Wall Street was mixed on Friday night due to the quite strong US non-farm payrolls aka NFP aka unemployment print, with the USD regaining ground against all of the major currencies as the Fed has a clear path to more rate rises. The Australian dollar was put back in its place as the RBA can’t play this rate game. Bond markets sold off with of yields with 10 year Treasuries pushed back up to the 2.8% level with more than 125bps in rate rises now predicted by the end of 2022, with a near 70bps rise for next month. Commodities remain volatile as oil prices came back slightly but still at a three month low, while gold suffered a little as an undollar, but not as much as expected and still hold on to its new monthly high.

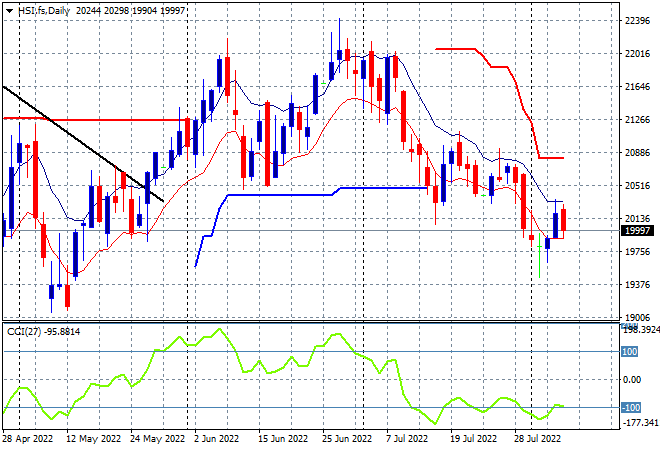

Looking at share markets in Asia from Friday’s session, where mainland Chinese share markets were basically treading water until a late surge saw the Shanghai Composite finish up 1% to 3227 points while the Hang Seng Index finished with a scratch session, closing 0.1% higher at 20201 points. Sentiment remains all over the place due to macro and geopolitical concerns with the daily chart still showing considerable overhead resistance and daily momentum readings quite negative. It looks like the May lows will come under pressure soon – but watch those long tails on the recent daily lows which maybe some support building:

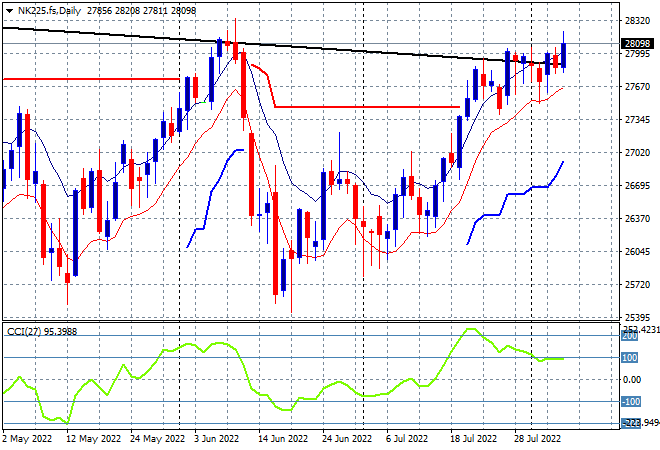

Japanese stock markets were the standout despite growing tensions over Taiwan, with the Nikkei 225 up 0.8% to 28175 points. Futures on the daily chart are suggesting this pause could be turning into a breakout to finally clear resistance at the previous highs at 28000 points. Daily momentum has retraced from its overbought status and while price recently made a new weekly high, the overall monthly/weekly downtrend (sloping black line above) is still in play: