Risk sentiment is in hesitation mode as traders await the next US CPI print and the fallout from the Fed as tech stocks also took a battering. The USD remains strong against most of the major currencies although Euro tried to break out of its current funk, the Australian dollar is looking to roll over below the 69 handle again. Bond markets saw some slight selloffs with 10 year Treasury yields pushed back up to the 2.8% level with more than 135bps in rate rises now predicted by the end of 2022. Commodity prices moderated as oil went nowhere with Brent crude still well below the $100USD per barrel level at a three month low, while gold lifted to almost push through the $1800USD per ounce level.

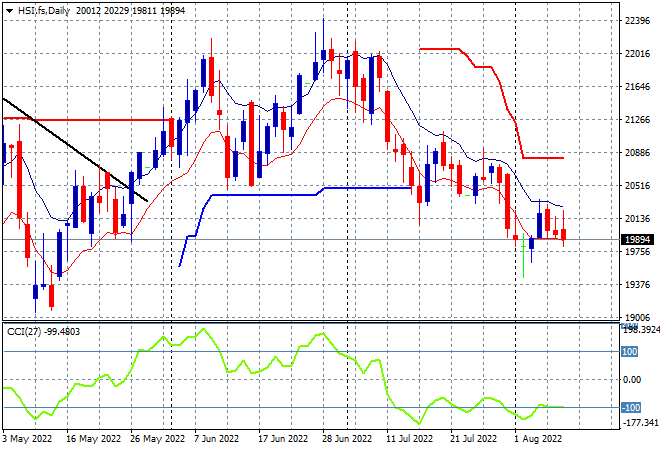

Looking at share markets in Asia from yesterday’s session, where mainland Chinese share markets were able to lift slightly into the close with the Shanghai Composite up 0.3% to 3247 points while the Hang Seng Index maintained a somewhat flat position, closing 0.2% lower at 20003 points. Sentiment continues to wane here with the daily chart still showing considerable overhead resistance and daily momentum readings remaining negative as the moving average channel trends down. It looks like the May lows will come under pressure soon so watch for a break below the low moving average:

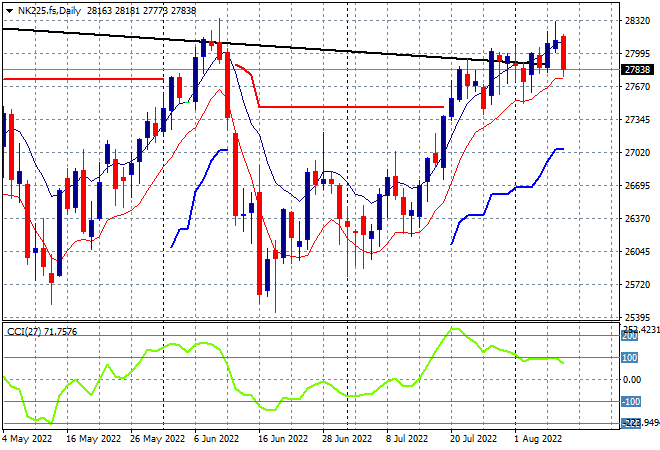

Japanese stock markets pulled back sharply however with the Nikkei 225 finishing down 0.8% to 27999 points. The daily chart was suggesting this pause could be turning into a breakout to finally clear resistance at the previous highs at 28000 points but that was put in its place yesterday with a bearish engulfing candle following the topping action of the previous session. Daily momentum has continued to retrace from its overbought status with the overall monthly/weekly downtrend (sloping black line above) back in play. Watch the low moving average to come under pressure next: