Australians that leveraged up to purchase property at the peak of the market risk being trapped in ‘mortgage prison’, according to mortgage experts.

They warn that the combination of rising mortgage rates and falling house prices (negative equity) will impede their ability to refinance because they will no longer meet borrower stress tests, potentially trapping borrowers into expensive mortgages that they will struggle to repay.

Phoebe Blamey, a director of mortgage broker Clover Financial Solutions, described the situation as “a nightmare for many borrowers who are locked in at more expensive rates” because “many lenders are not coming to the party by reducing loans for existing borrowers”. So while “there are better rates with other lenders, they can’t qualify for them… so they are trapped”.

RateCity.com.au research director, Sally Tindall, similarly warned that “property prices are falling, and likely to fall even further next year”. Therefore, “those who bought recently with a 20 per cent deposit may see their equity fall below this level, effectively putting them in mortgage prison”.

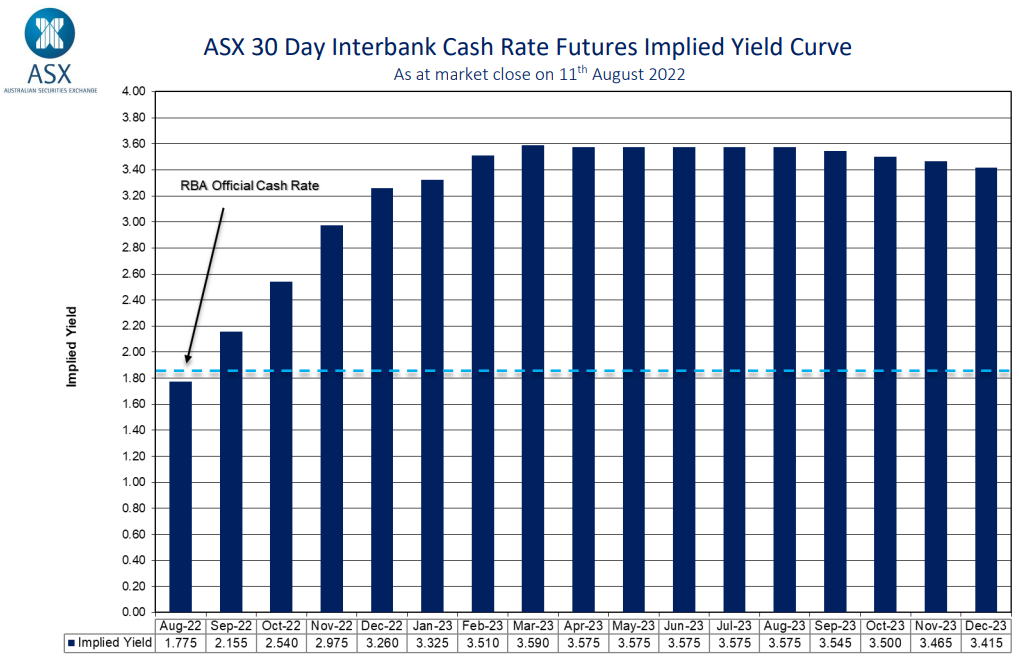

The latest futures market forecast has the official cash rate (OCR) climbing to 3.6% by March 2023, which would be an increase of 1.75% from its current level. It would also mean that the Reserve Bank of Australia (RBA) is only half way through its tightening cycle.

Latest futures market forecasts suggests RBA is only half way through its tightening cycle.

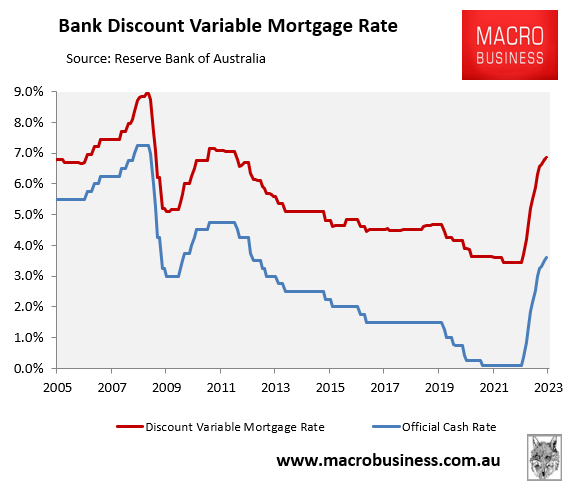

If this forecast came true, it would see Australian mortgage rates soar. Australia’s average discount variable mortgage rate would climb to 6.85% – its highest level since late 2011:

Futures market: Variable mortgage rates to double.

In fact, the average discount variable mortgage rate would rocket to double its level in April 2022 (3.45%) before the RBA commenced its tightening cycle.

If mortgage rates were to rise this aggressively, Australian mortgage holders would obviously face a massive jump in their repayments, which would plunge many into severe financial stress at the same time as their home values tank, especially if they purchased in Sydney or Melbourne.

Many recent buyers would, in turn, be plunged into negative equity and would be unable to switch lenders to a better deal. These borrowers would indeed become “mortgage prisoners”, captive to their banks.