The Reserve Bank of New Zealand (RBNZ) today hiked the official cash rate (OCR) by another 0.5% – the fourth consecutive double rate hike. This lifted the OCR to 3.0%, up from the record low 0.25% in August 2021. It also took the OCR to its highest level in seven years.

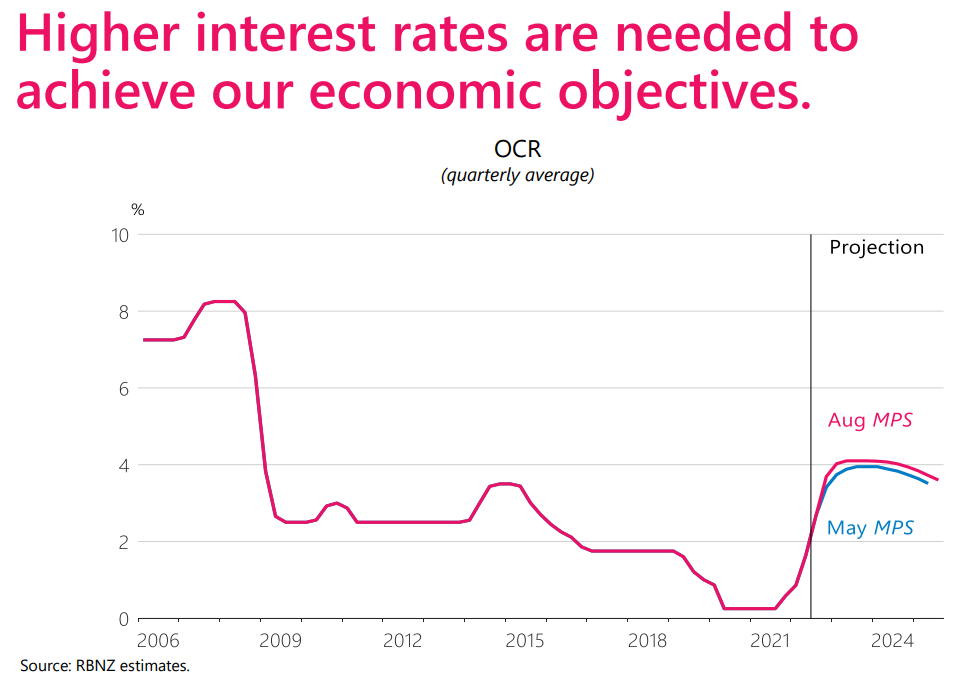

In announcing its decision, the RBNZ noted that “inflation is higher than target, and employment is well above its maximum sustainable level”. Accordingly, “the New Zealand economy needs to go through a period of more moderate growth to better match demand with production capacity”, and “a higher OCR is needed to achieve our economic objectives”.

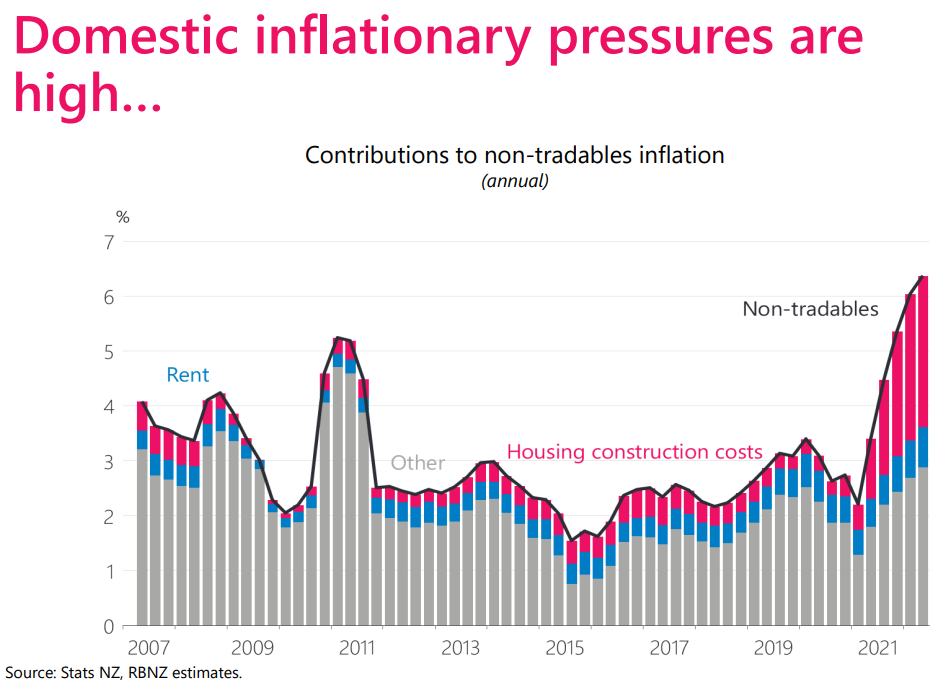

The RBNZ’s data pack attached to the decision noted that “domestic inflationary pressures are high”:

Advertisement

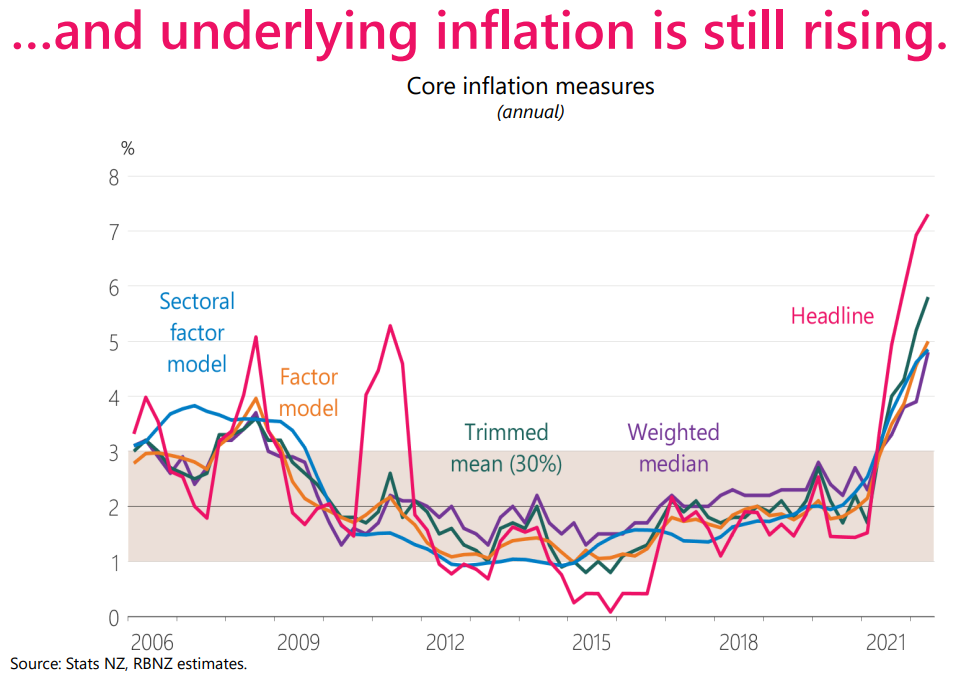

Moreover, “underlying inflation is still rising”:

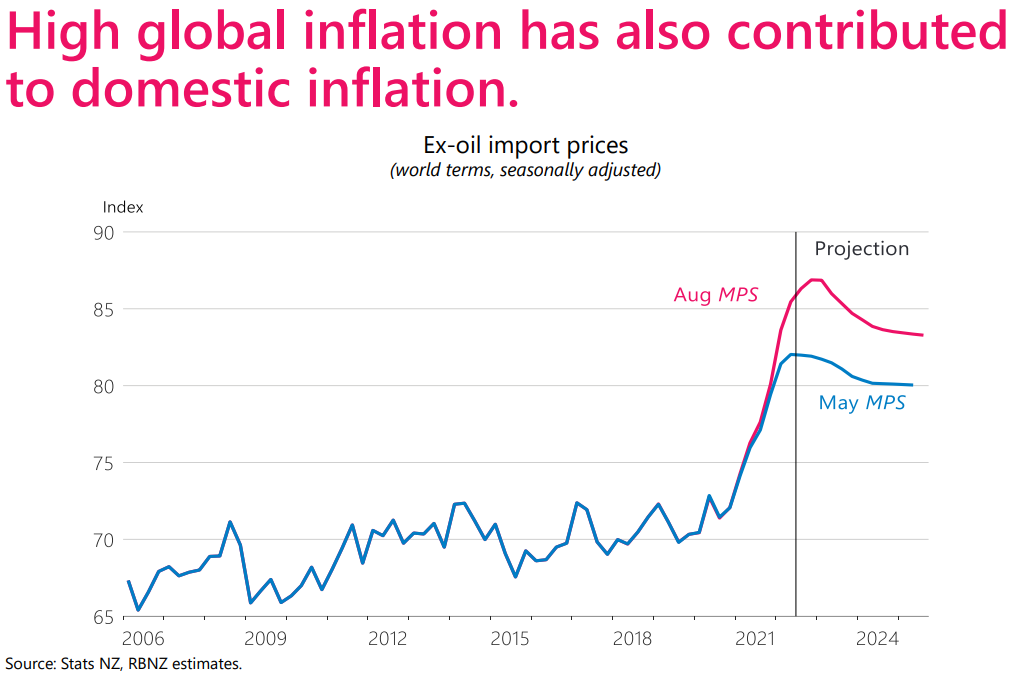

The RBNZ has also revised up its inflation forecasts on the back of high global (imported) inflation:

Advertisement

Accordingly, the RBNZ “committee members agreed that monetary conditions needed to continue to tighten until they are confident there is sufficient restraint on spending to bring inflation back within its 1-3 percent per annum target range” and “remains resolute in achieving the Monetary Policy Remit”.

Indeed, the RBNZ has lifted its OCR forecast above 4% by the middle of next year, with rate cuts not likely until late 2024. Previously it had forecast an OCR peak slightly below 4%:

Advertisement

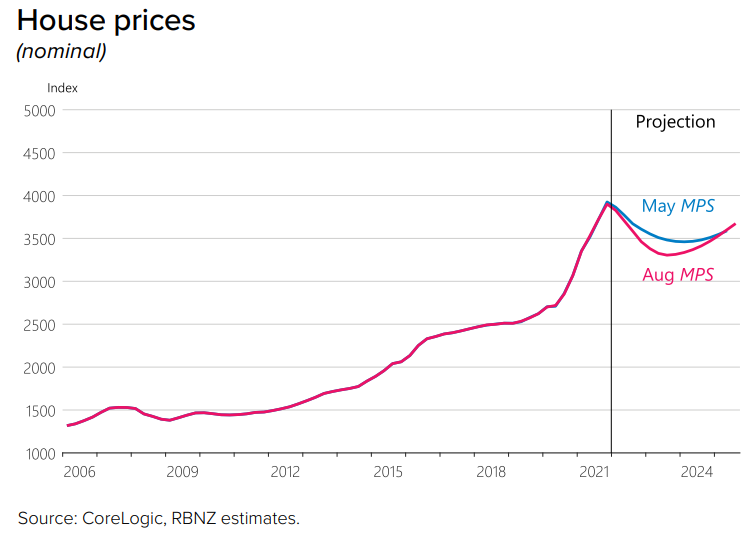

The RBNZ has also projected a bigger 15% decline in house prices:

While there is considerable uncertainty about the outlook for house prices, the central projection assumes that prices will continue to decline until the September 2023 quarter. This would result in a total decline of 15 percent from the December 2021 quarter peak, slightly more than assumed in the May Statement. Lower house prices and higher mortgage rates are assumed to result in weaker household spending, as households feel less wealthy and more of their incomes go towards servicing their debts.

Advertisement

In short, the RBNZ’s aggressive monetary tightening will continue, which will place further strong downward pressure on New Zealand house prices, which are already in freefall.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.