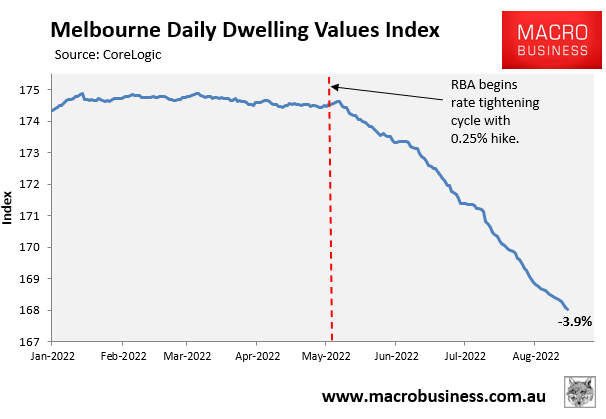

Much like Sydney’s, Melbourne house price losses have accelerated, with values down 3.9% from their peak:

Melbourne house prices plummeting after RBA rate hikes.

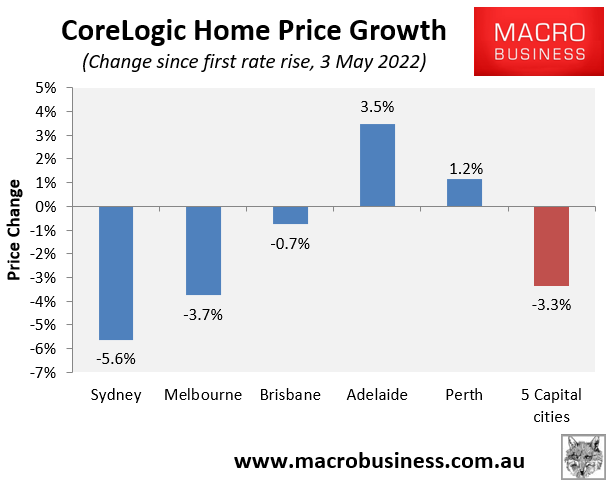

Melbourne dwelling values started falling sharply after the Reserve Bank of Australia’s (RBA) initial interest rate rise on 3 May. Since that first hike, Melbourne’s dwelling values have plummeted by 3.7%. Alongside even heavier falls across Sydney (-5.6%), these two capital cities have driven a 3.3% decline at the 5-City aggregate level over the rate hiking period:

Sydney and Melbourne suffer heavy price falls after RBA rate hikes.

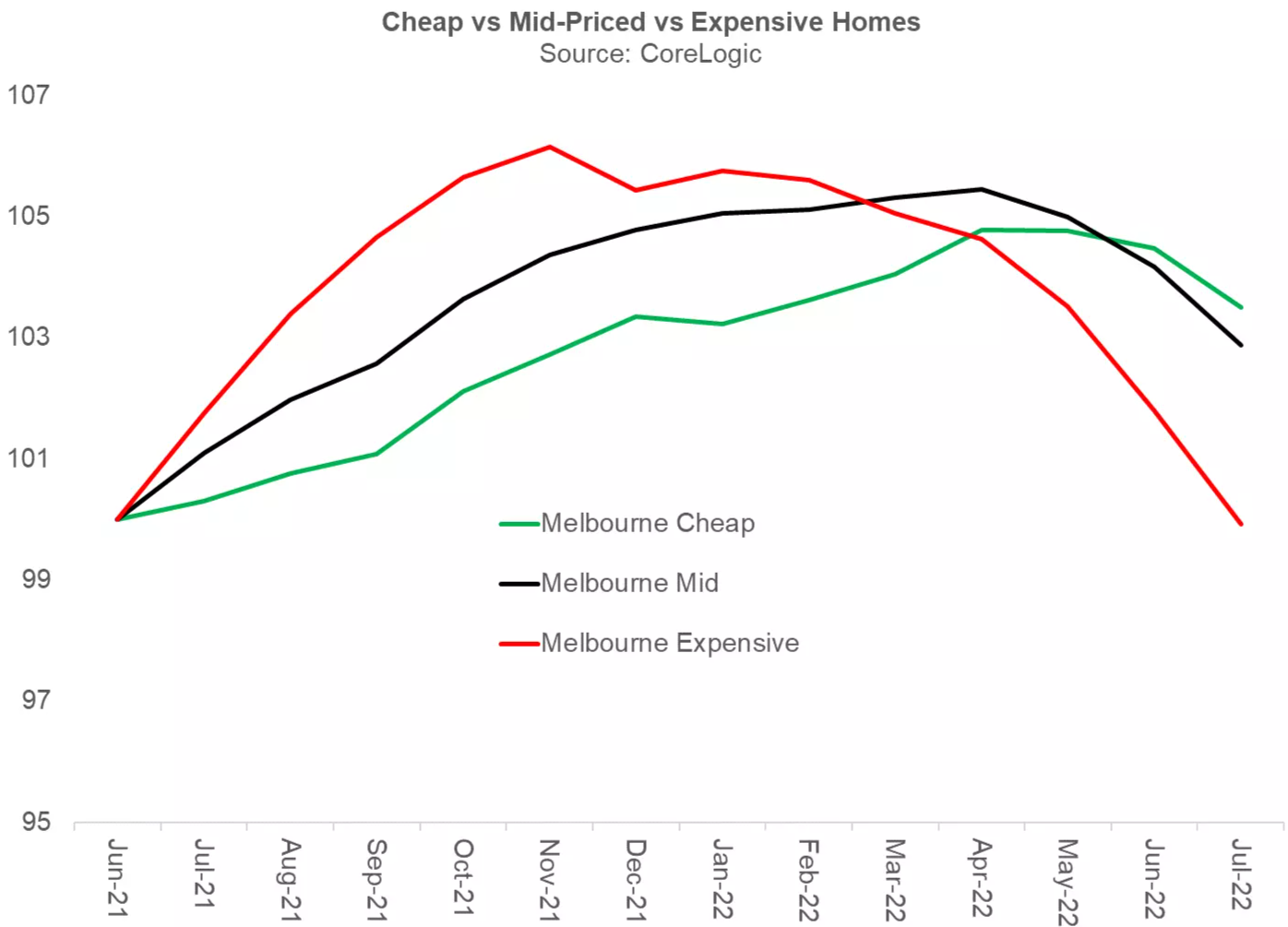

Like Sydney, Melbourne’s dwelling price falls have been driven by the expensive end of the market – i.e. the top 25% of dwellings by value – where prices had fallen by around 6% as at the end of July:

The premium 25% of Melbourne’s housing market has experienced the sharpest price falls.

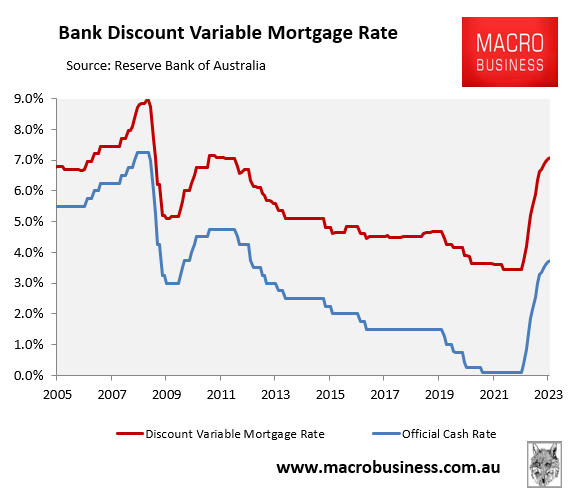

The latest futures market forecast has the official cash rate (OCR) peaking at 3.7% in May 2023.

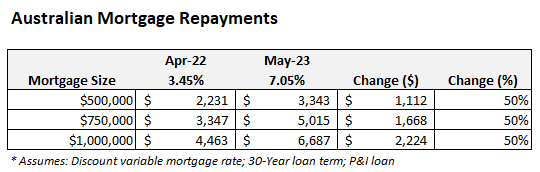

This would mean that the average discount variable mortgage rate would soar to 7.05%, more than double the 3.45% that existed in April 2022:

Futures market: Mortgage rates to more than double.

This would represent the highest discount variable mortgage rate since late 2011. In turn, it would lift mortgage repayments a whopping 50% versus their level in April 2022 immediately before the RBA’s first rate hike:

The impact would be especially damaging for Sydney and Melbourne house prices, given they have the nation’s most expensive homes and biggest mortgages. As shown in the table above, monthly mortgage repayments would soar by $1,668 on a $750,000 mortgage, or by $2,224 on a $1,000,000 mortgage.

Accordingly, Sydney and Melbourne house prices would plunge under the market’s OCR forecast, probably by more than 20%.

Of course, it is my view that the market’s OCR forecast is overly hawkish and that the RBA won’t lift rates nearly as high. In which case, house prices will “correct” rather than “crash”.

Either way, both markets are facing their biggest peak-to-trough price falls in generations. Pass the popcorn!