This is how the gas cartel operates. It is very adept at lurking in the shadows. It will rort you to death until called out and, when it is, slink away to avoid prosecution.

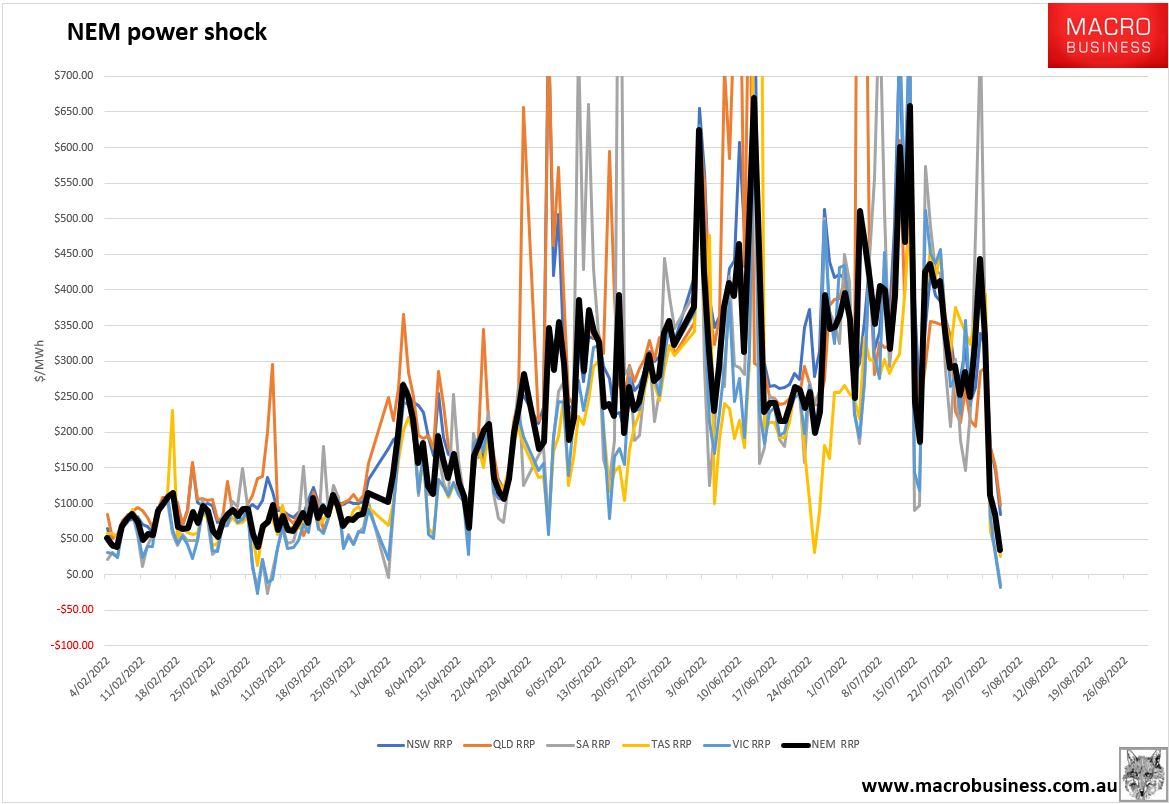

The last week of public scrutiny has collapsed the gas price. Today it is $11Gj in VIC after sitting on the $40 regulated ceiling for months. The wind is blowing too so the electricity price has cratered:

We all had a good laugh a few days ago when I pointed out that the east gas cartel was colluding on how to disguise its collusion:

Australia’s three largest east-coast gas exporters have held an emergency meeting to discuss boosting domestic supplies after federal Resources Minister Madeleine King threatened unprecedented export controls if the industry fails to act first.

Representatives from the three Queensland producers – Origin Energy-backed APLNG, Shell’s QCLNG joint venture and Santos’ GLNG – joined a conference call on Monday afternoon, according to senior gas industry sources familiar with the talks.

The meeting was convened by their industry group, the Australian Petroleum Production and Exploration Association, and discussed the drafting of a non-binding “heads of agreement” to take to government in a bid to formalise their commitment to plugging a shortfall predicted to hit the eastern seaboard next year.”

But there is a very serious side to this that was pointed out in detail in Monday’s staggering ACCC report into the sector:

• The upstream market is highly concentrated and dominated by the three LNG exporters and their associates. In 2021, the three LNG exporters and their associates had influence over close to 90% of the 2P reserves in the east coast, through a combination of their direct interests in 2P reserves, associates, JVs and exclusivity arrangements. This highlights the effective control that the LNG exporters have over the supply and development of gas in the east coast, as well as competition in the domestic market.

• JVs can adversely affect competition if participants do not put in place and adhere to robust ring-fencing arrangements that prevent the sharing of commercially sensitive information, 8 with other projects in which JV participants have an interest. A JV participant can also have the incentive and opportunity to exploit their position in a JV to delay the development of gas if it improves the participant’s competitive position in other projects.

• Joint marketing by incorporated and unincorporated JVs is more prevalent than we expected, with the LNG exporters and some other producers engaging in joint marketing in the domestic market without authorisation. This results in a material reduction in the number of producers competing to supply gas into the domestic market.9

• Exclusivity provisions in GSAs entered into between domestic producers (as sellers) and LNG exporters (as buyers) are restricting the ability of domestic producers to compete to supply gas into the domestic market. These provisions can also reduce the incentive that domestic producers have to develop gas over time and result in development decisions being based on the requirements of the LNG exporters, rather than the domestic market.

• Mergers and acquisitions of other producers, tenements or interests in JVs by larger producers, can result in a reduction in producers competing to supply gas into the market and slow the progress of gas development.

Together with the high degree of concentration in this part of the market, these arrangements contribute to a lack of effective upstream competition in the east coast. They may also increase the risk of coordinated conduct and increase the market power of the LNG exporters. This is concerning, given the supply conditions that are expected to prevail in the east coast in 2023 and beyond, and the reliance that will be placed on the LNG exporters to supply more gas into the domestic market.

Entering into these types of arrangements without authorisation risks breaking the restrictive trade practices provisions in Part IV of the CCA if they amount to cartel conduct, or have the purpose, effect or likely effect of substantially lessening competition.

While in the past producers may have considered that these arrangements would not substantially lessen competition, in a concentrated and tight market the effect on competition can be heightened. We will continue to review some of these arrangements and, where appropriate, consider enforcement action.

Producers should also consider whether they could implement changes to their arrangements to help improve competition and the timely supply of gas to the market as a matter of priority.

This is criminal activity in the plain light of day. Why is the ACCC granting the cartel the latitude to stop breaking the law? This is the functional equivalent of a polite warning if I were to march into the local bank and stick it up with a shotgun.

The ACCC must prosecute the cartel immediately and the Albanese Government install a $7Gj price trigger within a toughened domestic reservation regime.

Otherwise, the cartel will be back at the mother of all heists the moment the spotlight shifts.