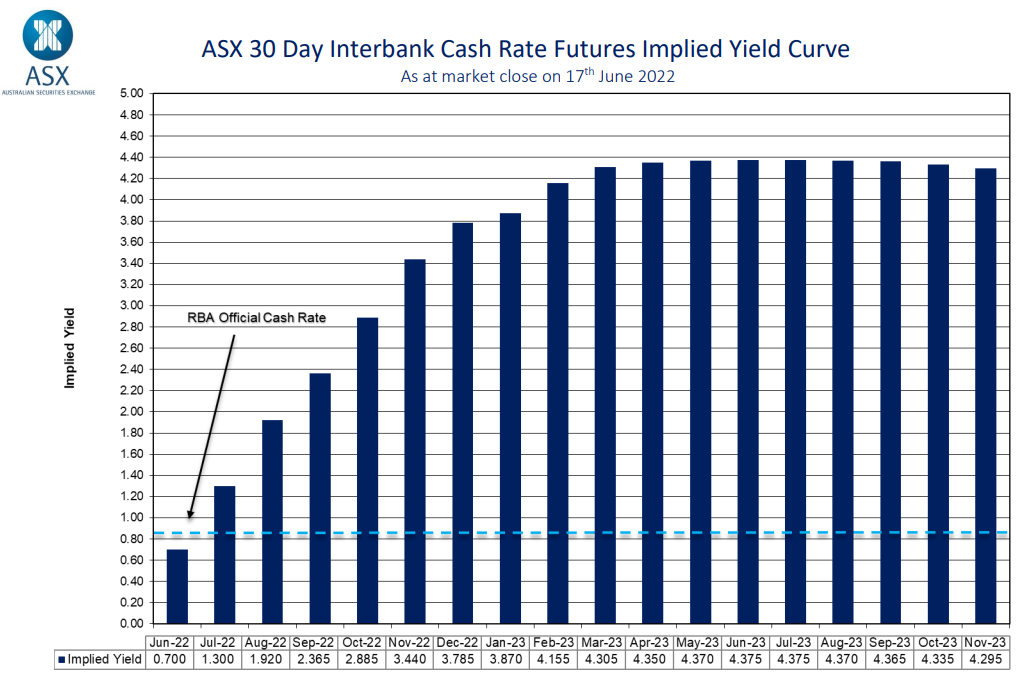

In mid June, the futures market forecast that the Reserve Bank of Australia (RBA) would hike the Official Cash Rate (OCR) to 3.8% by December and to 4.4% by May 2023:

Futures market drinking the interest rate Kool Aid.

According to The AFR, markets have now slashed their forecasts, and are tipping the OCR to only peak at 3%:

Curve Securities director Peter Sheahan said money markets had lowered the peak RBA cash rate pricing to 3 per cent, after the US Federal Reserve signalled it could “pause” interest rate rises following more monetary policy tightening in the coming months.

“The number of RBA hikes and terminal rate has been revised dramatically in just six weeks from 10 hikes, to six hikes and 3 per cent, after the US Federal Reserve’s aggressive action and ‘pause’ comment to give them time to assess,” Mr Sheahan said.

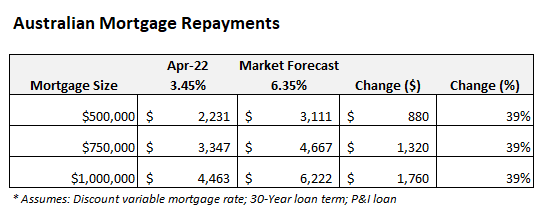

If the market’s latest OCR forecast comes to fruition, then Australia’s average discount variable mortgage rate would lift to 6.35%, up from 3.45% in April. In turn, average principal and interest mortgage repayments would still soar by 39% from their level before the RBA began hiking rates:

The ‘market’ still forecasts big increases in mortgage repayments.

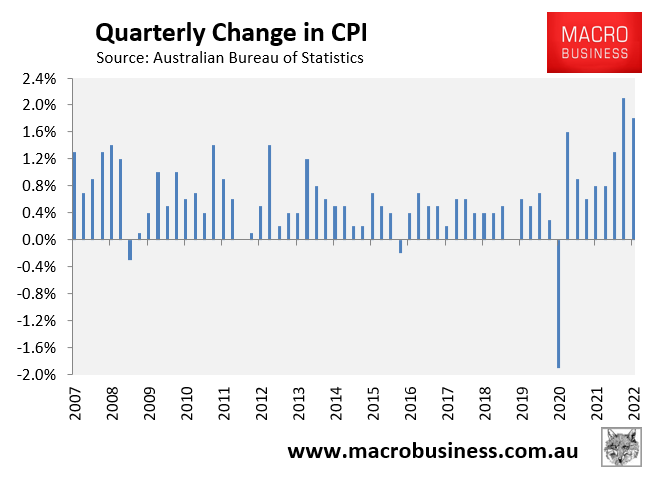

Given CPI moderated in the June quarter, from 2.1% to 1.8% (see next chart), the RBA would be wise to pause after tomorrow’s expected 0.5% rate rise to see how the data evolves.

Australian CPI retraced in Q2.

In particular, the Q2 wage growth data will provide important insight into whether inflationary pressures are becoming domestically driven, rather than primarily imported or weather-related.

The RBA will also likely see that discretionary consumer spending is falling, alongside ongoing sharp falls in house prices.

To put it bluntly, the RBA needs to tread cautiously on rates. Because a 3% OCR by year’s end – as forecast by ANZ, Westpac and the market – risks driving the economy into an unnecessary recession. It would also be followed with aggressive rate cuts by the RBA anyway.