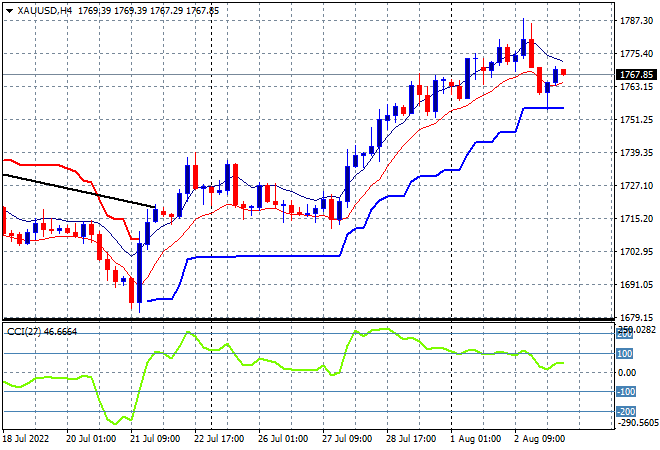

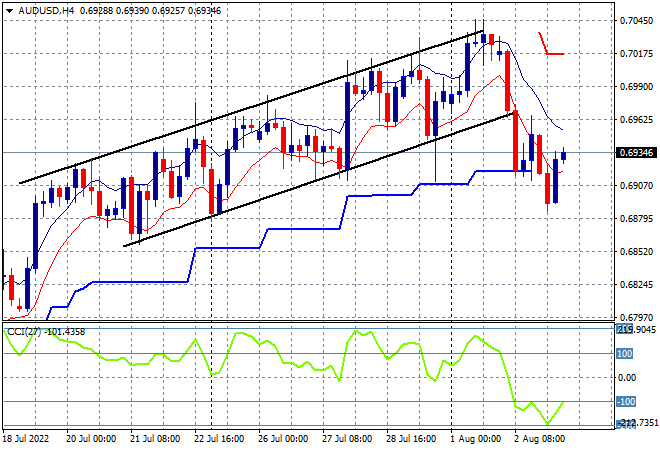

Asian stocks are having another very mixed session given the rising tensions around Taiwan and China and the somewhat volatile session on overnight markets due to more hawkish Fed talk. The USD is holding on to its overnight reversal gains with the Australian dollar having slumped post the latest rate rise by the RBA, while Yen is weaker. Meanwhile oil prices are slipping below key support levels, with Brent crude remaining below the $100USD per barrel level, while gold has been able to clawback some of its overnight losses, currently at the $1767USD per ounce level:

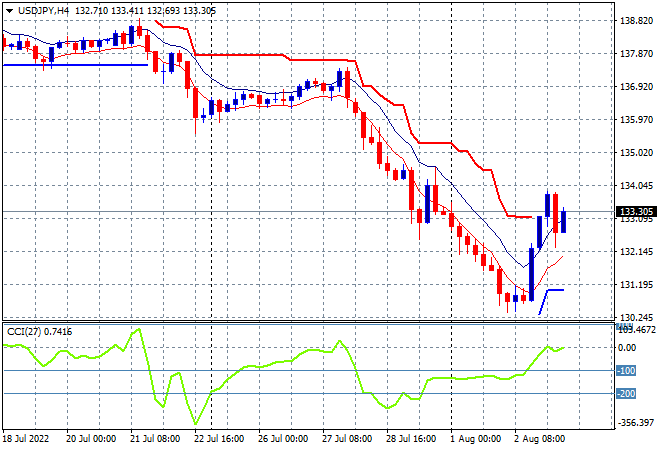

Mainland Chinese share markets were looking to hold on to scratch sessions despite increased tensions of Taiwan but are selling off now, with the Shanghai Composite down 0.7% to 3167 points while the Hang Seng Index is still above water yet well below the 20000 point barrier, up around 0.5% to 19819 points. Japanese stock markets are coming back in similar fashion with a weaker Yen helping, with the Nikkei 225 up 0.5% to 27741 points as the USDJPY pair maintains it overnight bounce at the 133 level:

Australian stocks pulled back slightly in response to overnight volatility with the ASX200 closing 0.3% lower as it continues to reject the 7000 point level, closing at 6975 points. The Australian dollar was able to clawback some of its overnight losses but remains on the ropes here after a strong reversal post the RBA rate rise:

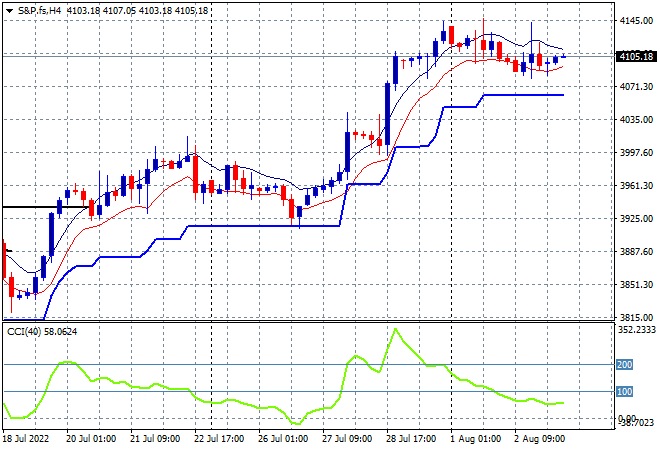

Eurostoxx and US futures are holding on to their start of week positions following the mild falls overnight with the S&P500 four hourly futures chart showing price action pausing here above the 4100 point level as the relief rally takes a breather:

The economic calendar ramps up with the latest UK and US Services PMI surveys.