Bill Evans of Westpac cheering on the destruction of his own bank! Consumption is not going to hold up for very long and business investment will be next. Pass the popcorn.

—————————————————————————————–

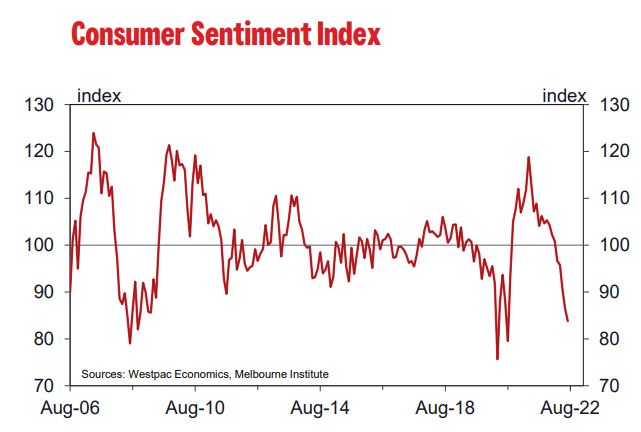

The Westpac Melbourne Institute of Consumer Sentiment Index fell by 3% from 83.8 in July to 81.2 in August.

This reading is on a par with the lows of the Covid and Global Financial Crisis although still well above the lows during the late 80/s/ early 90’s recession.

Since the recent peak in November 2021 the Index has fallen every month for a cumulative decrease of 22.9%.

Individual movements in the sub-indexes over that period are: “Finances relative to a year ago” (-18%);” Finances over the next 12 months” (-19%);” the economy over the next five years” (-18%);” the economy over the next 12 months” (-31%) and “whether now is a good time to buy a major household item” (-27%).

Our experience is that the 12month economic outlook has been the most volatile of the sub- indexes. A strong message from the collapse in the Index over the last nine months has been the negative attitude to major household purchases where confidence has fallen almost as fast as the 12month economic outlook.

It seems likely that inflation, which we still see as the major negative for confidence over this period has been weighing particularly heavily on the attractiveness of consumer durables.

For example, the recent June quarter inflation report showed a 7% (8.3% for the year) quarterly rise in the price of furniture and a 3.3% (5.7% for the year) quarterly increase in the cost of major household appliances. These increases were mainly due to transport and material costs, exacerbated by shortages.

It is ominous that the pace of these price increases has been increasing rapidly.

Interest rates continue to weigh on Confidence. With the Reserve Bank delivering yet another 0.5% rate increase last week the proportion of respondents expecting rates to rise by 1% or more over the next 12 months did fall from 72.8% in July to 57.6%.

Despite the higher starting point (1.85%) there is still a majority of respondents expecting rates to increase by at least 1%. We concur. We expect the cash rate to rise by a further 150 basis points by February next year.

Respondents holding a mortgage were particularly unnerved by the rate rise. Their confidence fell by 8.9% compared to modest moves from tenants (0.2%) and those owners who do not have a mortgage (-2.1%).

The major movements in the sub – indexes in the month were “12month economic outlook” (-8%); and “time to buy a major household item” (-8.4%).

Other components – “household finances relative to a year ago” (0.1%); “12month outlook for household finances” (+2.3%); and “5year economic outlook” (-1.0%) were relatively steady.

Confidence in the labour market continues to print on the upside. The Westpac Melbourne Institute Index of

Unemployment Expectations fell by 5.8%. (a lower read indicates a lower share of respondents who expect the unemployment rate to rise). Since the July Sentiment survey the unemployment rate was reported by the Australian Bureau of Statistics to have fallen from 3.9% to 3.5%.

A vibrant jobs market along with solid household balance= sheets are important explanations for the current resilient household spending despite deteriorating confidence.

Although overall consumer spending remains buoyant the housing market continues to deteriorate.

The Index “Time to buy a Dwelling” fell 2.3% from 80.1 to 78.2.

The Index is 41% below its recent peak in November 2020.

It has been steady since March 2022. We believe this Index responds to affordability as well as overall confidence in the market. As prices appeared to be peaking in the major markets in the second quarter of 2022 so prospects of improving affordability may have started to take hold.

Although this Index is likely to have bottomed out signs of a sustained improvement are unlikely while overall confidence in the housing market continues to deteriorate.

The Westpac Melbourne Institute Index of House Price Expectations is tumbling.

It fell by 7.5% from 104.9 in July to 97.1 in August.

It is now down by 41% from its recent peak in April 2021.

Pessimists now outnumber optimists.

The 17.7% fall in Victoria from 99.0 to 81.6 is particularly confronting.

Surprisingly the fall in NSW was only 2.3% from 97.3 to 95.1 but is now signalling that the pessimists are clearly in the ascendency.

Queenslanders are finally facing a much more subdued outlook.

The Queensland Index fell 10.0% from 115.18 in July to 103.62 in August.

The pessimists look likely to overtake the optimists in Queensland in the very near future.

The Reserve Bank Board next meets on September 6. We expect the Board will decide to raise the cash rate by a further 50 basis points to 2.35%.

That move would leave the cash rate in the “neutral range” as defined by both the Governor and the Deputy Governor in recent speeches.

It is sensible policy to move the cash rate quickly into that range given the extremely tight labour market and booming inflation.

Once in that neutral range it would be prudent to scale back the increases to 25 basis points per meeting as policy settings move further into the contractionary zone.

The Board will be monitoring the impact of the rate increases on the economy, particularly household spending, inflation, and wages growth.

Although our survey continues to highlight the parlous state of confidence and a rapidly deteriorating housing market household spending seems set to maintain momentum into the December quarter.

We expect that the Board will respond, after September, by adopting a steady 25 basis points per month policy into the new year with the last increase expected in February 2023.

It is critical that the Board signal to firms that it is committed to a very significant slowdown in demand in 2023 persuading them that demand in 2023 will not be strong enough to support any extension of the price increases that we are likely to continue to see for most of the remainder of 2022.