Wall Street stalled overnight on some disappointing earnings while European markets continued their surge as the Bank of England was the latest to raise interest rates. Currency markets are still prepping for tonight’s US non-farm payrolls aka unemployment print, with the USD pulling back most of its recent gains particularly against Euro, although Pound Sterling didn’t move much on the rate rise. The Australian dollar is also still failing to climb back above the 70 level following its post-RBA rate rise walloping. Bond markets saw more tightening of yields with 10 year Treasuries pushed down to the 2.6% level with more than 100bps in rate rises still predicted by the end of 2022. Commodities remain volatile as oil prices lost nearly 3% to entrench its three month low, while gold rose to a new monthly high.

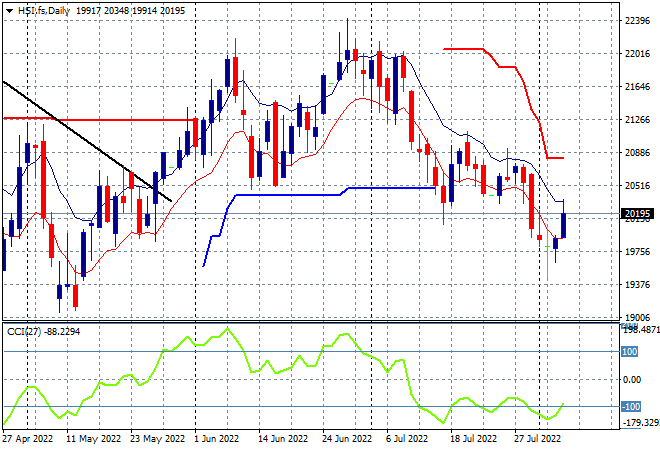

Looking at share markets in Asia from yesterday’s session, where mainland Chinese share markets had a good start to the session before giving up gains midway through with the Shanghai Composite now only up 0.8% to 3189 points while the Hang Seng Index is surging through the 20000 point barrier, up more than 2% to 20176 points. Sentiment remains all over the place due to macro and geopolitical concerns with the daily chart still showing considerable overhead resistance and daily momentum readings quite negative. It looks like the May lows will come under pressure soon – but watch those long tails on the recent daily lows which maybe some support building:

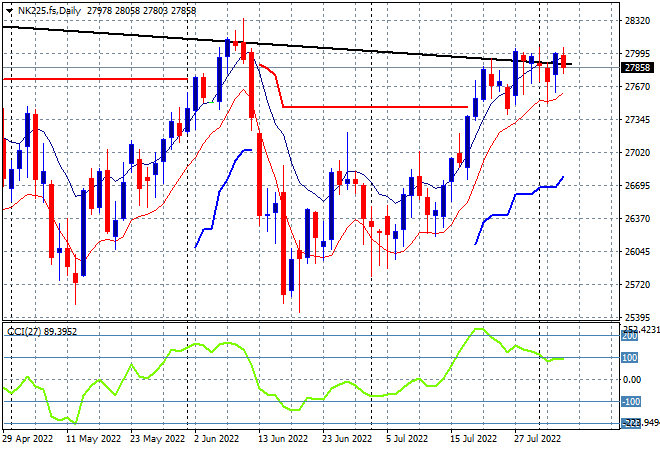

Japanese stock markets are coming back in similar fashion with a weaker Yen helping, with the Nikkei 225 up 0.6% to 27932 points. Futures on the daily chart are suggesting this pause could be turning into a breakout to finally clear resistance at the previous highs at 28000 points, but this hasn’t translated into actual price action yet. Daily momentum has retraced from its overbought status and while price recently made a new weekly high, the overall monthly/weekly downtrend (sloping black line above) is still in play: