Risk markets were contained overnight with both European and US stocks unable to gain traction post the US CPI print in the previous session. The USD remains slightly weak against the major currencies with Euro holding on to its recent gains while the Australian dollar is at a two month high above the 71 cent level due to higher commodity prices. Bond markets saw 10 year Treasury yields rise sharply, now back to the 2.9% level while interest rate futures are steady with 120bps in rate rises still predicted by the end of 2022. Commodity prices lifted with the weaker USD helping Brent crude nearly reach the $100USD per barrel level while gold continues to fail its way through the $1800USD per ounce level.

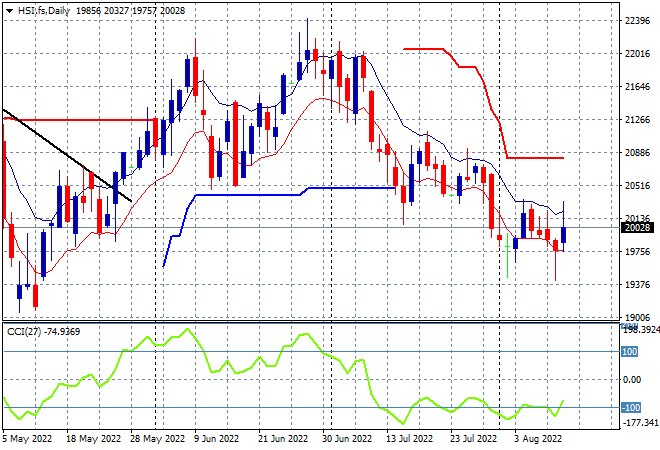

Looking at share markets in Asia from yesterday’s session, where mainland Chinese share markets are soaring higher with the Shanghai Composite up more than 1.6% to 3281 points while the Hang Seng Index has taken back most of its previous loss to close more than 2% higher at 20031 points. The daily chart is still showing considerable overhead resistance and daily momentum readings remaining negative as the moving average channel trends down despite these oscillations. The May lows could come under pressure soon if there is another break below the low moving average:

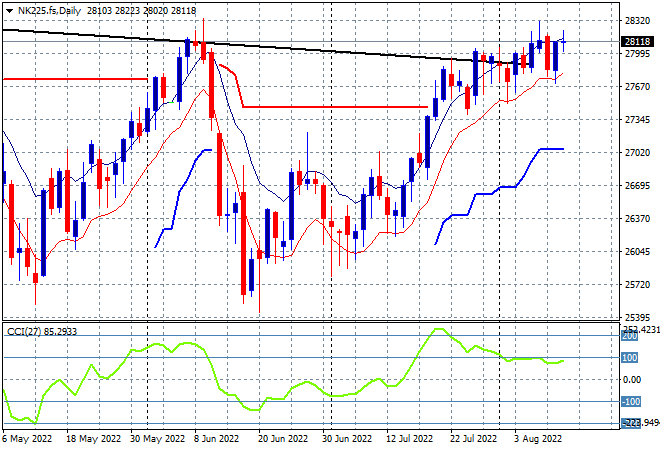

Japanese stock markets were closed for yet another holiday. The daily chart is still suggesting this pause could be turning into a breakout to finally clear resistance at the previous highs at 28000 points but price action continues to bunch up around this level. Daily momentum has continued to retrace from its overbought status with the overall monthly/weekly downtrend (sloping black line above) back in play. Watch the low moving average to act as support going forward if it can translate overnight positive risk sentiment into something sustainable: