We’ve reached the blowoff profits phase of the COVID commodity mania. The AFR is on its knees sucking the proverbial:

The biggest contributor to Australia’s record trade surplus, BHP, has vowed to be disciplined as it pursues growth in “future facing” commodities after reporting its biggest profit in Australian dollar terms, record dividends worth $23.2 billion and the payment of almost 10 per cent of all federal income tax receipts.

Hmm, well, is it really being disciplined? Looks tempted to me:

BHP boss Mike Henry has reiterated the company’s commitment to a “value over volume” mantra while flagging a possible 40 million tonne expansion of the mining giant’s powerhouse WA iron ore division.

The mining giant announced the proposed capacity upgrade for its Pilbara operations as it surprised the market with a higher than expected full-year profit and dividend, underpinned by a record sales result from WAIO.

The company issued 2023 production guidance for its Pilbara operations of 278–290Mt at costs of $US18-$US19/t, representing a 6 per cent increase on last year.

But BHP has set a medium-term goal of exceeding 300Mtpa from WAIO and flagged a possible expansion to 330Mtpa.

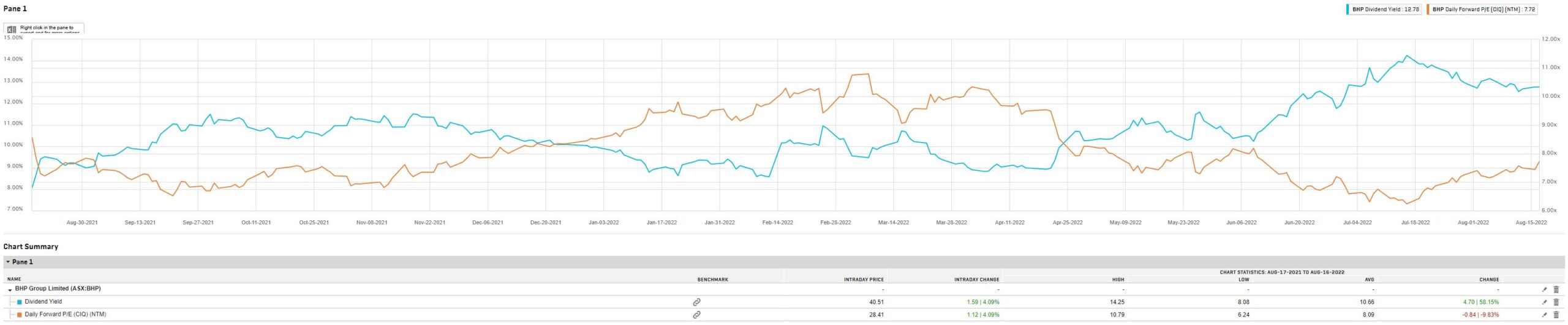

And why not? It is flush with cash and has a very strong balance sheet. What’s not to like with such a huge dividend and being so cheap?

The problem is, these are all signs of an unsustainable top in the cycle not a bottom or even plateau:

- Mining dividends never last. Least of all, those based upon temporary plagues and wars.

- Low P/Es are the time to sell miners, when commodity prices are high and the cash is flowing.

Moreover, the obvious risk to BHP earnings is getting worse not better. China and iron ore are at high risk of another leg down over H2, especially through the Sep/Oct seasonal trough.

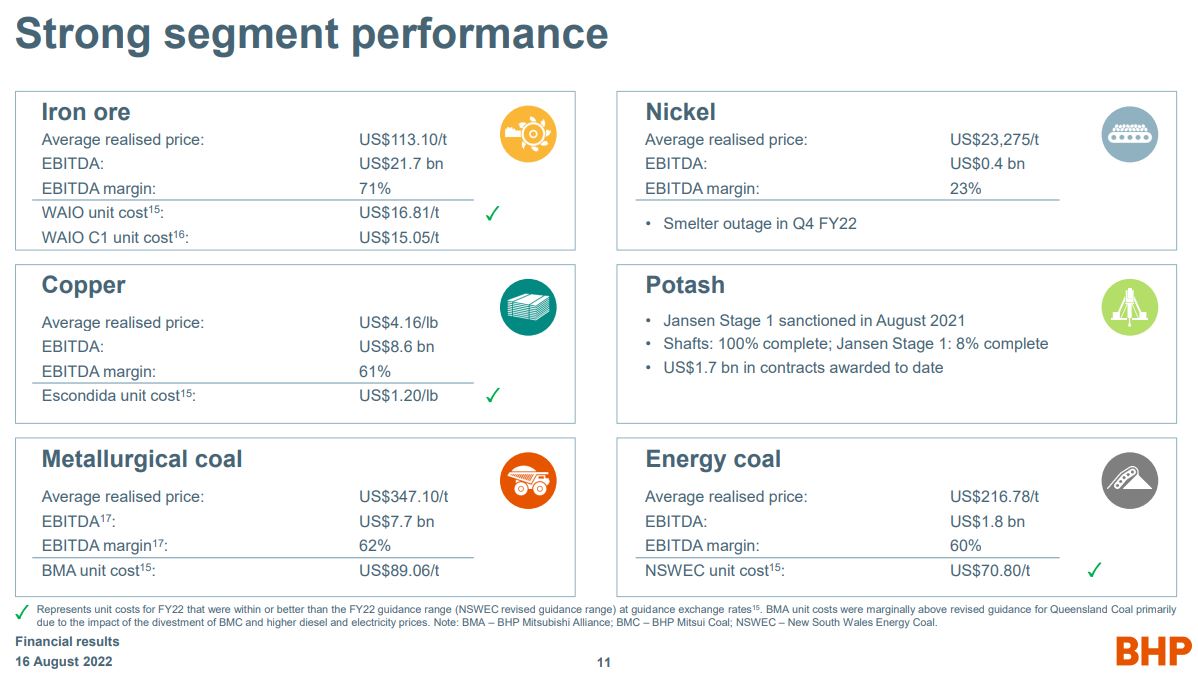

BHP enjoyed an average iron ore price of $113 and coking coal price of $347 over 21/22. That delivered three-quarters of EBITDA:

Currently, coking coal is $230 and iron ore is $104 but both are in the gun for lower.

BHP’s commodity price man, the former Phat Dragon of Westpac, is not bullish exactly but he is not bearish enough:

China’s economy has been nothing if not turbulent in the 2020s to date. First, we saw a spectacular V–shape across calendar 2020, with strong momentum carrying over into the first half of calendar 2021, giving China “first–in, first–out” status in the global pandemic. The positive momentum was then arrested – abruptly – in the September quarter of that calendar year. The “dual control” framework for energy policy, the “zero–growth” steel mandate and the desire to constrain macro–financial risks in the property market were all fierce headwinds for the growth trajectory. The reality of the resulting slowdown, the scale and pace of which was clearly unintended, soon had the authorities announcing a series of counter measures designed to stabilise confidence moving into an important political year in calendar 2022. Calendar 2022 started with promise, partly due to the tilt towards easier policy settings – but then came the COVID–19 lockdowns in the June quarter: a period in which the economy suffered a sequential contraction. Roughly two months into the recovery period from the lockdowns, the flow of data has been somewhat mixed.

A rapid turnaround between the last tightening measure of a cycle and the first easing measure of a new one is not unusual in China. The major uncertainty in such circumstances is how to gauge the appropriate lag between the change in policy stance and the response of real economic activity. Obviously, the blunt force of the lockdowns in the June quarter, and the omnipresent threat of snap civic restrictions that will persist while a material immunity gap in the population remains, complicate the analysis. So too does the present state of the all–important real estate sector.

China’s housing market has often been at the centre of counter–cyclical policy shifts. It is also the biggest wild card in the remainder of calendar 2022 and into calendar 2023. Our current diagnosis is that what ails Chinese housing is not a demand problem – it is a supply–side problem.

More specifically, the resolution of the current issue lies within the nexus of developer balance sheets, macro–prudential controls on the same, and risk–averse financiers, who have lost confidence over the last twelve months or so in the face of high–profile defaults.

It is instructive to compare the present situation to the extended real estate downturn of the mid–2010s. The earlier cycle was characterised by an excessive inventory of unsold properties, with substantial over–building in lower tier cities intersecting with tightening purchase controls on out–of–town investors against a backdrop of policy uncertainty under the anti–corruption drive, property tax pilots and the national housing ownership registry. Such was the depth of the issue that “housing de–stocking” that it became a macroeconomic priority in parallel with the execution of President Xi’s signature Supply Side Reform (hereafter SSR) initiative.

The excess inventory problem at the national level was also the collective expression of hundreds of demand–supply mismatches across China’s various city tiers. The resolution required a transfer of real assets from the balance sheet of developers to the balance sheet of households, and that in turn required an increase in purchasing power and regulatory forbearance on the out–of–town investor question. The transfer was ultimately unlocked through a considerable expansion of mortgage loans and a more lenient approach to investors.

The upswing began tentatively, with the average historical lag relationship between the leading indicators and building activity comfortably exceeded, but ultimately an enduring upswing in sales and starts was put in place. It had a lower peak but a longer tail than prior cycles. The shadow of this cycle is still visible in the pipeline of work under construction today – which is part of the problem. Developers have been incentivised to start multiple projects but not to complete them in timely fashion. This oddity stems from the fact that buyers need to compete for access to developments by paying very large down–payments – 100% up front – a practice that has evolved due to the extraordinarily high demand for property assets in China which has historically put developers in a very advantageous bargaining position. If they choose to, developers have been able to dawdle their way through projects after the initial phase without repercussion – prioritising the majority of their capital instead for the acquisition of land and the initiation of new projects.

The authorities have progressively recognized that this issue was creating unhealthy imbalances in the real estate market. For some years, the response was to tread relatively softly, reflecting the sector’s central role in employment, the credit–collateral system, and the storing of wealth. National level housing policies have been directed towards limiting speculation, modest direct interventions via public housing and shanty town reconstruction and the building up of rental markets. These measures did not tackle the root causes of the starts/completion imbalance, one of which was of course the incentive matrix faced by developers. The enormous wedge between the volume of starts and completions that opened across 2016–2019 made this abundantly clear. The response was to place developers into a traditional SSR template, with specific macro–prudential guardrails now known as the “three red lines” introduced in August 202016.

These regulations, finally, increased the incentive for leveraged developers to complete projects in timely fashion, as running down their liabilities to off–the–plan buyers counts towards the –10 percentage point reduction in the liability–to–assets ratios required of the sector. This has seen completions out–perform starts. But with most of the sector coming under financing pressure since Evergrande’s problems came to light roughly a year ago, even working capital has become an issue for some developers. That has led to a very slow supply response to the easier policy measures enacted to boost the demand side of the housing market; a distinct lack of progress on many semi–finished projects; and disgruntled purchasers in multiple locations threatening mortgage servicing strikes.

This latter factor may have been the final straw that forced the authorities’ hand to intervene directly on the supply–side. Not long after this story created a local media stir, it was made known that a state–backed vehicle would be created to backstop financially distressed developers and get liquidity flowing to the sector again. The Politburo meeting of late July released some high–level details, alongside a resolute statement to “stabilise the real estate market” and “ensure housing delivery”.

This episode shows yet again that at this stage of China’s development, real estate is so significant in terms of its impact on employment, local government finances and consumer confidence, not to mention the backward linkages into heavy industry, that anything more than a shallow dip is difficult to absorb whilst also retaining desired levels of macro stability.

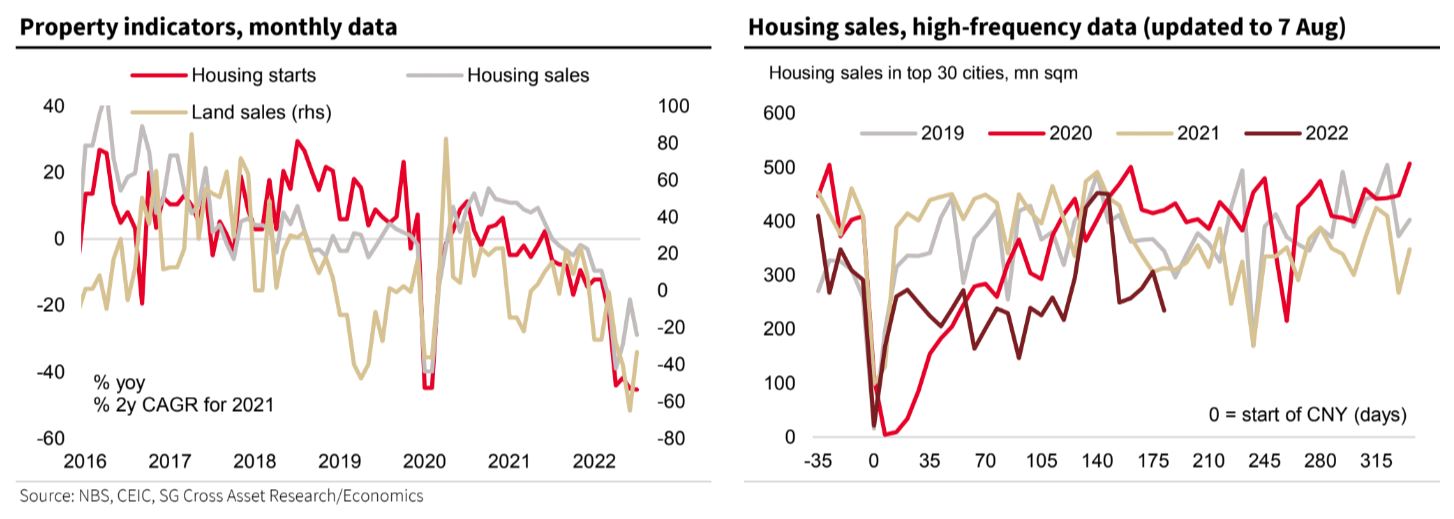

Turning to the specifics now, this is how the major housing data stood as of June 2022 (year–to–date, YoY unless otherwise stated). The volume of housing starts – the key indicator for contemporaneous steel use in real estate – have declined by –34.4%. Sales volumes declined –22.2% (weighed down by pre–sales at –27%: existing home sales rose +16%). The equivalent comparisons for housing completions – the key indicator for contemporaneous copper use in real estate – was –21.5%. Floor space under–construction was tracking at –2.8%; land area sold was –48.3% YoY and developer financing was –25.3%.

A final observation on housing: the scaled inventory of unsold dwellings is close to historical lows as we move into this next cycle phase. A sustained period of weak starts has diminished the pipeline of work, and the needed focus on completions has been delayed. That implies that despite the challenges on the supply side of the industry, risks for housing prices are not skewed downwards. In fact, the reverse may well be true.

To my mind, that’s wrong. The most consistent trend in Chinese policymaking in the past 18 months has been the determination not to stimulate. Beijing has engineered the annihilation of the runaway property sector and then happily let it burn. Every stimulus step has been reluctant and late. It has even missed and abandoned growth targets. The last Politburo meeting mentioned neither the property bailout fund nor additional allocations of credit for local government infrastructure vehicles.

Moreover, there is little sign of a turn in any of it:

There are 90m empty apartments now losing money with the constant refrain coming from Beijing of “houses are for living in, not speculation” that could hit the market and, contrary to Phat’s assertion, there is already a glut of unsold stock as well, especially in lower tier cities.

It looks to me like authorities are very comfortable to pace stimulus such that property keeps adjusting lower. To wit, sales and starts:

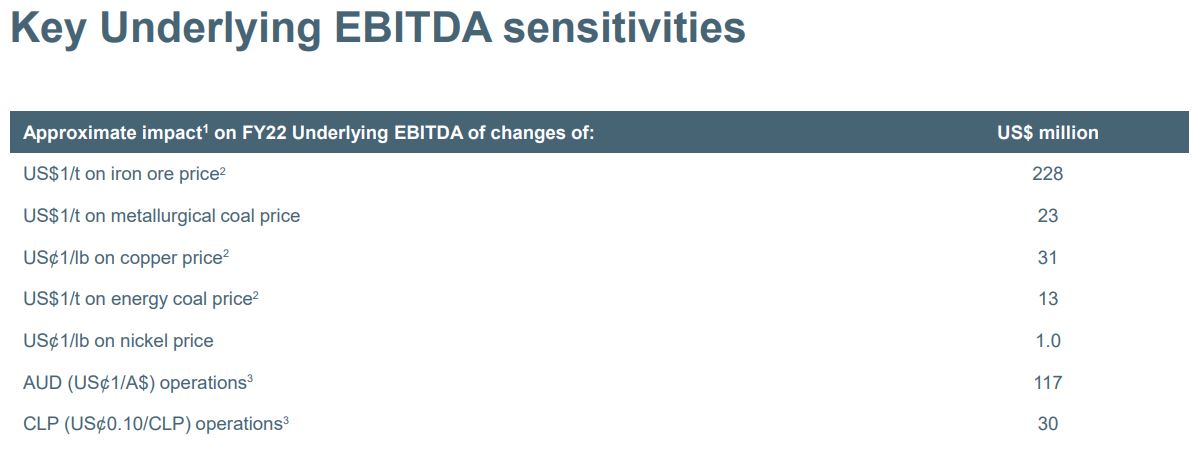

My forecast for the iron ore price is to touch $60 before year-end, and that by itself will wipe $17.2bn from EBITDA annualised:

If you think that the dividend will survive that then I’ve got a bridge I will sell you.

When BHP sold its oil division it turned itself into a giant FMG and now it will suffer from the same wild volatilities.

A reminder: this post is not investment adice.