The RBA has already overcooked the tightening cycle.

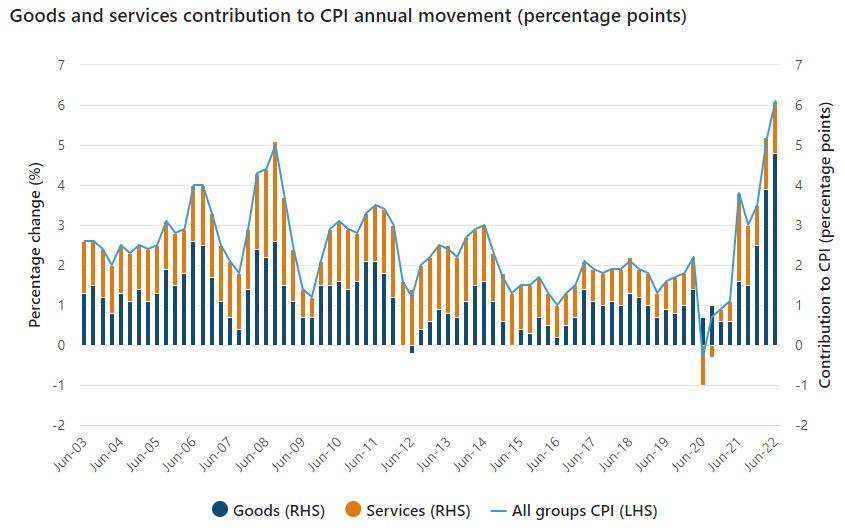

First of all, the inflation we’ve had so far is mostly in goods and much of that is imported:

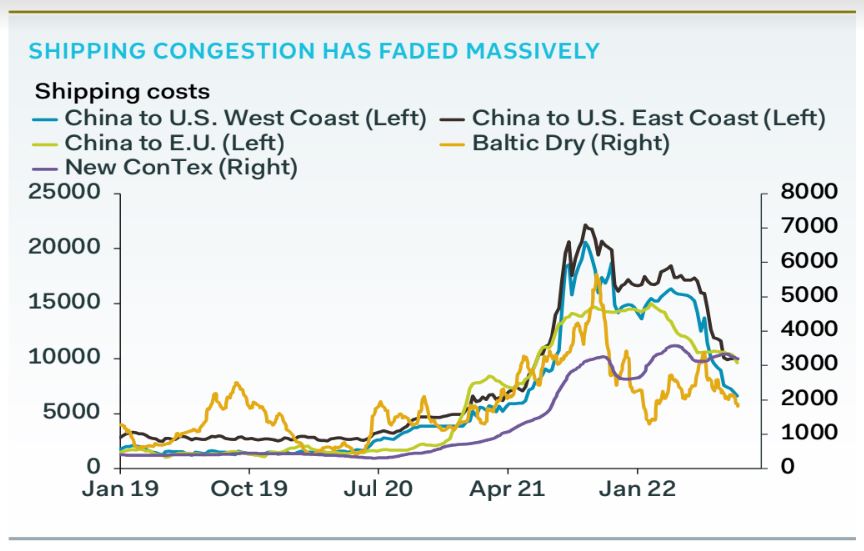

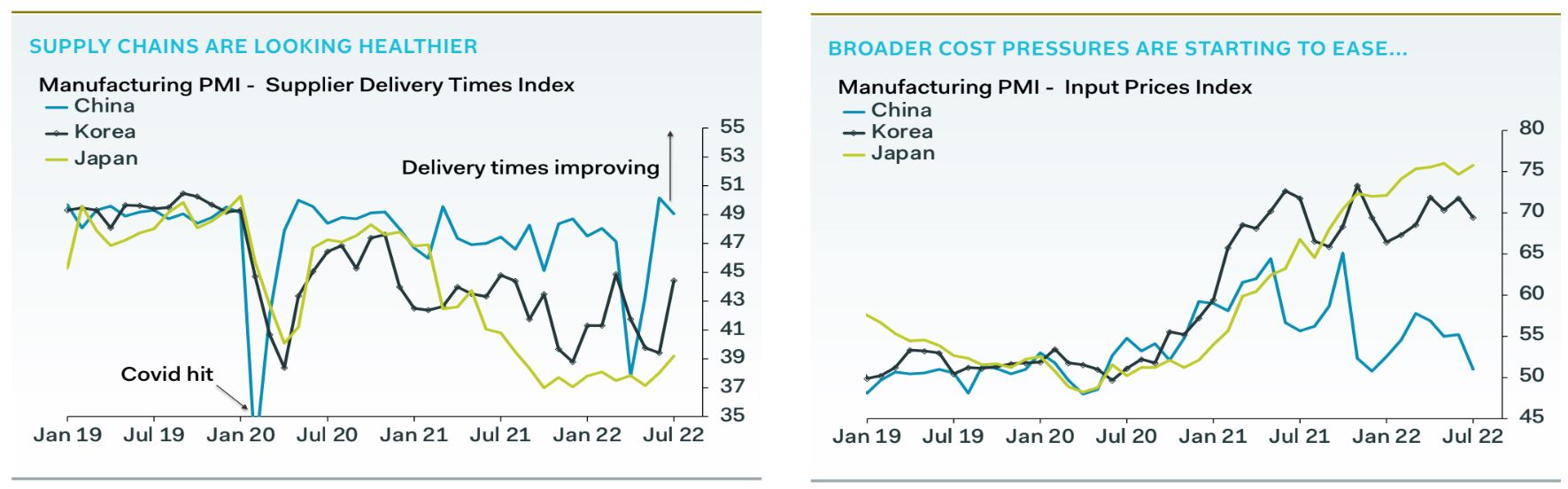

The supply chain and commodity price inputs that drive up these prices are already deflating internationally. Falling prices will arrive in due course:

Those goods that are made in Australia, building materials most obviously, are also going to deflate as the housing construction bust intensifies:

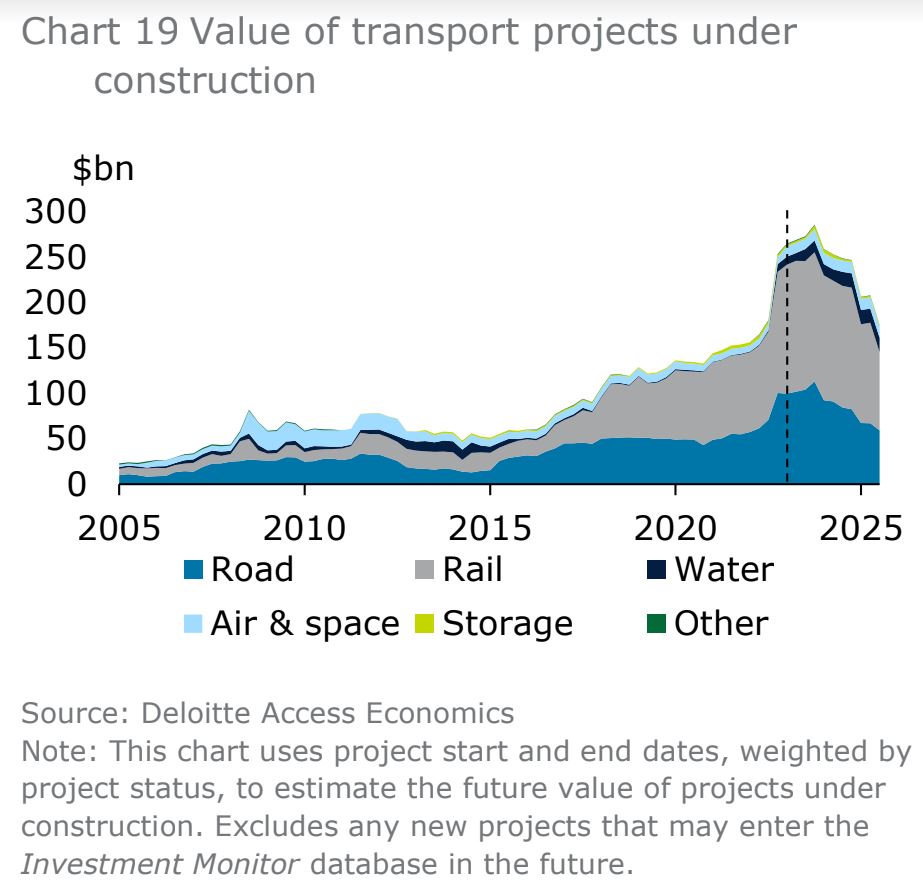

The infrastructure boom is also about to top out

:

Moreover, the second wave of inflation, coming from the evil gas cartel, is also over so long Labor does what it should with tougher domestic reservation:

It must also be remembered that the huge terms of trade boost is not what it seems and is also crashing. The gas component is not an export for the east coast. It is an import of high energy prices and drained income with no taxes. Iron ore and coking coal are deflating with China’s structural property adjustment. Softs are deflating. Thermal coal is crazy but there’s no investment coming for that:

Other hot inflation reads in food and transport will also fall with energy, including oil for transport which is also now tumbling:

As we know, consumer confidence has been annihilated. Consumption will fall with house prices from here. Business investment will follow:

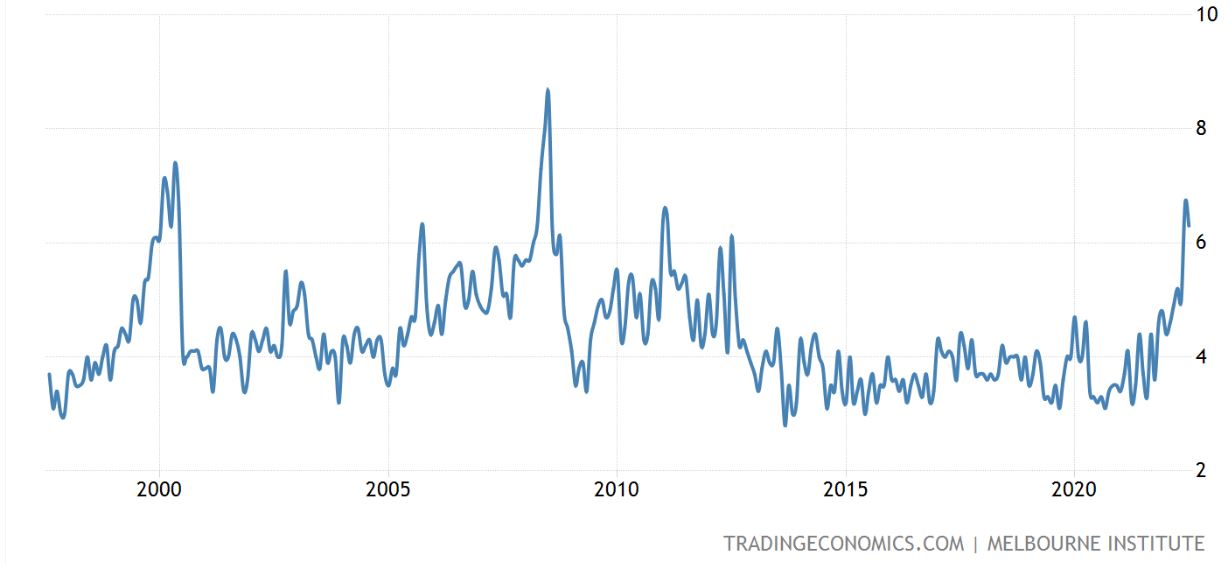

Inflation expectations have only returned to periods where Aussies did enjoy some decent wage growth. The RBA needs to keep this intact, not sink it again as it stupidly did post-2010:

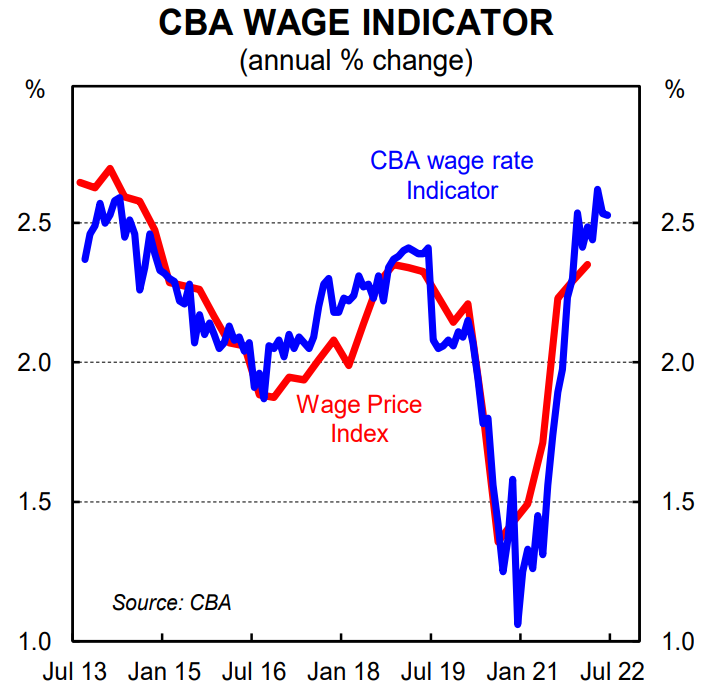

Sadly, there is no wage pressure to worry about. What there is has been exaggerated by vested interests to hoodwink the gormless RBA. The CBA’s wage tracker, which leads the ABS’ labour price index and is derived from CBA accounts, shows that wage growth remains sluggish, growing only by around 2.5% in the year to July:

Even NAB’s economics team has trashed its own business survey by doing a similar analysis using its own bank accounts, and also shows that wage growth was only around 2.5% in the June quarter:

The NAB is getting real-time data on whether its customers’ wages are going up, down or sideways…

It’s the first time the bank has used its customers’ data in this way. So, it began with the deposit account data of roughly a million customers, and its computer models whittled that down to 250,000 customers that has straightforward, measurable wage or income deposits.

Its results are remarkably consistent with the ABS’s results on wage growth.

That is, NAB’s analysis has found wage growth increased 2.5 per cent in the three months to June — up 0.1 per cent on the ABS’s measure for the March quarter. In other words, wage growth, it reckons, is barely budging.

This is contradictory to what the Reserve Bank is reporting.

The Albanese Government is also determined to crush wages with restored mass immigration pronto. The leading edge of this has begun as a deluge of cheap foreign labour lands in the form of international students.

Finally, the RBA faces a half trillion fixed-rate mortgage reset for the next three years. This embedded tightening will smash house prices regardless of what else happens now.

The Lunatic RBA said at its last meeting it is turning data-dependent. The data is warning that it has already overcooked the tightening.