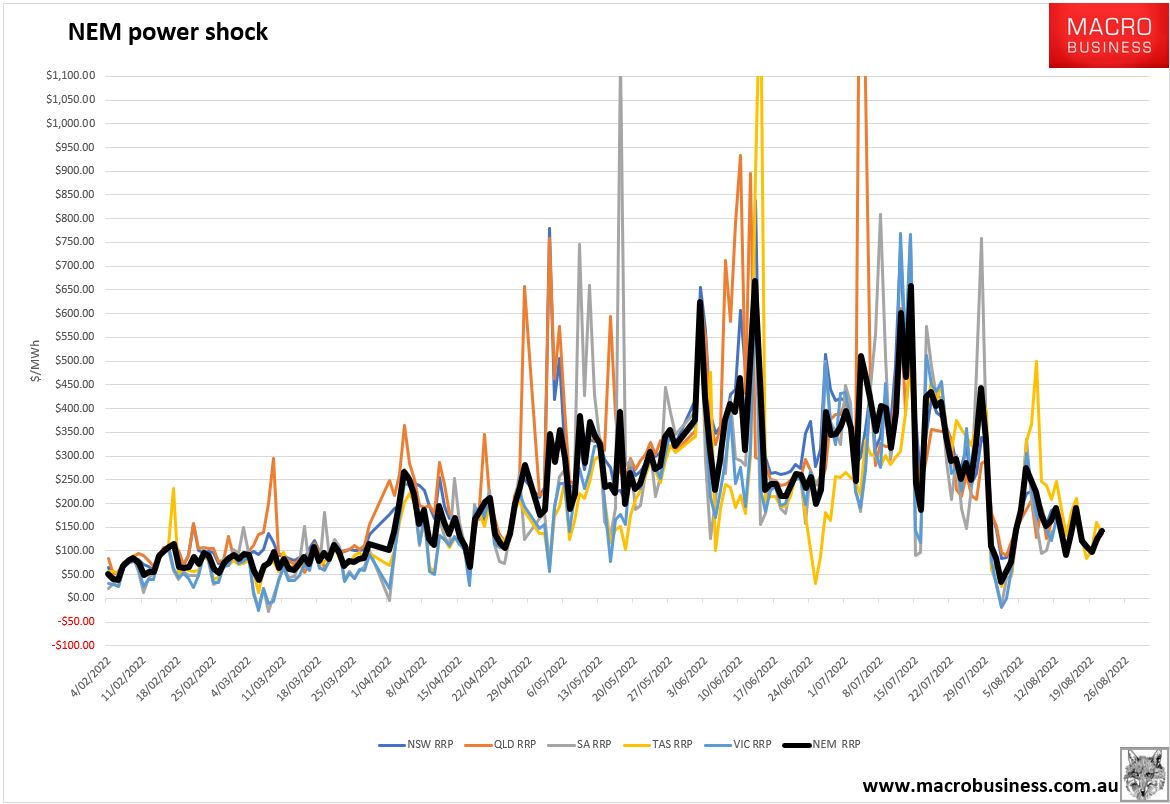

Where is this urgent review of the ADGSM we were promised? I suppose it is stuck in unnecessary and corrupt negotiations with the criminal and war-profiteering gas cartel. Especially so, since Resources Minister Mad King appears captured by those she should be regulating. Are they negotiating or figuring out how high a price they can scam and get away with?

That price today is bouncing around from $15-20Gj. Put another way, it is trading in a range that adds 30-80% to utility bill inflation over the next year:

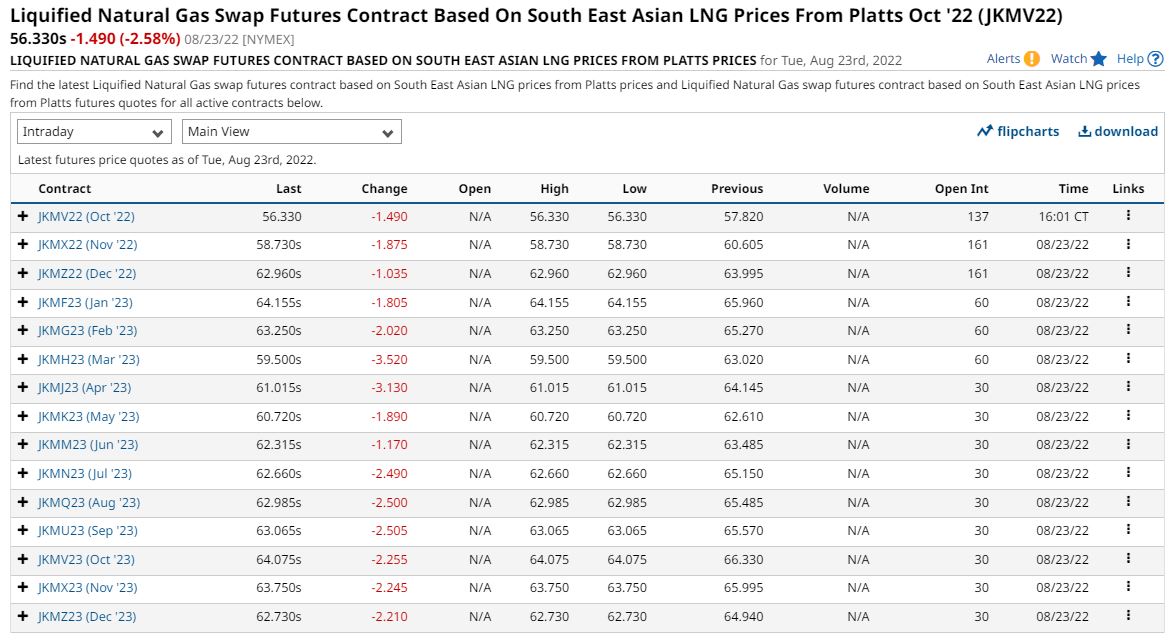

Meanwhile, there was some minor relief in JKM overnight which will determine the local price in a matter of days as the APLNG sixth Curtis Island train resumes operations:

Advertisement

It’s more than a little bit scary to consider that winter prices for JKM don’t usually peak until January and they are already at nearly $100Gj in Asia.

But then, do prices even matter anymore? Not in a failed market:

Advertisement

At one point yesterday morning gas prices rose by 10%. Which, in cash terms, is roughly equivalent to pre-crisis cost of gas.

With gas prices so high it’s quite frightening to see them jump *another* 10%

Given they’re already >10 times the average last decade, it’s going up BY THE ENTIRE AMOUNT GAS USED TO COST in one morning

I’m an economist. I think price signals are useful. Two weeks ago, when discussing how governments should respond to rising energy bills on Radio 4 I gave the economist’s answer: let bills rise to keep the price signal whilst giving households lump sum payments to protect their incomes.

But a lot can change in two weeks.

We have reached the point when European gas pricing is conveying no more useful information. The message, at present, is crystal clear: there is a serious shortage of energy. You could double prices at this point and we would learn nothing new.

Cornwall Insight reckon they imply a domestic energy price cap of over £5,300 by Q2 next year. Citi have notched up their UK CPI forecast at 18.6%. I’m not questioning the maths behind either Cornwall’s or Citi’s calculations but I do not think either is at all politically tenable.

These sorts of numbers imply widespread poverty amongst households, a collapse in discretionary spending, utter ruin for many SMEs and a fair few larger firms too.

In reality the government will not stand idly by and let this happen. The domestic energy price cap will not be allowed to reach £5,000. Firms will receive support with their bills. Perhaps not as much as they need, but a substantial amount.

Liz Truss may be against ‘handouts’ but crises make for unusual outcomes. Gordon Brown, the co-creator of New Labour, found himself nationalising banks. Boris Johnson, perhaps Britain’s most libertarian inclined Prime Minister of modern times, found himself placing the nation under house arrest. Rishi Sunak was pushed into increasing the tax burden to its highest level in decades whilst constantly talking about his love of low taxes.

Liz Truss may be, by instinct, Britain’s most free marketeer PM since the 1980s but she will soon find herself capping prices, ignoring market signals and overseeing a large bailout of corporate Britain.

If energy prices stay at their current levels over the next couple of years, then government debt to GDP is heading for 120%. The only question is the route taken rather than the destination. Either the government can directly borrow the money to subsidise energy bills or it can let prices rip and see debt rise as one price of an even more gut wrenching recession.

A wide ranging support package to cap bills for households and firms has to be the realistic base case. The trickier decisions for the Truss government will come later and be even more unpleasant for them.

Dealing with the costs of high energy bills is going to mean a furlough-scheme type fiscal outlay. And with interest rates heading up the cost of servicing that debt is going to be higher too. The room for the kind of wide ranging, permanent tax cuts that Truss supports simply will not exist.

The second challenge will be even trickier for the Truss government. The government will have no option other than to suppress the price signal coming from the energy market. But capping prices is one thing, it does not (in the short term) deal with the reality that prices are rising for a reason: a genuine shortage of energy.

Once the government has accepted that it can’t allocate energy using a price mechanism, then the only option left will be energy rationing. The politics of that are going to be exceptionally difficult.

Advertisement

Thankfully, the politics of scarcity are a lot easier in Australia because we have none. At least, we should have abundance because we have so much gas. Our scarcity is artificial and criminal.

From the recent ACCC report:

• Joint marketing by incorporated and unincorporated JVs is more prevalent than we expected, with the LNG exporters and some other producers engaging in joint marketing in the domestic market without authorisation. This results in a material reduction in the number of producers competing to supply gas into the domestic market.9

• Exclusivity provisions in GSAs entered into between domestic producers (as sellers) and LNG exporters (as buyers) are restricting the ability of domestic producers to compete to supply gas into the domestic market. These provisions can also reduce the incentive that domestic producers have to develop gas over time and result in development decisions being based on the requirements of the LNG exporters, rather than the domestic market.

• Mergers and acquisitions of other producers, tenements or interests in JVs by larger producers, can result in a reduction in producers competing to supply gas into the market and slow the progress of gas development.

Together with the high degree of concentration in this part of the market, these arrangements contribute to a lack of effective upstream competition in the east coast. They may also increase the risk of coordinated conduct and increase the market power of the LNG exporters. This is concerning, given the supply conditions that are expected to prevail in the east coast in 2023 and beyond, and the reliance that will be placed on the LNG exporters to supply more gas into the domestic market.

Entering into these types of arrangements without authorisation risks breaking the restrictive trade practices provisions in Part IV of the CCA if they amount to cartel conduct, or have the purpose, effect or likely effect of substantially lessening competition.

While in the past producers may have considered that these arrangements would not substantially lessen competition, in a concentrated and tight market the effect on competition can be heightened. We will continue to review some of these arrangements and, where appropriate, consider enforcement action.

Producers should also consider whether they could implement changes to their arrangements to help improve competition and the timely supply of gas to the market as a matter of priority.

Why is Mad King negotiating with a white-collar mafia? Where is the new ADGSM? Why aren’t the Australian people being briefed on what the Government’s objectives are?

Advertisement

In short, where is our government as an energy depression threatens to overwhelm the economy in days for no reason better reason than grand larceny?

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.