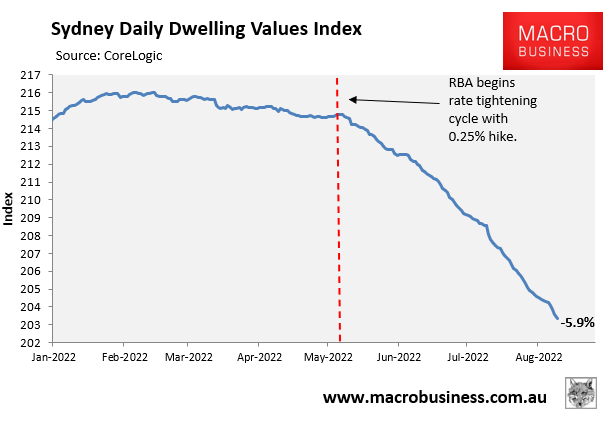

Sydney’s house price crash is accelerating with dwelling values now down 5.9% from their peak and quarterly losses running at their fastest pace since 1983:

Sydney house prices fall at their fastest pace since 1983.

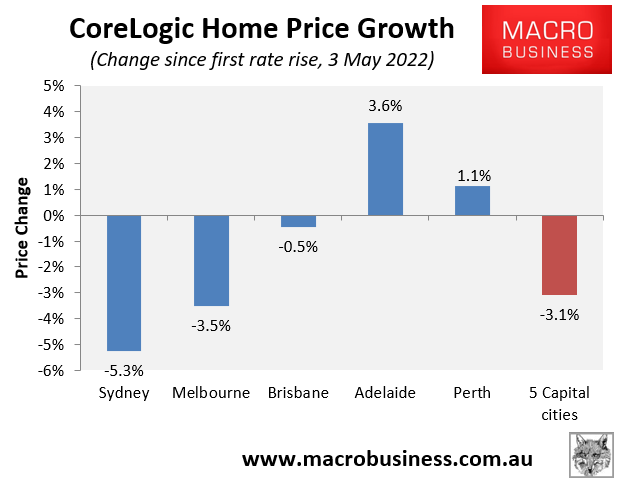

As clearly illustrated in the chart above, Sydney dwelling values began falling sharply following the Reserve Bank of Australia’s (RBA) first interest rate hike on 3 May. Since that first hike, Sydney dwelling values have plummeted an extraordinary 5.3% – well in excess of any other Australian market:

Sydney suffers heavy price falls after rate hikes.

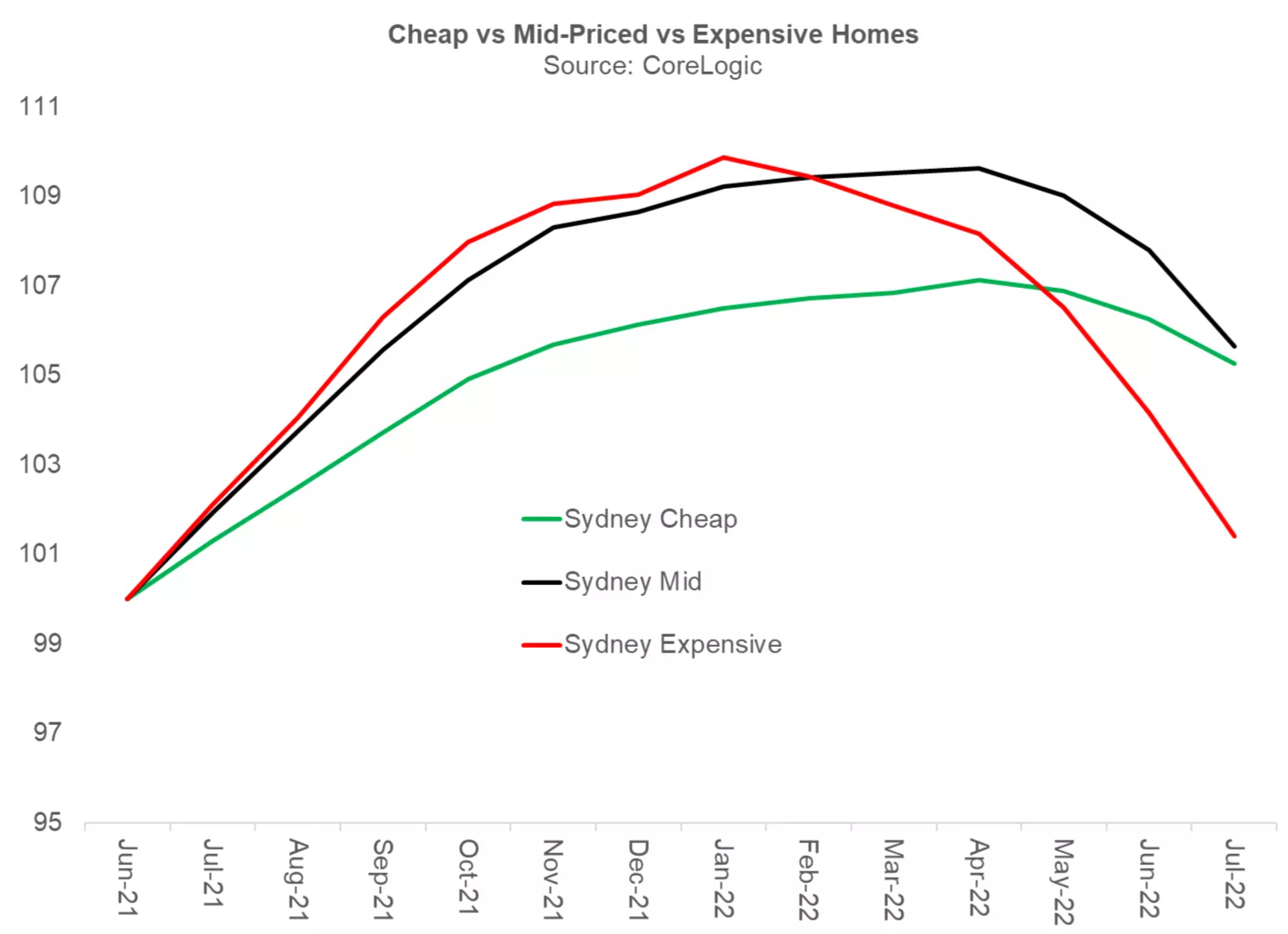

Sydney’s price falls have been driven by the premium end of the market – i.e. the top 25% of homes by value – where values have fallen by around 9%:

The most expensive 25% of Sydney’s housing market has experienced the biggest price falls.

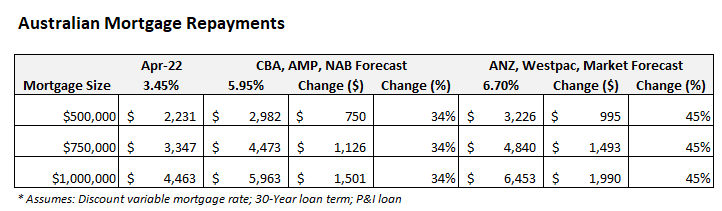

Economist predictions for how far the RBA will hike rates vary, ranging from a peak in the official cash rate (OCR) of around 2.6% (CBA, AMP and NAB) to a peak of 3.35% (ANZ, Westpac and the futures market).

This means that the OCR should rise another 0.75% to 1.50% depending on which forecast comes true, inferring a discount variable mortgage rate of between 5.95% and 6.70%.

Both scenarios would present a big lift in monthly mortgage repayments versus their level in April 2022 immediately before the RBA’s first rate hike.

As shown in the table below, mortgage repayments would rise by between 34% and 45%, representing a lift in monthly repayments of between $1,126 and $1,293 on a $750,000 mortgage:

Sydney mortgage holders facing a massive lift in repayments.

Sydney house prices would likely fall hard under either interest rate scenario, ranging from a steep correction (circa 15-20% fall peak-to-trough) to an outright crash (over 20% decline).

The market’s fate is in the hands of the RBA.