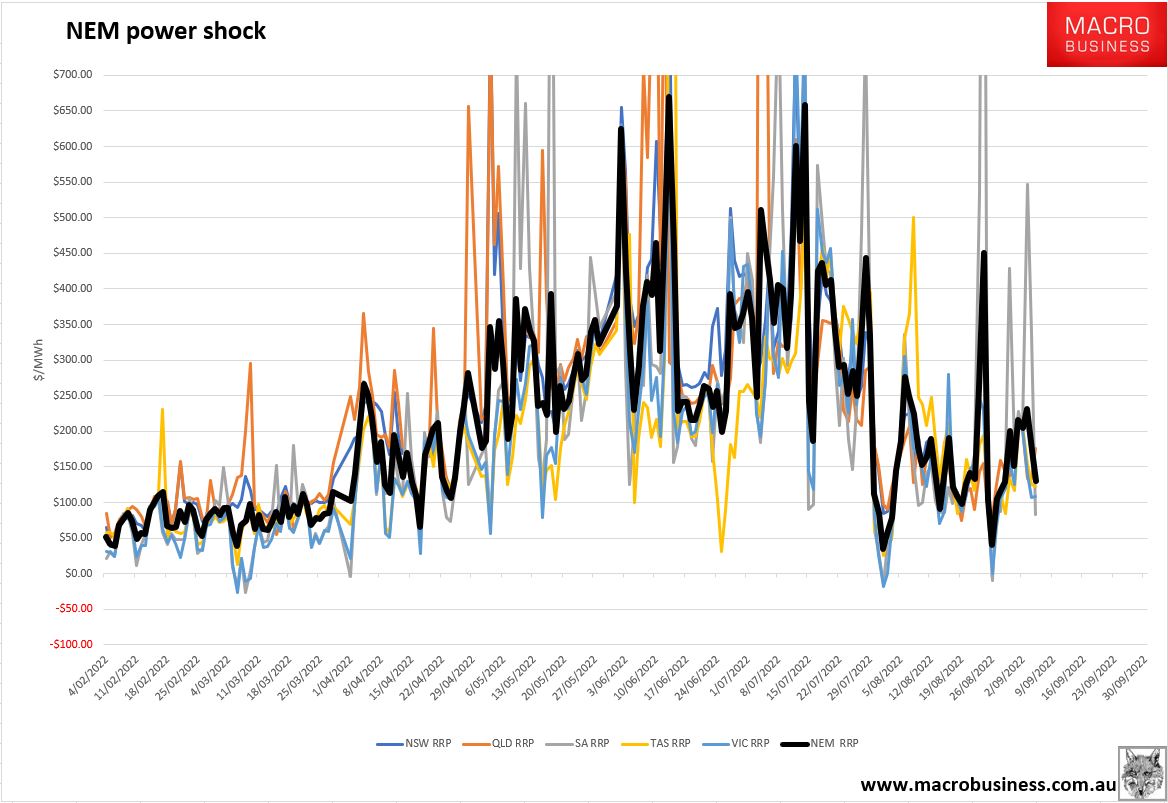

Energy prices have not come down. Indeed, they have kept going up. The east coast gas price has broken out of its $15-20Gj range of August as the shuttered sixth LNG export train on Curtis Island has reopened. Last week, prices averaged $21Gj and got as high as $25Gj over the weekend. The odds favour these prices continuing to rise because international prices are still insane at $90Gj and the evil gas cartel that is so central to setting electricity prices will naturally be pushing every available molecules offshore.

Electricity prices have duly rebounded to $150-200MW/h range. As things stand, gas and power prices will add 3.5% to the CPI over the coming year. It will be more with predictable spillovers. This destroys the RBA’s inflation outlook all by itself:

Making matters worse for Dr Lowe, his learnings from confessed failures this year indicate he should be onto the energy realty:

One lesson here is that what is happening at the sectoral level is important in influencing the overall inflation dynamics in our economy – it’s not just the aggregates that matter. Resources don’t move freely between sectors, which means that the composition of demand and supply is important, not just the overall level of demand.

In short, the head of the RBA last week utterly failed to bring any pressure to bear on the Albanese Government to fix this, even as he described the very rationale for doing so.

How do we account for this failure Orwellian failure?

One reason may be the forthcoming RBA review. This bizarre policy undertaking by the Albanese Government, which was born out of the RBA’s failure to sustain enough inflation over the Great Lost Decade post-2010, will now focus on its failure to deliver too much inflation over one year.

The defensive and backward-looking tone and scope of Phil Lowe’s speech tell us much. He is thinking in terms not of the bank’s national interest role so much as he is protecting its (and his) butt.

Let’s not forget that Dr Lowe’s predecessor, Glenn Stevens, is, incredibly, now chairman of Australia’s most policy-corrupting private bank.

Is it really too much to suggest that Dr Lowe has at least one eye fixed on his own post-RBA millions rather than on the Australian economy?

The second reason that we can speculate that the RBA is so steadfastly ignoring the energy danger on its doorstep is that it is reading the tea leaves within the Albanese Government and what it is going to do about the evil gas cartel at the heart of it all.

A few months ago, the RBA was stridently calling out energy inflation as a core problem. Since then, the issue has steadily receded from its communications. Why? Australian gas and power price have fallen from ludicrous highs, but both are still at preposterous highs more than enough to trash the RBA’s inflation outlook.

Has the RBA quietly gotten the message that the Albanese Government is going to act on these prices with stronger domestic reservation for gas and coal? Or is it the opposite? That the RBA has been quietly influenced by an energy cartel that plays the game of mates so exceptionally that having captured the Albanese Government it has now swamped the central bank as well?

After all, the RBA board still has evil gas cartel representation on its board.

I don’t know the answer. What we can say with certainty is that this is the ONLY question that matters to the RBA’s inflation outlook. If the Albanese Government regulates gas (and coal prices) then the bank is on track. If not, it is going to be blown away again by an inflation surge regardless of what happens in other sectors.

I may never be able to holiday again!