Here it is from the horse’s mouth. The RBA is now forecasting 6.25% inflation to June 2023 and more than half of it is the energy cartels!

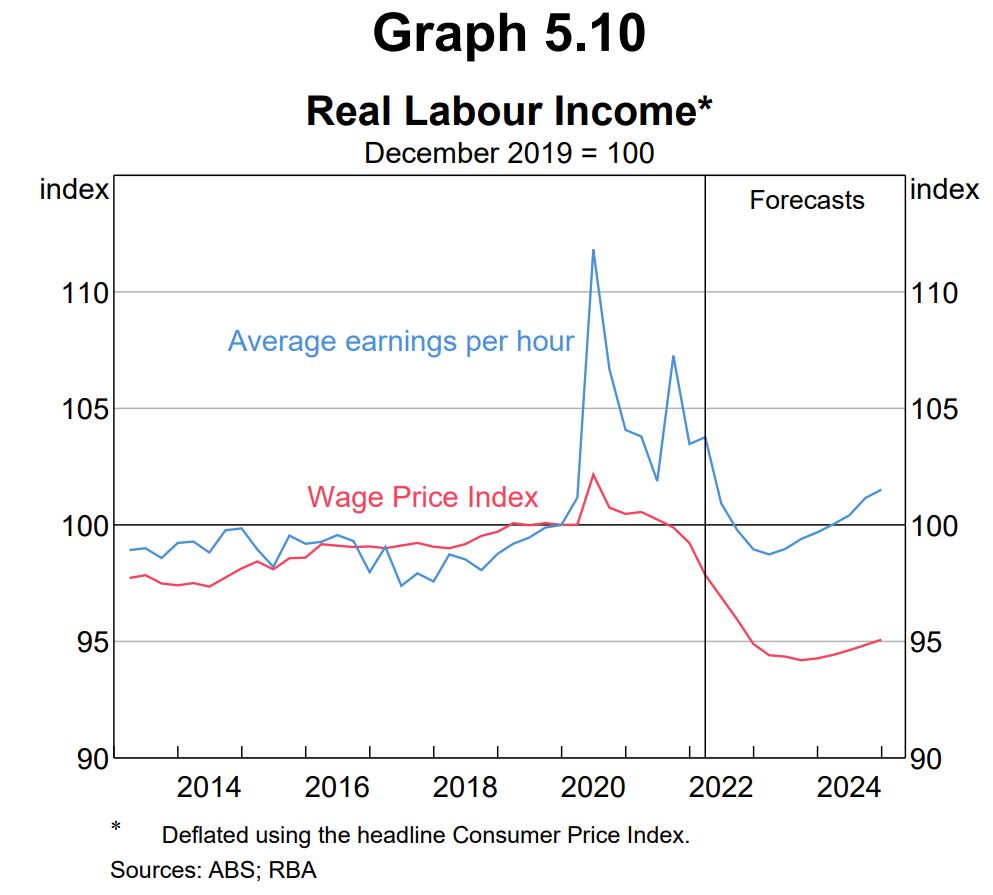

Moreover, the real income losses continue into 2023 as the price rises keep coming. Check out the shocking forecast for real wages:

In other words, if Albo’s cowards do nothing about the energy cartels, they are going to deliver the largest drop in living standards in living memory.

Advertisement

It will make the Coalition’s lost decade look like a picnic as more than twice the loss of purchasing power will transpire over one-third of the time.

Why? The RBA makes it very clear with a breakout section of “special interest”:

Wholesale electricity prices in the National Electricity Market (NEM) have increased sharply over the past six months, to be around four to five times higher in June and July than at the start of the year (Graph A.1). While futures markets suggest that wholesale electricity prices will decline over the coming quarters, they are expected to remain high relative to 2021. Wholesale gas prices are also significantly higher than one year ago.

These higher wholesale prices will be passed through to retail electricity and gas prices for households and businesses over time, adding to Consumer Price Index (CPI) inflation. Such price increases directly affect inflation because these two items account for about 3½ per cent of the CPI basket. They also indirectly affect inflation, as businesses gradually pass these higher costs onto consumers via higher prices for goods and services.

Graph A.1

A combination of factors has caused wholesale electricity prices to rise sharply

The NEM is the wholesale market through which generators sell and retailers buy electricity. Electricity generators submit bids into the NEM signalling how much electricity they are willing to supply and at what price; the generators that bid the lowest are then chosen to generate electricity to meet demand. The wholesale electricity price – or the ‘spot price’ – is the bid offered by the highest-bid generator that is chosen. The NEM operates across Queensland, New South Wales, the ACT, Victoria, South Australia and Tasmania. Western Australia and the Northern Territory each have separate electricity systems and regulatory arrangements.

Around 60 per cent of electricity generation in the NEM stems from coal-fired power. As such, disruptions in several large coal-fired power plants over recent months put pressure on the supply of electricity. A number of plants have been offline in recent months, with some facing unplanned maintenance problems. Other plants produced less power than usual due to a combination of factors, including difficulty accessing sufficient coal because of supply chain issues and illness-related staff absenteeism, and/or production at some coal mines being disrupted by rainfall and extraction difficulties. As a result, coal-fired electricity generation has been substantially lower in 2022 than in recent years (Graph A.2).

Graph A.2

Another factor that has put upward pressure on electricity prices is the sharp increase in domestic and overseas thermal coal spot prices since the start of the year, from already elevated levels (Graph A.3). While many coal-fired generators source coal through long-term contracts or from their own mines, some source coal from spot markets. Moreover, in aggregate, generators have sourced a larger-than-normal share of coal from the spot market recently because of disruptions to usual coal supplies. As a result, generators have increased the price at which they are willing to supply electricity, increasing prices in the NEM.

Graph A.3

Meanwhile, total demand for electricity from the NEM was slightly higher in May, June and July this year compared with the same time in previous years (Graph A.4), coinciding with below-average temperatures on the east coast.

Graph A.4

Lower coal-fired generation and higher electricity demand in the NEM has resulted in greater use of higher-cost gas-fired power plants to meet demand. The cost of gas-fired generation in early 2022 was almost double that seen in early 2021, with domestic wholesale gas prices rising from ~$6/GJ to ~$11/GJ over the year (for comparison, export-parity prices were around $40/GJ in early 2022). However, the most significant price jump occurred in early May, when the increase in demand for gas-fired electricity generation drove a sharp increase in domestic wholesale gas prices, which reached $40/GJ by the second week of May and have remained around this level since (Graph A.3).[1] This higher price for wholesale gas inputs has led to even higher gas-fired electricity generation costs, and therefore higher wholesale electricity prices.

Lower-than-expected output from renewables generation for a time may have also contributed to the increase in wholesale electricity prices. Overall, to date, renewables generation has been higher in each month of 2022 compared with previous years, largely due to an increase in capacity. However, electricity produced per unit of installed renewables capacity has been lower than in previous years, partly reflecting adverse weather on the east coast. This may have put further pressure on wholesale electricity prices if market participants had anticipated that renewables generators would supply more electricity into the NEM. Lower-than-expected output from rooftop solar may have also led households and businesses to demand more electricity from the NEM in recent months.

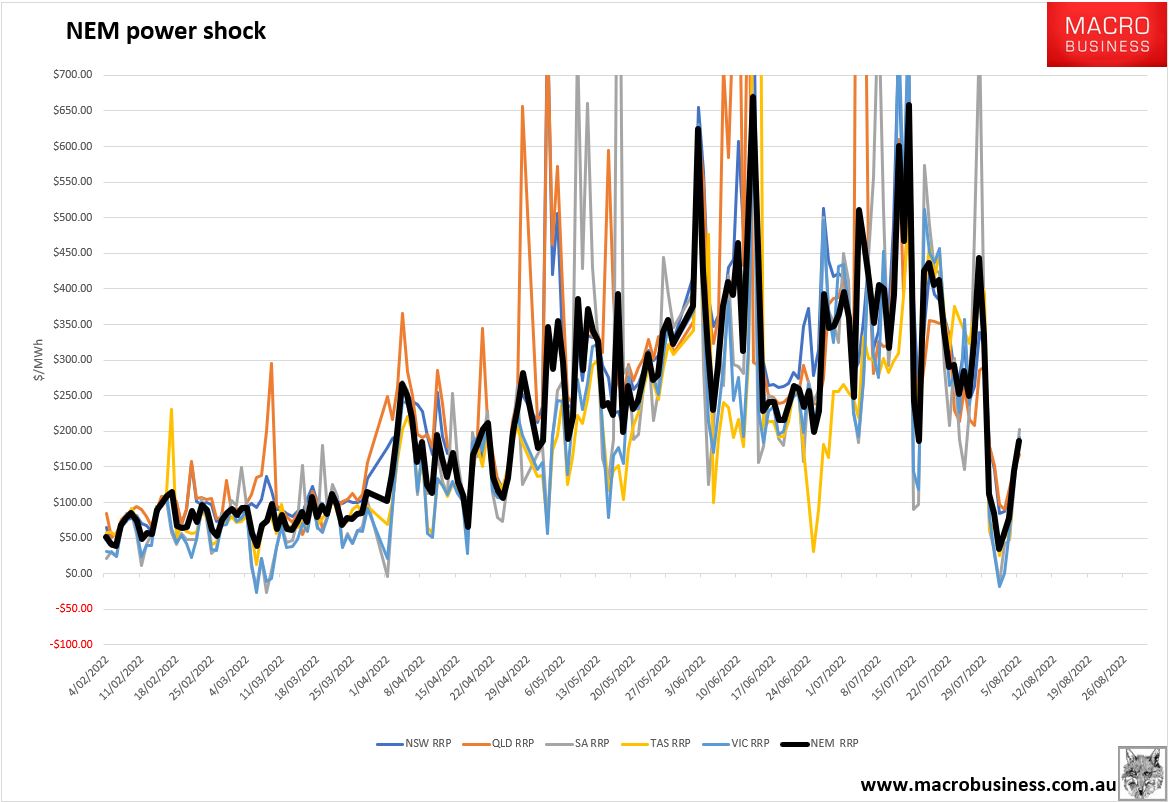

Wholesale electricity prices reached a peak in mid-June (Graph A.5). This led the Australian Energy Market Operator (AEMO), which oversees the NEM, to implement a price cap for a few days in some states. Subsequently, some generators withdrew from supplying electricity until directed to do so by AEMO, with liaison indicating that the $300/MWh price cap was below the cost of production for some generation sources. As a result, the NEM became difficult to operate and AEMO suspended the NEM between 15 and 24 June. Since then, the NEM has been operating as usual and wholesale electricity prices have remained elevated.

Graph A.5

Higher wholesale prices will lead to higher prices for households and businesses

Households’ electricity and gas prices are expected to increase significantly in the September quarter, following the recent increase in wholesale prices. However, the bulk of the effect of these higher prices on the CPI will be delayed until the December quarter because some state governments have introduced energy rebates.

Wholesale energy costs account for about one-third of households’ electricity and gas bills, as they directly affect retailers’ costs.[2] The pass-through from wholesale electricity prices to retail prices tends to be gradual, reflecting the fact that most retailers hedge at least some of their exposure to fluctuations in wholesale prices. In addition, the pass-through of these higher costs to the prices paid by customers is influenced by regulatory decisions about the default rate that customers are charged – commonly referred to as a default market offer (DMO) or standing offer – unless they shop around and get a market offer with a more competitive rate. The Australian Energy Regulator increased the default offers for electricity by 7–18 per cent in New South Wales, southeast Queensland and South Australia from 1 July 2022. The Victorian and Tasmanian regulators also announced a 5 per cent and 12 per cent increase, respectively, in their default offers from 1 July 2022. Around 10 per cent of residential customers across these regions are on default offers, with the remaining 90 per cent on market offers. Market offers have previously been priced at a significant discount to default offers; however, at least some of this discount has been eroded recently, with price increases for market offers in the east coast states and South Australia generally being larger than the increase in default offer prices. Meanwhile, retail electricity prices in Western Australia increased by 2½ per cent from 1 July 2022.

Contacts within the Bank’s liaison program generally expect further significant increases in retail electricity prices in 2023. This is largely because the recently announced regulated price increases for 2022 were decided before the latest run-up in wholesale prices and because wholesale prices are expected to remain elevated. Therefore, a further increase may be required to allow retailers to recover their costs.

Electricity and gas prices faced by businesses will also increase. Larger businesses are expected to face greater increases in electricity and gas bills over the next year than smaller businesses and households because wholesale prices make up a larger share of their energy costs (due to higher usage). However, most large businesses are on multi-year fixed-price contracts for electricity and gas, and therefore higher wholesale prices will be passed through more gradually as contracts reset. These expected price increases are likely to have a further indirect effect on inflation, to the extent that firms pass increases in energy costs onto their customers via higher prices.”

Advertisement

Not idly do the leaves of the RBA fall. The Bank needs and wants help with energy cartel inflation.

Albo can prevent and reverse all of this with the stroke of a pen. All he needs to do is install tough domestic reservation, or an export levy/super-profits tax benchmarked to pre-Ukraine prices to smash the gas and coal cartels, and real labor income will roar back to parity in the year ahead.

The Government needs to move fast. Every day that it hides in fear the gas cartel grows bolder and the price spikes trickle into more retail prices. Last week’s relief in the gas price is now fading with the east coast average spiking to $17Gj and NEM prices following like clockwork:

Advertisement

It is now abundantly clear that the RBA feels it will have no choice but to chase these price hikes higher even though it cannot affect them. That means it will crash other prices as an offset. Most notably asset prices and real incomes.

If the Albanese Government can’t act assertively on this then it will prove its economic ineptitude in the first few months of office.

Advertisement

Indeed, it will illustrate that it is neither “left” nor “Labor” nor “Australian” in any identifiable way.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.