You don’t say. For me, this is still a bear market rally owing to the nasty cocktail of sky-high inventories, a tightening Fed, and outright recessions in Europe and China. BofA.

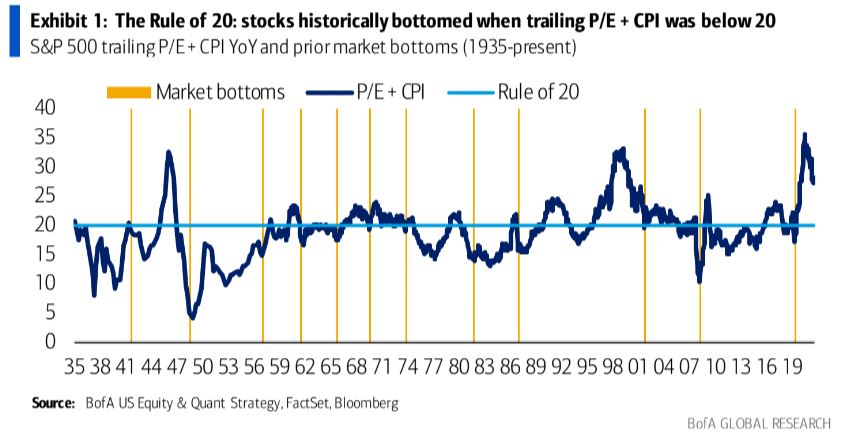

P/E should be 11 (it’s 20) or CPI should be 0% (it’s 8.5%)

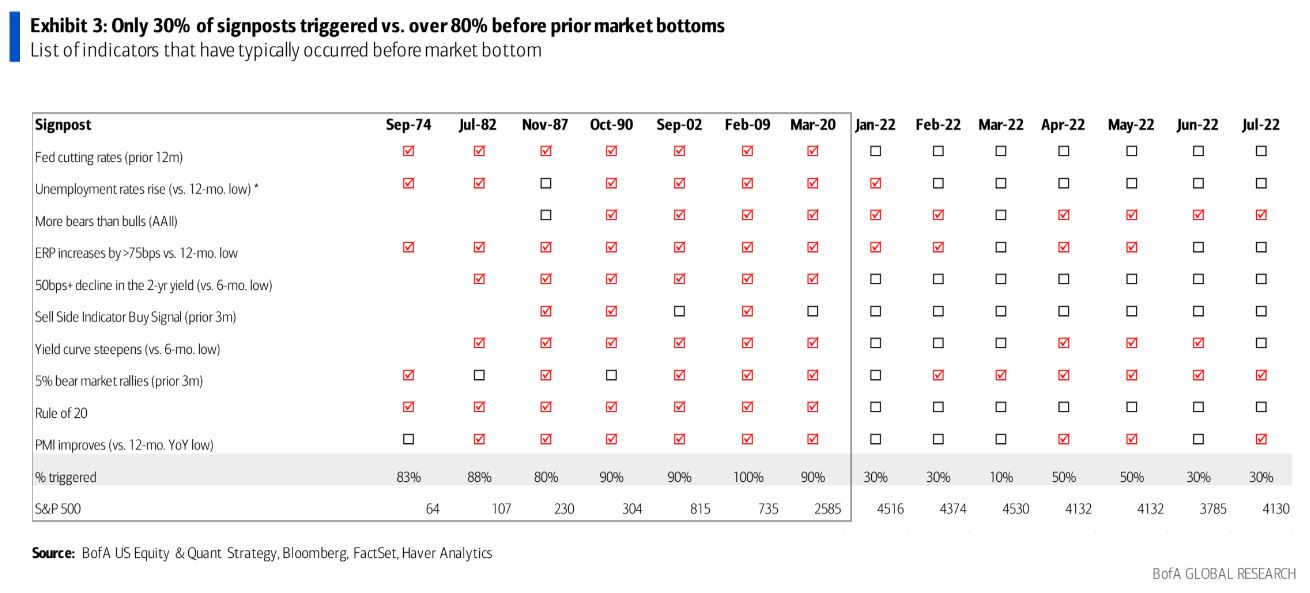

Only 30% of our bull market signposts (things that happen before a market bottom) have been triggered vs. 80%+ in prior market bottoms, suggesting that another pullback is likely (Exhibit 3). One signpost with a perfect track record is theRule of 20,i.e.,the sum of CPI y/y + trailing P/E has been lower than 20 when the market bottomed (Exhibit 1). Outside of inflation falling to 0%, or the S&P 500 falling to 2500, an earnings surprise of 50% would be required to satisfy the Rule of 20, while consensus is forecasting an aggressive and we think unachievable 8% growth rate in 2023 already.

Only 20% chance of recession now priced in

Stocks are still not inexpensive despite the bear market. In fact, they are more expensive after the S&P 500’s 17% rally from its June low, driven by a drop in the cost of equity (real rates + ERP). Our analysis of the ERP indicates a 20% likelihood of a recession is now priced in vs. 36% in June (Exhibit 2). In March, stocks priced in a 75% probability of recession. Even on EnterpriseValue to Sales, where sales should be elevated by the tailwind of 9% CPI, the market multiple is excessively elevated (+40%) relative to history–possibly because real sales growth ex-Energy is essentially flat.

More charts from The Market Ear.

Do you agree?

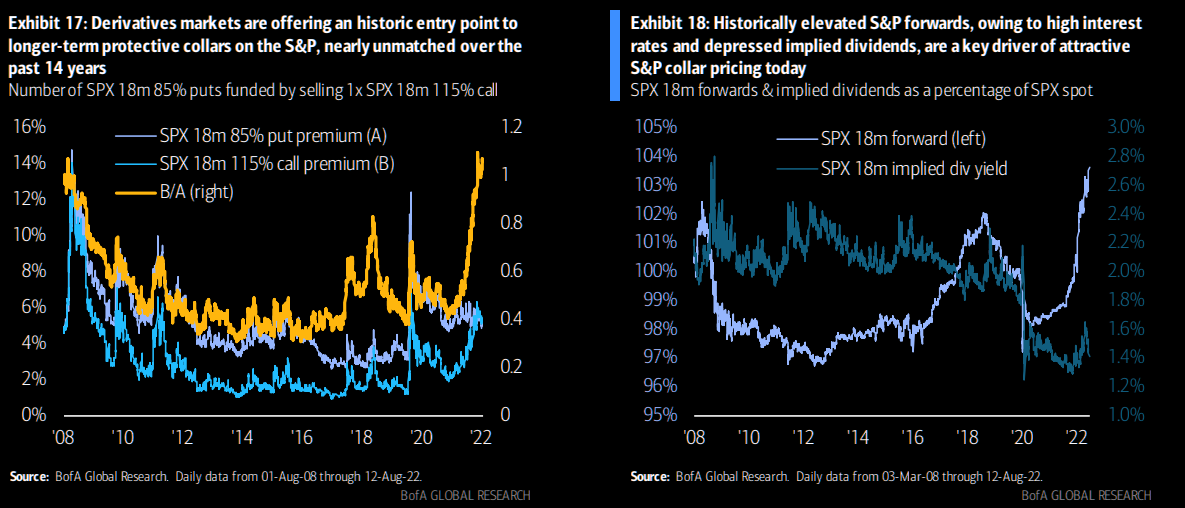

BofA’s derivatives research is basically asking if this is a rational rally or if you are being “sucked in” by momentum. They write: “…if you agree with what rising equities imply: 1) Rates & inflation matter less for equities than ever before; 2) Fighting the Fed now works; 3) Rates markets are clairvoyant, despite record economic uncertainty; 4) Even though QE inflated assets, QT won’t deflate them; and 5) Global geopolitical risks don’t present a material threat”. The team recommends low cost equity hedges and they like to buy a SPX Dec 23 3825-4800 collar (you buy the put and sell the call).

The collar offers a good longer term hedge for various scenarios and levels are very attractive due to high rates resulting in elevated forwards and low implied dividends.

Source: BofA

Recall the 2008 “analogy”?

Not perfect but still “hanging in” there.

Source: Refinitiv

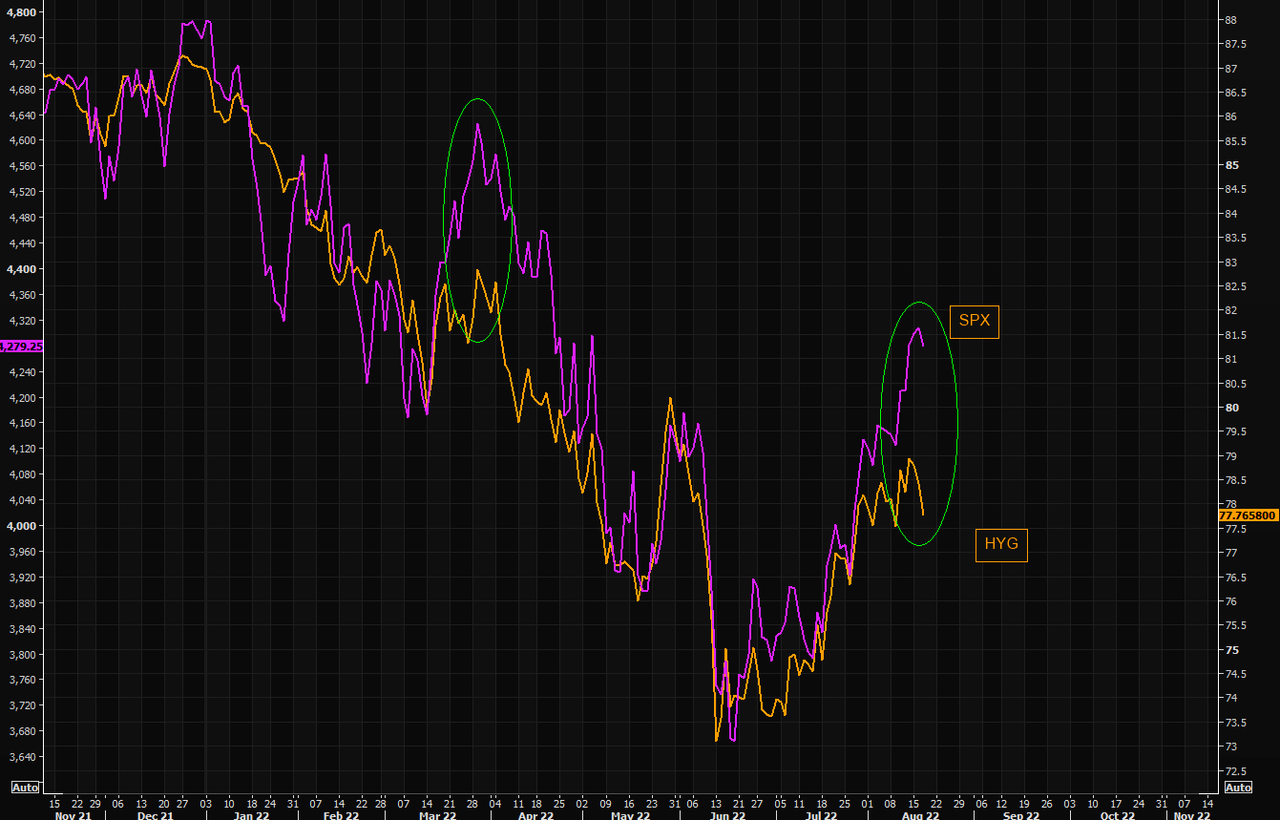

High yield “aggressively” not buying this

The HYG “roll over” is starting to look rather aggressive. Will SPX follow (again)?

Source: Refinitiv

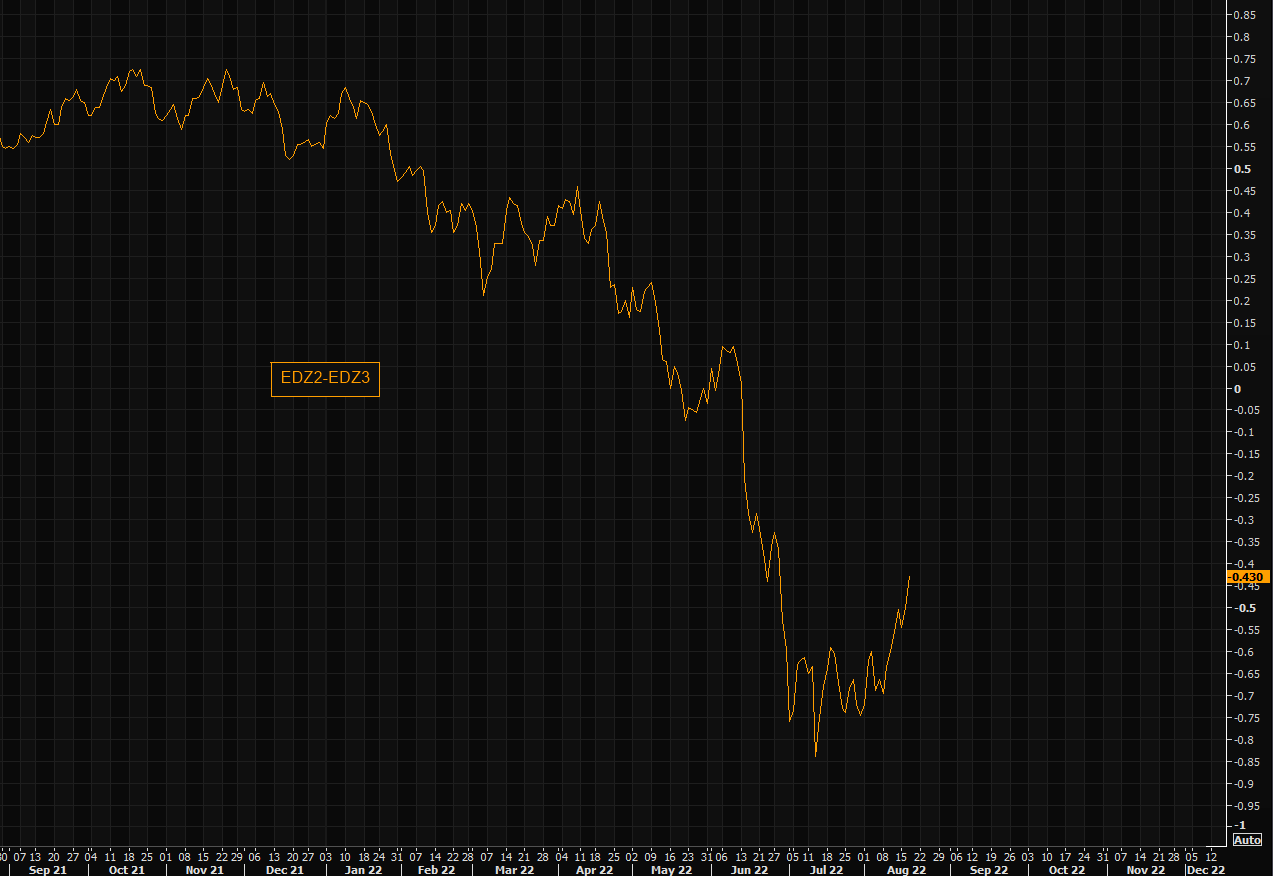

Seen the 2023 cuts?

EDZ2-EDZ3 spread continues moving higher, trading at levels last seen in late June. Second chart showing the shorter term chart vs SPX.

Source: Refinitiv

Source: Refinitiv

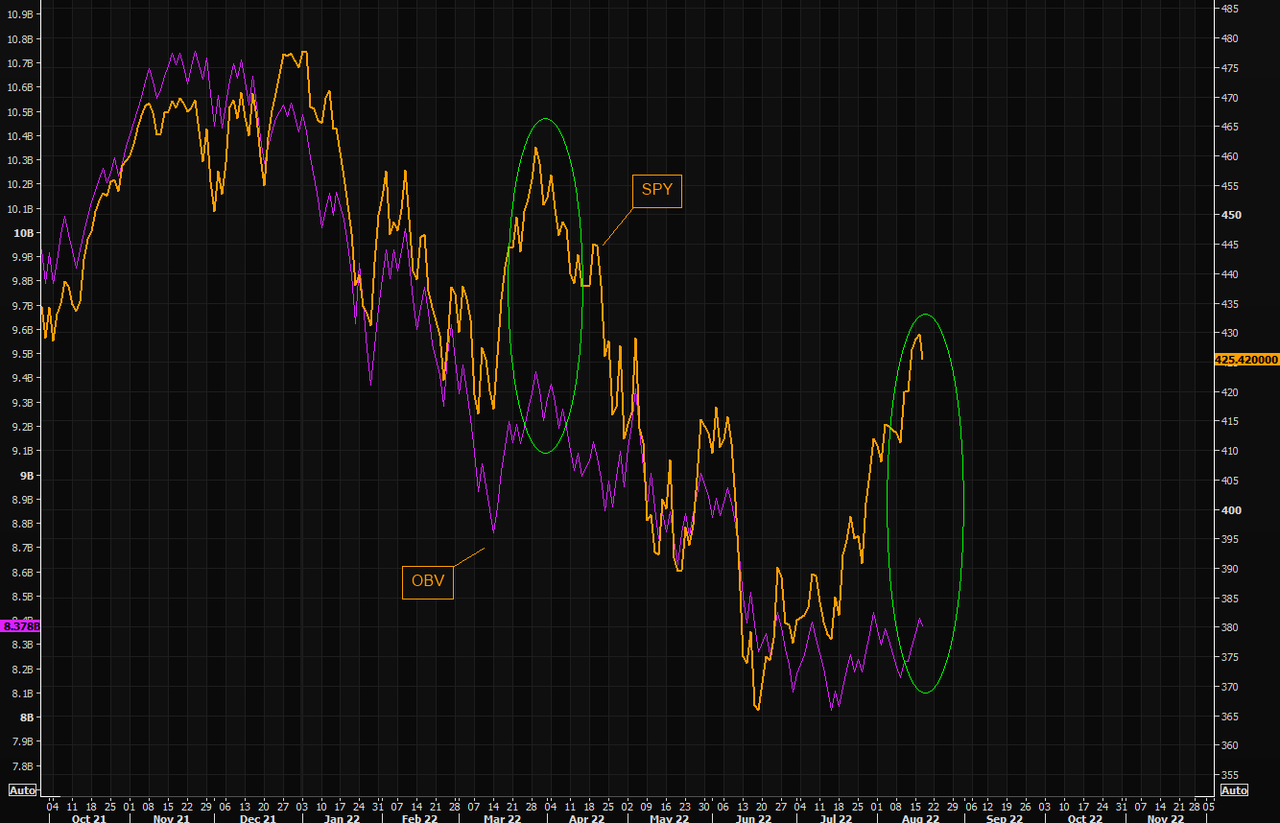

Don’t forget the “lack” of volumes

Just a quick updated chart of SPY vs on balance volume. Very similar to the March “set up”, at least from the volumes perspective.

Source: Refinitiv

Recession or not…

…but M2 money supply is falling quickly and the 2/10 remains rather “depressed”. Nothing for the short term trading mind, but worth having in the back of your head.

Source: Refinitiv

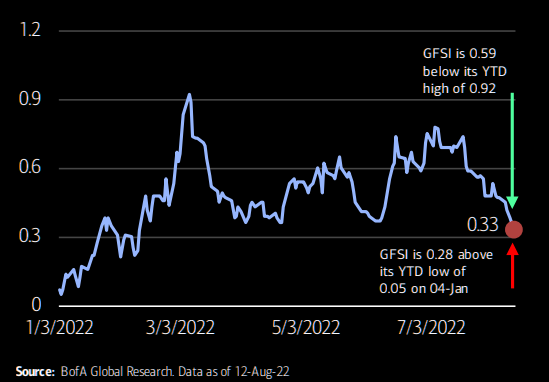

Why not fight the Fed?

BofA writes: “Market stress (inverse of financial conditions) is now closer to YTD lows than highs. With the Fed wanting financial conditions to tighten (higher stress), markets seem comfortable fighting the Fed.”

(GFSI = global financial stress indicator)

Source: BofA

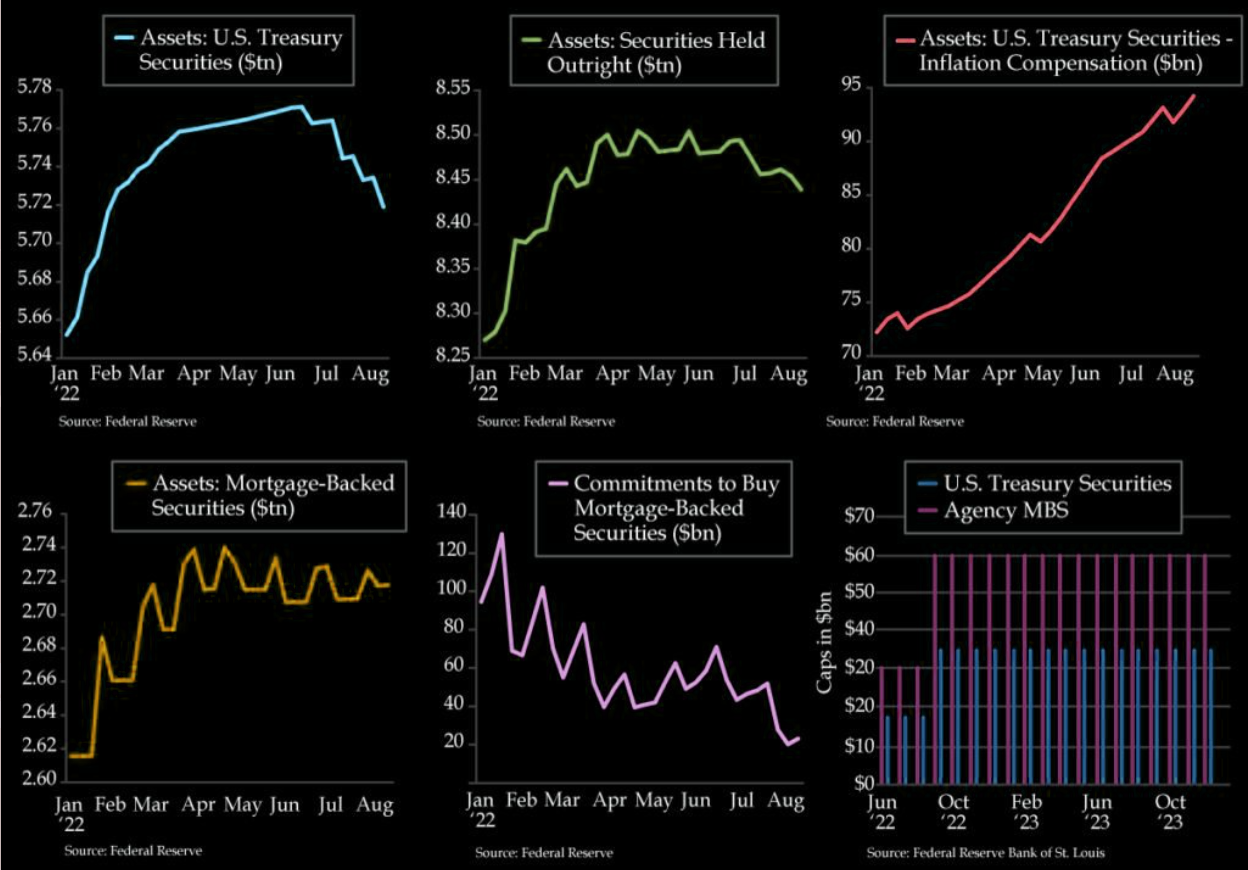

QT

What has been achieved so far. The first chart looks initially like they have progress until you see the scale….

Source: FED

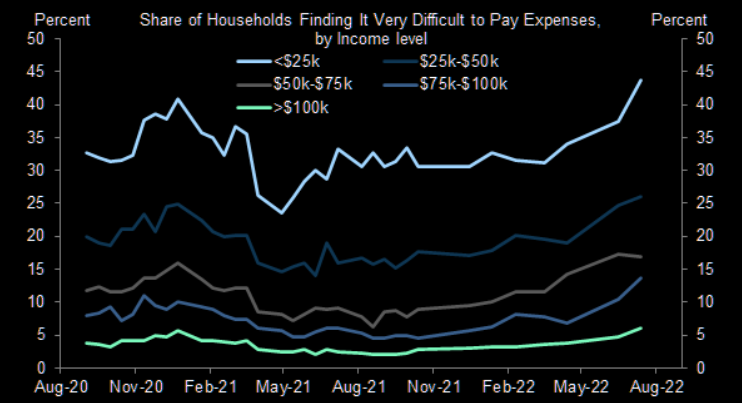

Who pay my bills…?

Low income households are increasingly finding it very difficult to pay expenses.