Wall Street was again hesitant overnight as traders continue to absorb the impact of quite strong US unemployment print from Friday night plus the latest Congress machinations around spending. The USD remains strong against most of the major currencies although the Australian dollar has picked up pace to try to get back to its pre-RBA rate rise position. Bond markets tightened slightly 10 year Treasury yields pushed down to the 2.7% level with more than 130bps in rate rises now predicted by the end of 2022. Commodities remain volatile as oil prices came back 2% or more but still at a three month low, while gold also lifted to almost get back to last week’s high around the $1775USD per ounce level.

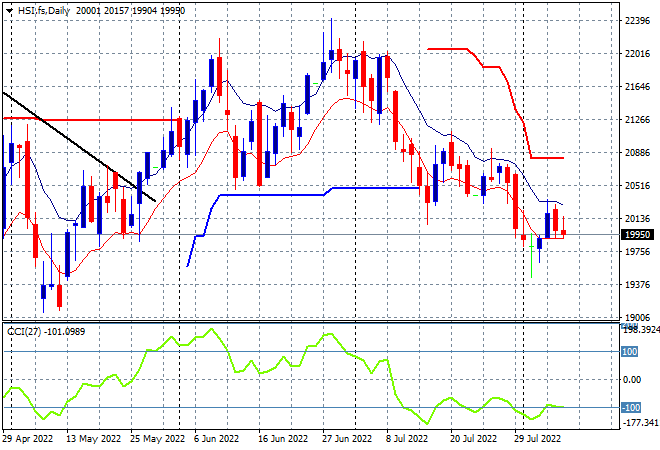

Looking at share markets in Asia from yesterday’s session, where mainland Chinese share markets gained some ground heading into the close with the Shanghai Composite up 0.2% to 3236 points while the Hang Seng Index fell down again, closing off more than 0.7% to 20045 points. Sentiment remains all over the place due to macro and geopolitical concerns with the daily chart still showing considerable overhead resistance and daily momentum readings quite negative as the moving average channel is still trending down. It looks like the May lows will come under pressure soon:

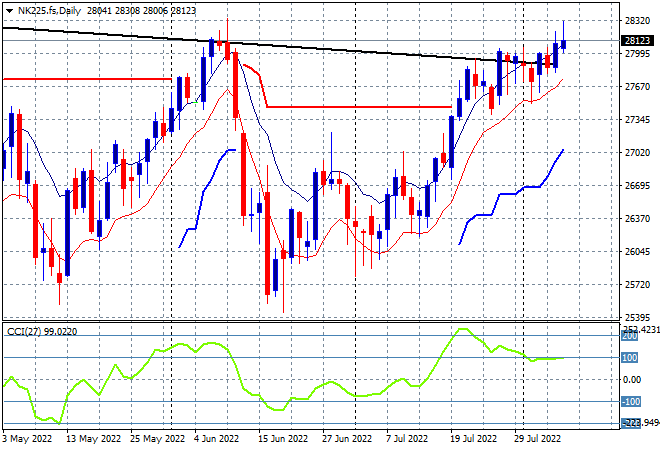

Japanese stock markets were treading water with only minor gains with the Nikkei 225 finishing up 0.2% to 28249 points. Futures on the daily chart are suggesting this pause could be turning into a breakout to finally clear resistance at the previous highs at 28000 points. Daily momentum has retraced from its overbought status and while price recently made a new weekly high, the overall monthly/weekly downtrend (sloping black line above) is still in play: