Stock markets finished the trading week with vigour on Friday night with big gains on Wall Street as inflation expectations may have peaked with the latest US CPI print. The USD returned to form and gained some 0.5% against the major currencies with Euro in the main retracing back most of its post-CPI gains, while the Australian dollar still held on to its two month high above the 71 cent level despite falls in commodity prices. Bond markets saw 10 year Treasury yields pull back again, down to the 2.8% level while interest rate futures are steady with 120bps in rate rises still predicted by the end of 2022. Commodity prices were weaker due to the stronger USD with Brent crude oil down over 2% to pullback below the $100USD per barrel level while gold finally broke through the $1800USD per ounce level.

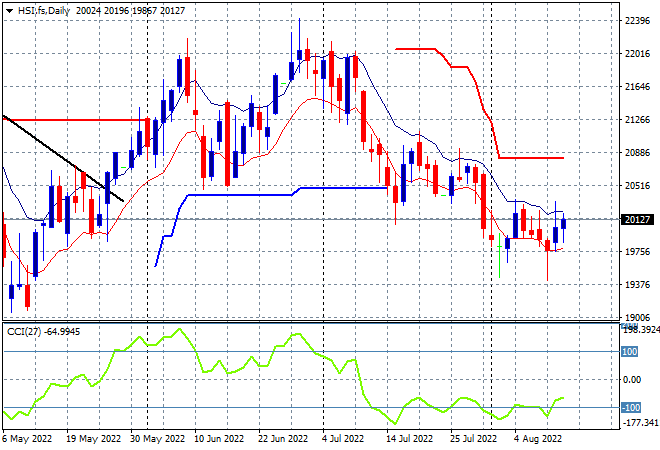

Looking at share markets in Asia from Friday’s session, where mainland Chinese share markets were down throughout the session with the Shanghai Composite eventually closing nearly 0.2% lower to 3275 points while the Hang Seng Index lifted slightly, closing up 0.4% at 20175 points. The daily chart is still showing considerable overhead resistance and daily momentum readings remaining negative as the moving average channel keeps trending down although there are signs of deceleration evident. The May lows could come under pressure soon if there is another break below the low moving average:

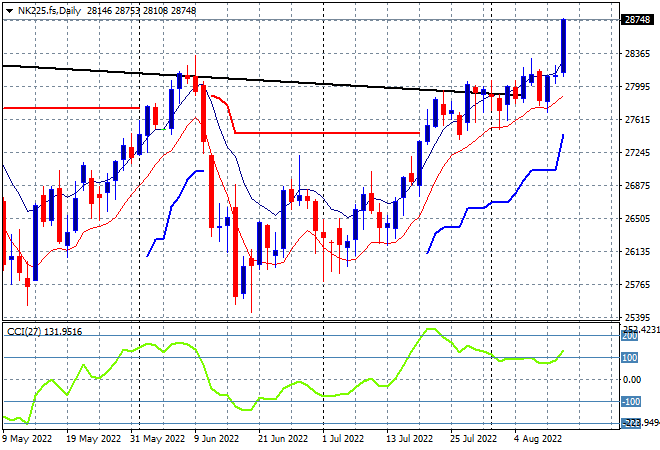

Japanese stock markets reopened from their holiday with the Nikkei 225 putting on more than 2.6% to 28546 points. The daily chart had been suggesting a breakout after finally clearing resistance at the previous highs at 28000 points with Friday’s effort pushing daily momentum up through the overbought level again. The overall monthly/weekly downtrend (sloping black line above) seems to be broken here after price action bunched up for so long. With very positive risk sentiment now, watch the 28000 point level to turn into support next: