Pantheon kicks us off with an analysis of Chinese July data:

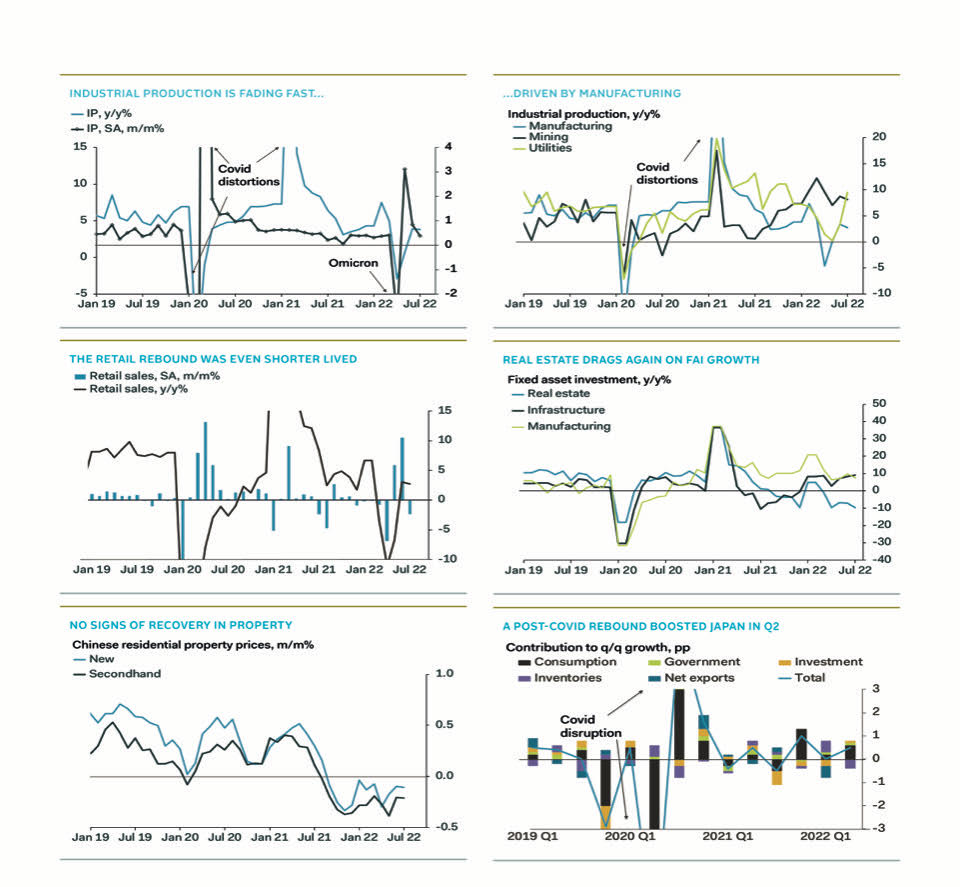

- China: Industrial production growth slowed to 3.8% y/y in July, from 3.9% in June. Consensus was 4.3%.

- China: Retail sales growth slowed to 2.7% y/y in July, from 3.1% in June. Consensus was 4.9%.

- China: FAI growth fell to 5.7% ytd y/y in July, from 6.1% in June. Consensus was 6.2%.

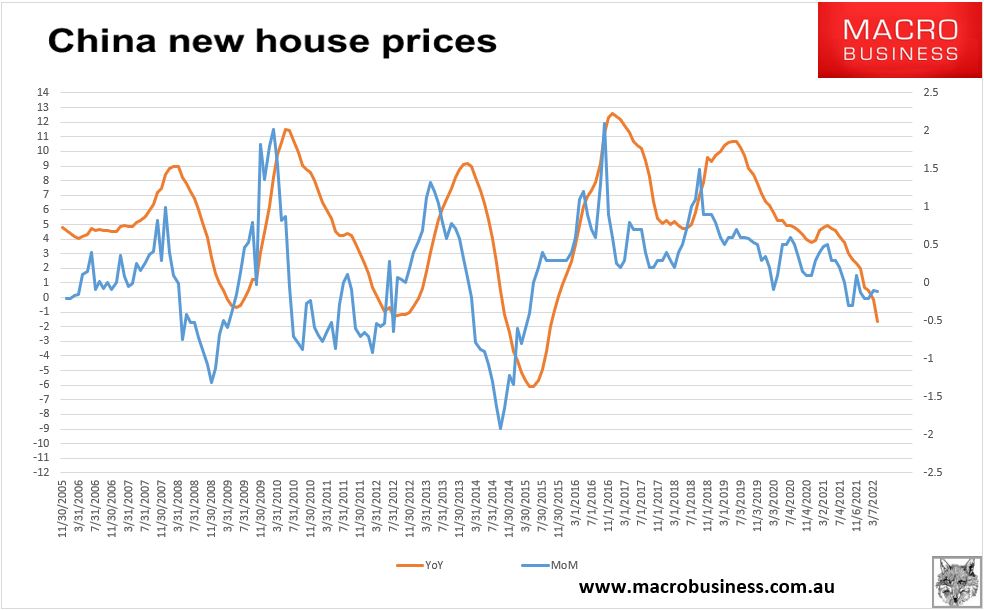

- China: New home prices fell 0.11% m/m in July, down from -0.10% in June. Consensus was 0.10%.

- China: The PBoC cut the 1-year MLF rate to 2.75%, from 2.85%. Consensus was 2.85%.

Manufacturing struggles despite subsidies

Chinese factory productions decelerated sharply. Output rose just 0.38% m/m, on the official seasonally adjusted measure, down from 0.84% in June, and 3.1% in May, as the boost from reopening fades. The y/y slowdown was led by manufacturing, which rose just 2.7% y/y in July, from 3.4% in June. Growth in mining output was also slower, at 8.1% y/y, from 8.7%, but utilities output jumped, growing 9.5% y/y, from 3.3%, largely due to electricity, which grew 10.4% from 3.2%. This likely reflects stronger than usual demand for energy amidst a heatwave, without which Chinese industrial production would have been even worse.Other isolated bright spots were autos, accelerating both in value and volume terms – propped up by government subsidy and tax cuts, for now – and extraction of petroleum and natural gas, driven by the latter. No other industry reported an acceleration in y/y output by value added. Volumes data revealed some impact from infrastructure spending, with improvements in caustic soda and cement production, though steel and iron output fell deeper into decline.Pressure continues to build on the private sector, where IP growth halved to 1.5% y/y in July, from 3%, even as SOE output climbed 5.4%, from 3.1%, reflecting the split of ownership in manufacturing and heavier industry and utilities.The slowdown in Chinese industrial production supports the narrative that stronger performances in May and June were primarily the result of a reopening rebound, and that with order backlogs now cleared, China’s factories will increasingly run idle once more.An even bigger miss for retail salesWe were taken particularly by surprise at the weakness of retail sales, where we had thought China should eke out one more month of modest monthly growth given the support for some big ticket purchases. Instead, however, retail sales fell 2.4% m/m, seasonally adjusted, from growth of 10.5% in June. Unadjusted, the drop was even larger, at -7.4%, from 15.5%. A renewed surge of Covid cases and tightening of zero-Covid restrictions likely played a part, but we think weak underlying demand is the main problem. Catering sales – which should struggle most if zero-covid is the main driver – rose 0.3% m/m, seasonally adjusted, in July, from 10.2% growth in June.Car subsidies remain in place, but it looks like activity here was hugely front loaded. Auto sales fell 2.8% m/m seasonally adjusted in July, after growing 19.7% in June, and 11.8% in May. Indeed, outside of catering, everything slowed in July, on a m/m basis, in many cases entering outright decline. Domestic demand is doing terribly, and continues to receive little-to-no support from policymakers. Retail sales will slow further in AugustReal estate still a killer for FAIThe main drag on FAI growth in July once again came from real estate, which more than offset the improvement in infrastructure. Manufacturing also took a hit in July. We estimate that while infrastructure investment rose 9.1% y/y, from 8.2% in June, real estate FAI shrank 9.5%, down from a 7.1% fall, and manufacturing FAI growth slowed to 7.5%, from 9.9%. As with the credit data earlier in the month, the state sector is increasingly the only support of investment. Stimulus is clearly coming through, but it’s not enough. Combined infrastructure and real estate investment – a proxy for construction-centric spending – fell 1.2% y/y in July, down from -0.1% in June.The ongoing decline in property prices, where secondhand home prices also fell 0.21% in July, unchanged from June, makes it clear that we should not expect real estate to return as a source of growth any time soon, and no policy changes appear to be on the horizon that might turn this around. Manufacturing investment, meanwhile, requires manufacturing profits. Slowing industrial value added growth, discussed above, alongside weakening domestic and global demand, do not make for an encouraging backdrop. We expect the role of infrastructure investment to become more dominant – but still insufficient – in the coming months.Monetary easing won’t do anythingThe PBoC cut the MLF rate by 10 bps today, which we can only imagine was because they felt like they had to be seen to do something, rather than because they think it will have much effect. At the same time, they injected only RMB 400B in MLF funds, with RMB 600B expiring tomorrow; in effect, a net withdrawal. As the credit data last week showed, availability of funds is not the problem, loan demand is. Equally, the price of credit is unlikely to be the deciding factor, particularly with interbank rates so low. We expect the PBoC to face renewed pressure from the MoF and others to provide more support, but liquidity is not the answer.

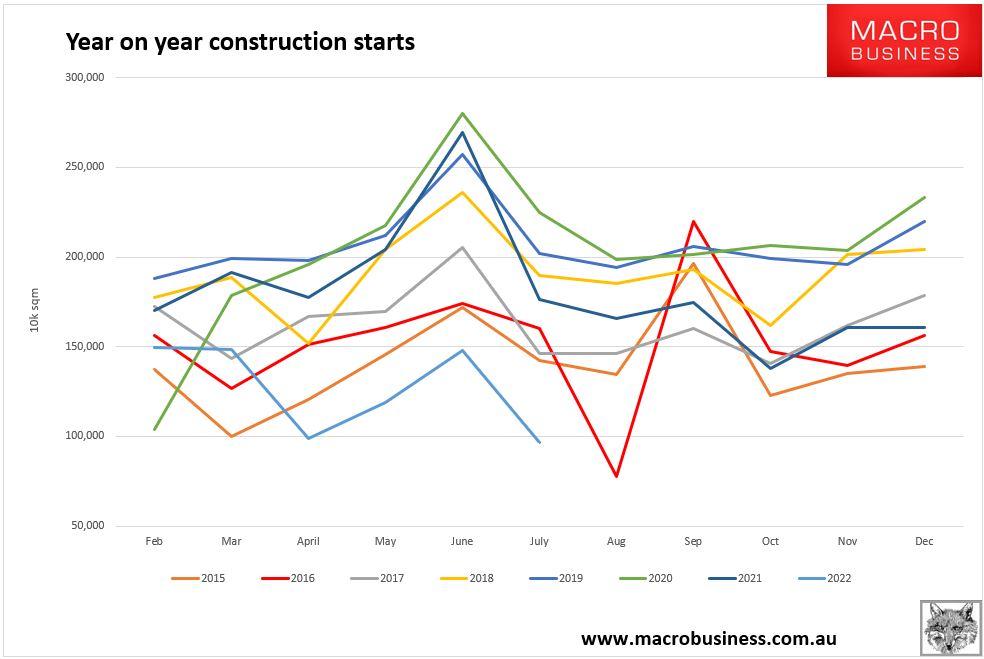

Let’s dig into the more commodity-specific data. Real estate is in a terrible state with floor area starts down 36% and the leading indicator of land sales down by 48%:

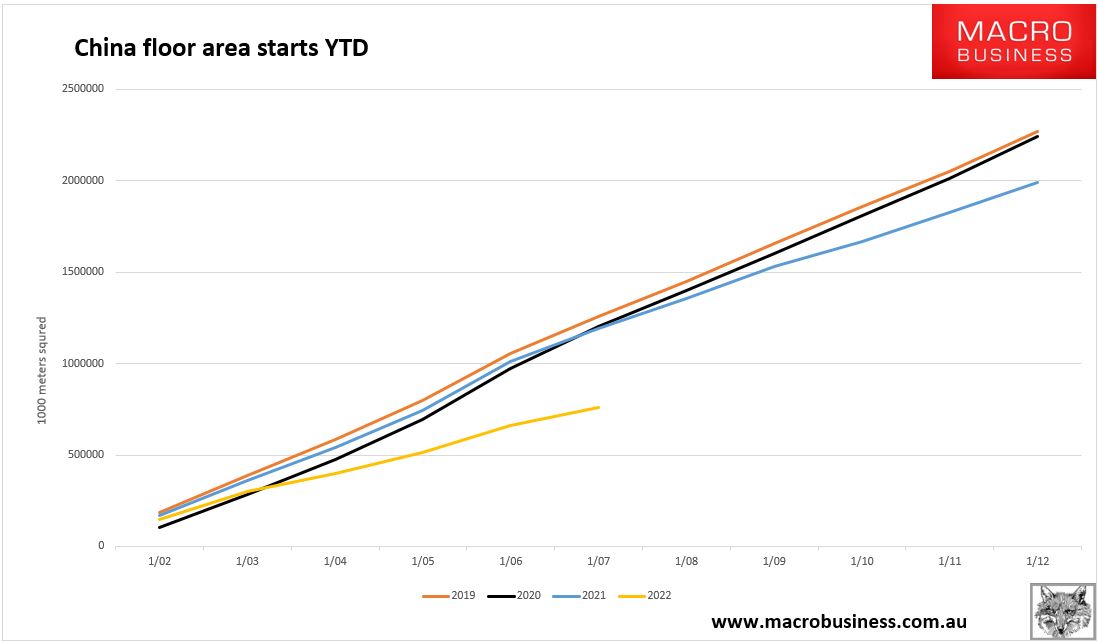

Year-to-date starts are…well…see for yourself:

Rolling annual starts have much further to fall based on current sales volumes:

And there is no reason to think it will change as prices for new apartments fall as well:

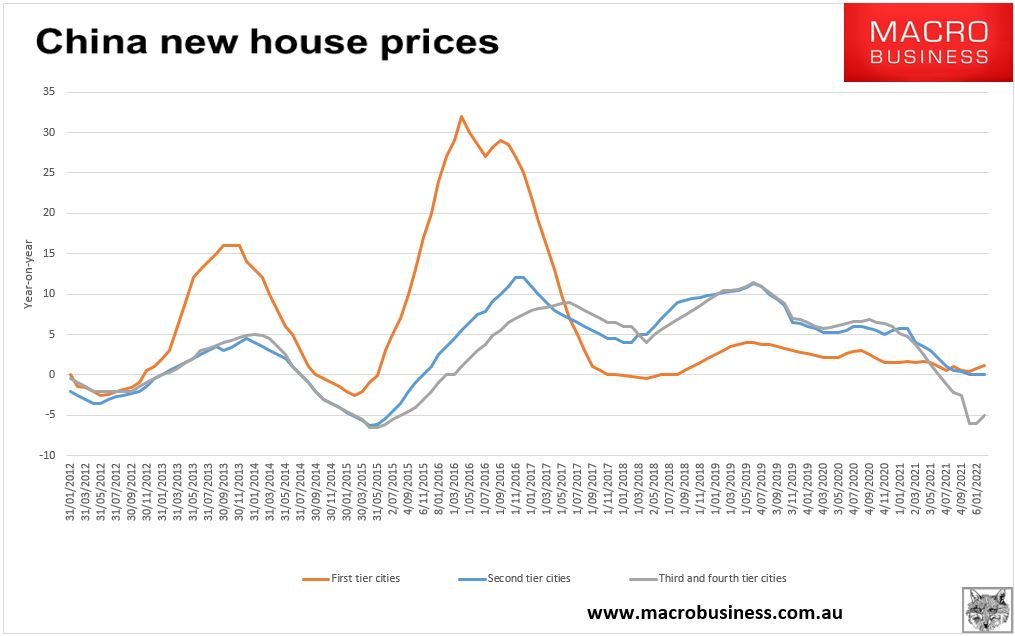

Top tier cities are OK but the vast majority of construction is in the lower tiers and they are not well:

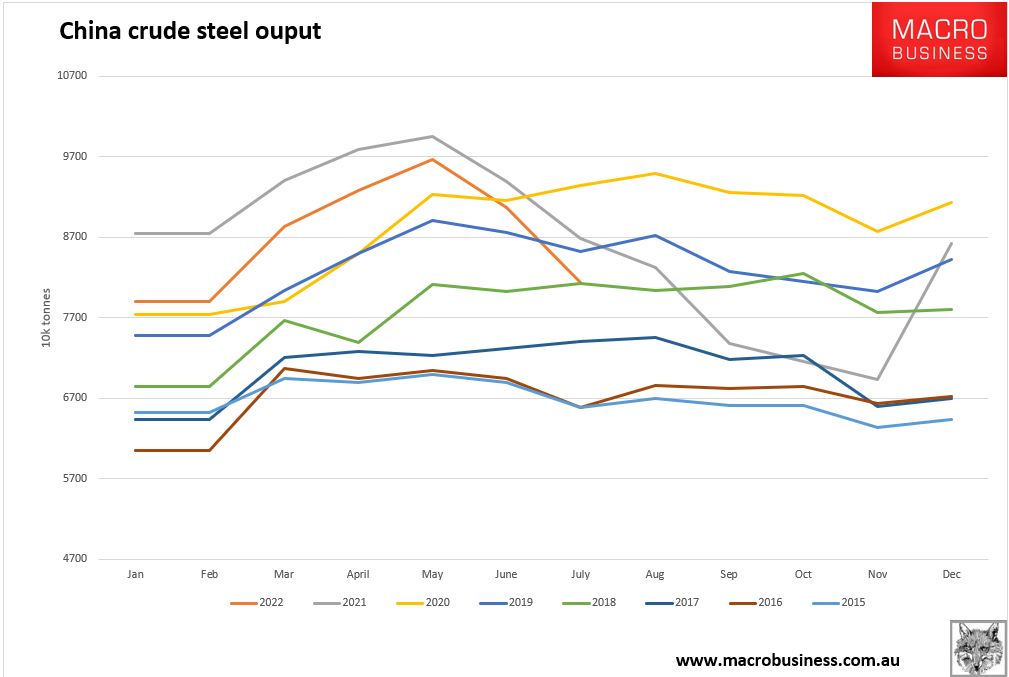

Crude steel output tanked the same as last year but worse:

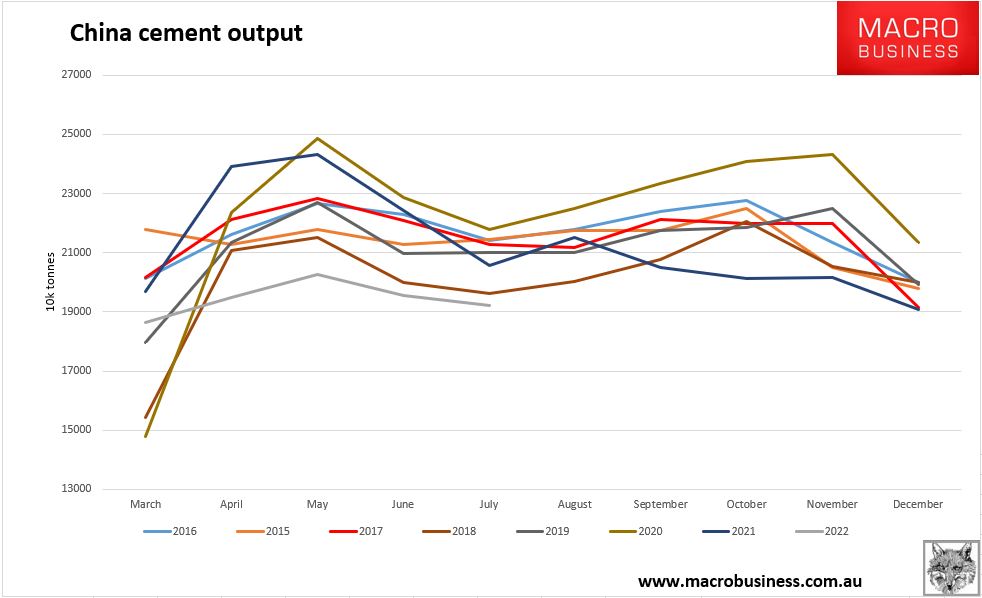

Cement output shows how inadequate is infrastructure stimulus:

China has gone ex-growth before our very eyes.