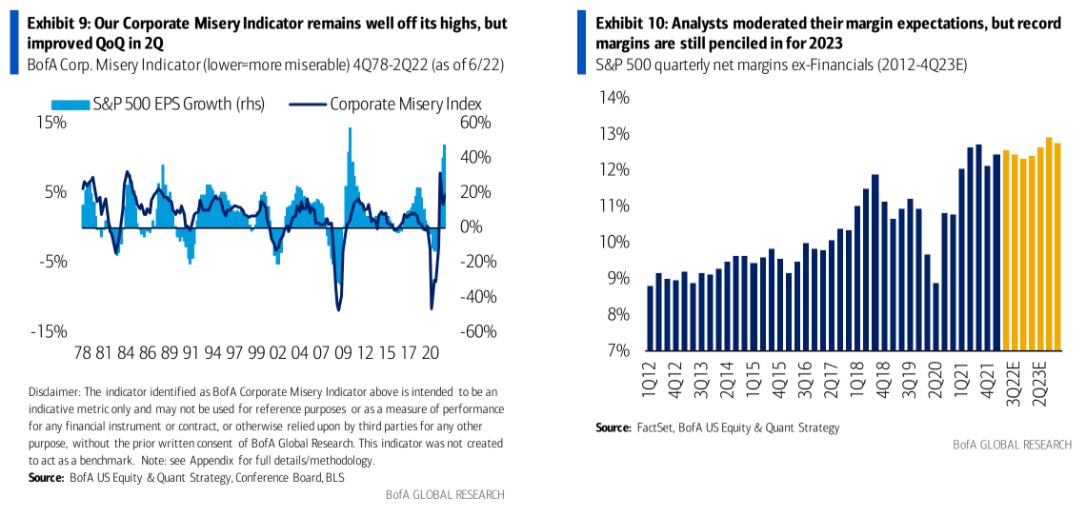

BofA pokes the elephant in the earnings room. As huge inventories are confronted with declining demand, corporate pricing power is going to collapse and margins crater. This is the downside of the inflation trade that is on the offing but not yet priced.

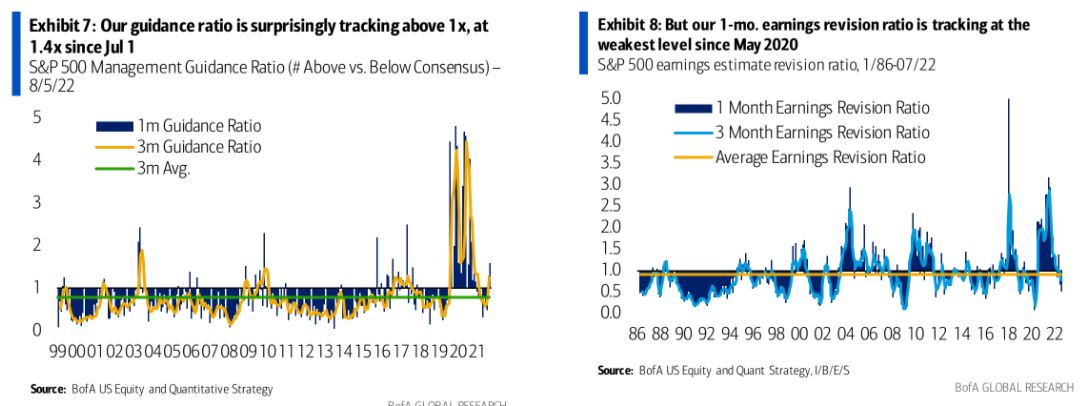

Nearly 90% of 2Q earnings are in and 2Q EPS is tracking a 4% beat at $57.74(+10%YoY) vs. consensus $55.35. 68%/66%/51% of companies beat onEPS/sales/both, much better than the historical average of58%/58%/40%.

Our guidance ratio surprised to the upside, with the ratio of above-vs. below-consensus guidance tracking at 1.4x this earnings season. However, our 1-mo. earnings revision ratio came in at the weakest level sinceMay2020, at 0.5xin July, and 3Q EPS has been revised down by 4% since July 1.We forecast 2023 EPS of $200, 20% below consensus.