By Gareth Aird, head of Australian economics at CBA:

Key Points:

- Next week the ABS will publish the Q2 22 Wage Price Index (WPI – 17/8), and the July labour force survey (18/8).

- The semi-annual Average Weekly Earnings (AWEs) data will also be realised, though this tends to get less focus from market participants than the WPI.

- We expect the WPI to increase by 0.8%/qtr in Q2 22 which would see the annual rate step up to 2.7%.

- The unemployment rate on our forecasts will hold flat at 3.5% over July.

- Outcomes in line with our forecast would see us retain our call for the RBA to raise the cash rate by 50bp at the September Board meeting.

- A weaker wages print and/or an increase in the unemployment rate could see the RBA opt for a less aggressive rate rise (they could move back to a ‘business as usual’ 25bp rate hike or raise the cash rate by 40bp to restore it to a more conventional metric – this would send a signal to households and business that the pace of tightening will moderate).

Overview

Next week the ABS will publish key data which relates to the labour market. An update on wages growth over the June quarter and the unemployment rate in July will be critical inputs into the RBA’s policy deliberations at the September Board meeting.

Our central scenario is for the RBA to raise the cash rate by 50bp at the September Board meeting. But this is certainly not a done deal. The RBA could shift to ‘business as usual’ 25bp monthly increments from here, particularly if the upcoming data next week supports the case to slow the rate of policy tightening.

What to expect in the Q2 22 Wage Price Index (WPI)

For all the rhetoric and anecdotes of stronger wages growth, the official WPI has been stubbornly slow to lift. It is true that wages growth has accelerated. But the pace of change has been modest considering the tightness in the labour market.

Indeed the RBA was right on ‘inertia’ in our wages setting process. The WPI is comprised using a similar methodology to the CPI. It is designed to measure pure wages inflation. More specifically, the WPI measures changes over time in the price of wages and salaries unaffected by changes in the quality or

quantity of work performed. Other series like Average Weekly Ordinary Time Earnings (AWOTE), payrolls and Average Earnings National Accounts (AENA) pick up compositional changes in the workforce and/or changes in hours worked.

The WPI computes wages inflation in a more pure form and for that reason it has been the RBA’s preferred measure of wages growth. That said, over the recent past the RBA has focussed on ‘labour costs’ when referring to wages growth, in part because the WPI has been slow to lift.

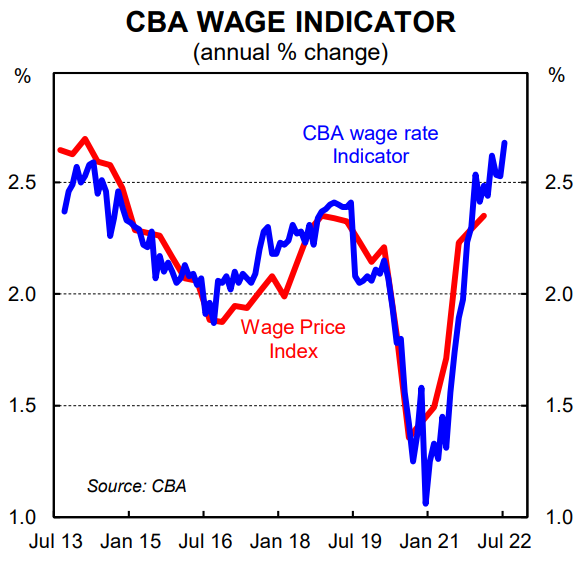

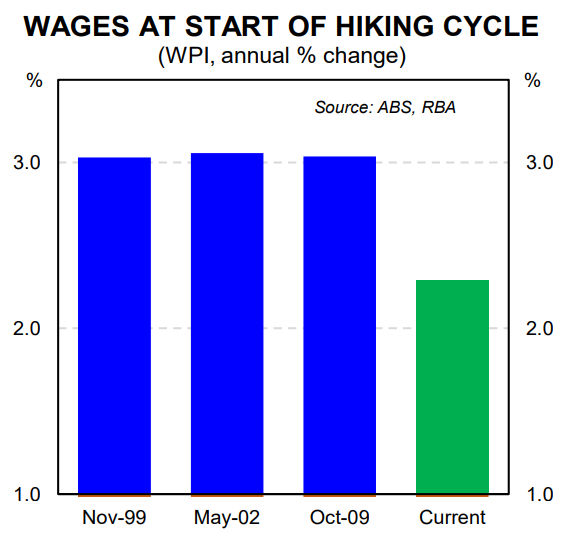

To recall, the WPI rose by 0.7%/qtr in both Q4 21 and Q1 22 (both outcomes were ‘soft’ 0.7% quarterly increases, rounding to 0.65% on a two decimal place basis). The WPI sat at 2.4%/yr at Q1 22 – well below the RBA’s desired range for annual wages growth to settle around 3.5%.

The reference period for the WPI is the middle month of the quarter. As such the Q2 22 WPI will capture the pulse of wages growth as at May 2022.

Our internal data very accurately maps the WPI. It indicates wages pressures in the economy have taken time to emerge. Indeed our data more accurately captures what is happening in the economy than business surveys and business liaison as it is measures actual dollars paid into a matched sample of ~275k CBA bank accounts.

We are able to track wages inflation because we apply a strict criteria to the accounts we include in our sample each month to account for people moving jobs, receiving a bonus or modifying hours worked in any material sense. We also take into account changes in tax rates or levies.

The upshot is that whilst wages growth across the economy is moving higher and some people are receiving large pay rises, there has not broad based wages pressures. Indeed real wages growth (as measures by headline inflation deflated by the wage price index) is deeply negative.

Our internal data indicates the Q2 22 will rise by 0.7-0.8%/qtr. Our point forecast is 0.8%/qtr which would take the annual rate to 2.7%. The risk is skewed to a softer 0.7%/qtr which would see the annual rate print at 2.6%.

What to expect in the July labour force survey

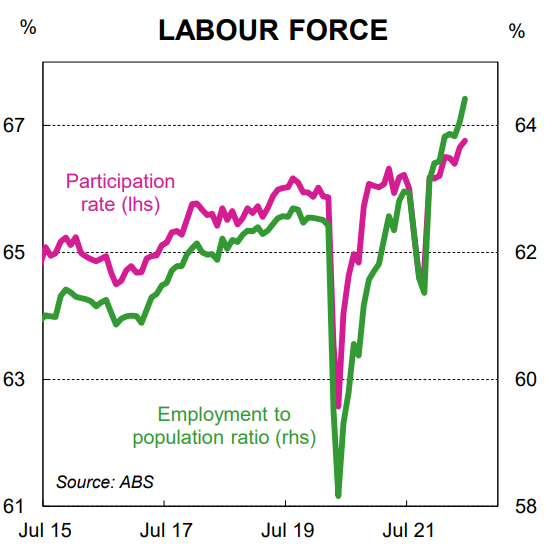

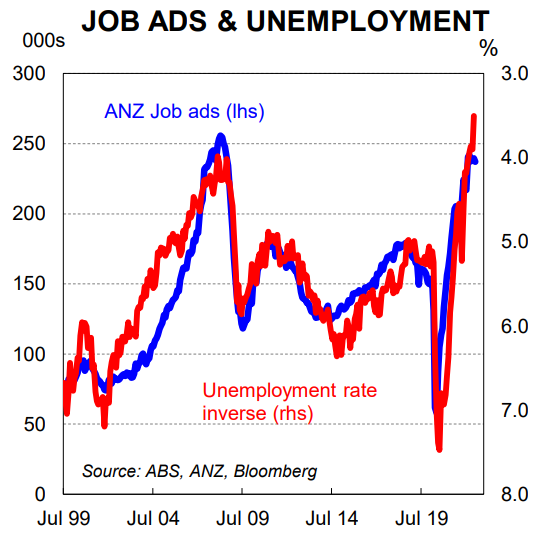

The labour force data has been remarkably strong and the unemployment rate sits at a 50-year low. The June labour force survey significantly bettered market expectations. Employment rose by a massive 88.4k and the unemployment rate fell to 3.5% from 3.9% in May.

The size of the drop in the unemployment rate was surprising given the unemployment rate had printed at 3.9% over the previous three months.

The sell side of economists will be reluctant to forecast an increase in the unemployment rate in July and/or a fall in employment. Indeed we are in that bracket. Our forecast is for an increase in employment of 20k in July and for the unemployment rate to remain at 3.5%. But the risk is tilted towards some

statistical payback and therefore a softer report.

Sample rotation in the monthly survey augments this risk. The June outgoing rotation group has an unemployment rate of 2.8% versus the June total group of 3.4% (original not seasonally adjusted). It also has a higher employment to population ratio (65.7%) than the total group (64.5%). This means that if the July incoming group has similar characteristics to the remaining sample the overall sample will be weakened by the June outgoing rotation group (each month one eighth of the total sample leaves the group and is replaced by an incoming group). See table below.

What does it mean for our RBA call

We think at this stage that if the Q2 22 WPI and July labour force data prints in line with our forecasts the RBA will raise the cash rate by 50bp at the September Board meeting. But that is not a done deal even if the data comes in line with our forecast.

The RBA has put through an incredible amount of tightening already in a very short space of time (175bps over four meetings; i.e. three months). And there is a lag between changes in the cash rate and the impact it has on monthly cash flow for borrowers on a floating rate mortgage.

At CBA, for example, by December the impact of already announced rate rises on monthly cash flow for mortgage holders on variable rate loans will be a four-fold increase compared to July. As such, there is a strong case to slow the pace of rate rises given we expect consumption growth to slow significantly as the lagged impact of rate hikes impacts many households. Indeed we think moving to 25bp ‘business as usual’ increments in the cash rate from here would be prudent against that backdrop.

We suspect the RBA does not share our view at this stage. But the RBA may come around to a similar mindset if the data next week prints softer than our forecasts. More specifically, a weaker wages print and/or an increase in the unemployment rate could see the RBA move back to a ‘business as usual’ 25bp

rate hike or raise the cash rate by 40bp to restore it to a more conventional metric. Either move would send the signal to households and businesses that the pace of tightening will moderate.

In summary our RBA call for the September Board meeting is in the balance and the data next week will see us firm up our expectations for the September decision. The August RBA Board Minutes to be published next week may also contain information that will feed into the mix for our September call. In any event, we still look for the cash rate to peak at 2.6% in this cycle and continue to expect rate cuts in H2 23 (two 25bp are pencilled in for H2 23).