Terry McCrann wrote a strange article in the Weekend Australian arguing that the Reserve Bank of Australia’s (RBA) interest rate hikes are actually “super stimulatory” because the real interest rate has fallen:

In Australia, at the end of 2021, the RBA’s official cash rate was 0.1 per cent. Inflation for the year was 3.5 per cent.

Now the RBA’s cash rate is up to 1.85 per cent. But inflation for the year to June was 6.1 per cent.

In real terms, over the year so far, the RBA has cut its official rate – from minus 3.4 per cent to minus 4.25 per cent; going from super-stimulatory to even more super-stimulatory.

Furthermore, the RBA expects inflation to increase to 7.8 per cent by the end of the year. It will certainly be higher than 6.1 per cent well before that, in the next print for September.

But take the RBA’s 7.8 per cent; it has now set its rate at minus 5.95 per cent relative to where it believes inflation is headed.

Restrictive? Tough? My rear end.

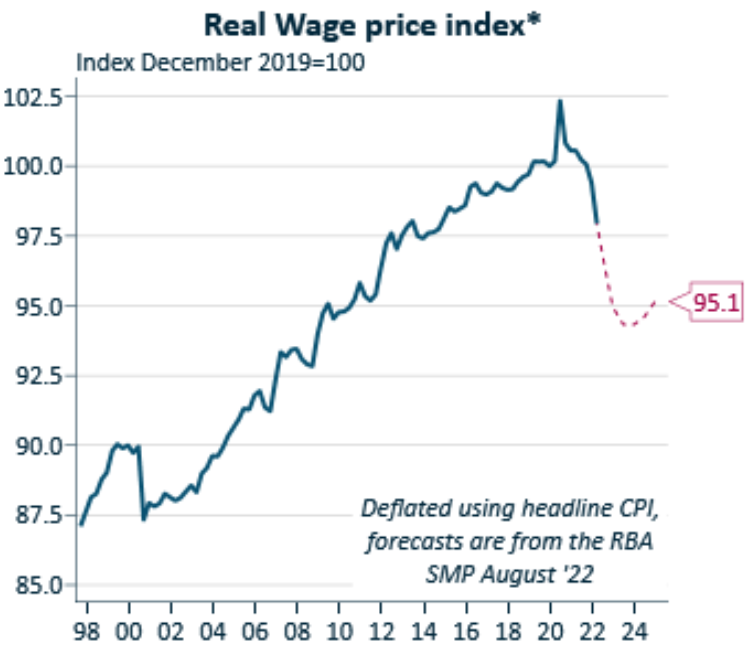

If it was the 1970s and Australian wages were automatically adjusted to match CPI, McCrann might have a point. But this isn’t the 70s, and Australian real wages are falling at an alarming rate. In fact, they will fall to 2009 levels if the RBA’s forecasts for wages and inflation come to fruition:

RBA SoMP: Aussie real wages to plunge to 2009 levels.

Unlike the 1970s, Australia’s inflation is not being driven by soaring wages (which are actually disinflationary), but by soaring costs – think petrol, energy and food. Inflation is primarily supply-driven, not demand-driven, and is badly eroding Australian’s disposable income because their wages are not keeping pace.

Thus, to claim the RBA’s rate hikes are “super stimulatory” is outlandish, when the opposite is true. Further rate hikes will merely drain household disposable incomes even further by lifting mortgage repayments.

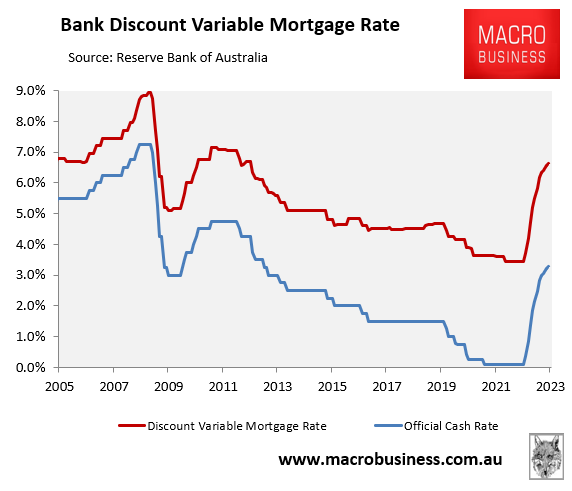

Consider the latest ANZ and Westpac forecast for the official cash rate (OCR). They tip the OCR to peak at around 3.25% by early next year, which would take the average discount variable mortgage rate to 6.60%, up from 3.45% in April 2022 before the RBA commenced its tightening cycle:

Mortgage rates to rise to 2012 levels.

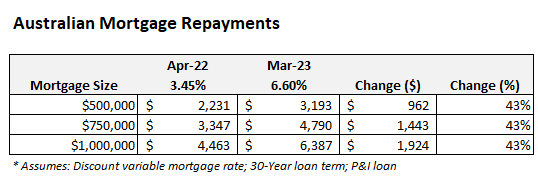

This would represent Australia’s highest discount variable mortgage rate since 2012. It would also lift principal and interest mortgage repayments by 43% against their level in April 2022:

In dollar terms, a household with a $500,000 mortgage would see their monthly repayments rise by $962, whereas a household with a $1 million mortgage would see their monthly repayments soar by $1,924.

The futures market’s OCR forecast is even more bullish, tipping a peak OCR of 3.70% by May 2023, implying a discount variable mortgage rate of 7.0%.

If this looks like “super stimulatory” monetary policy, Terry, I have a bridge to sell you.